A Quick Take On VTEX

VTEX (NYSE:VTEX) reported its Q2 2023 financial results on August 8, 2023, beating revenue but missing consensus earnings estimates.

The firm provides a digital ecommerce system for companies who want to do business in Latin America.

With revenue growth that remains robust, sharply reduced operating losses, continuing momentum with its international expansion and a strong balance sheet, I’m upgrading my outlook for VTEX to a Buy at around $5.60 per share.

VTEX Overview And Market

UK-domiciled VTEX provides enterprises and large retailers with an online retail platform that enables them to more effectively conduct business in Latin America.

Management is headed by Co-CEO and Co-Chairman Geraldo Thomaz, who previously graduated with a degree in mechanical engineering from the UFRJ.

The company’s primary offerings include:

-

API

-

Multi-tenant platform

-

Low code development

The firm seeks enterprise clients who aim to market and sell their products online in Latin American countries.

According to a 2023 market research report by Americas Market Intelligence, the market for ecommerce in Latin America was estimated at $375 billion in 2022 and is forecasted to reach $831 billion by 2026.

This growth, if achieved, would represent a CAGR of 22% from 2023 to 2026.

The countries of Peru and Mexico are expected to grow at the fastest CAGR rate, at 35% and 33%, respectively.

Brazil, the largest market by size, is expected to grow at a CAGR of 17% through 2026.

Major competitive or other industry participants include:

-

SAP

-

Oracle

-

Magento

-

Salesforce

-

Shopify

VTEX’s Recent Financial Trends

-

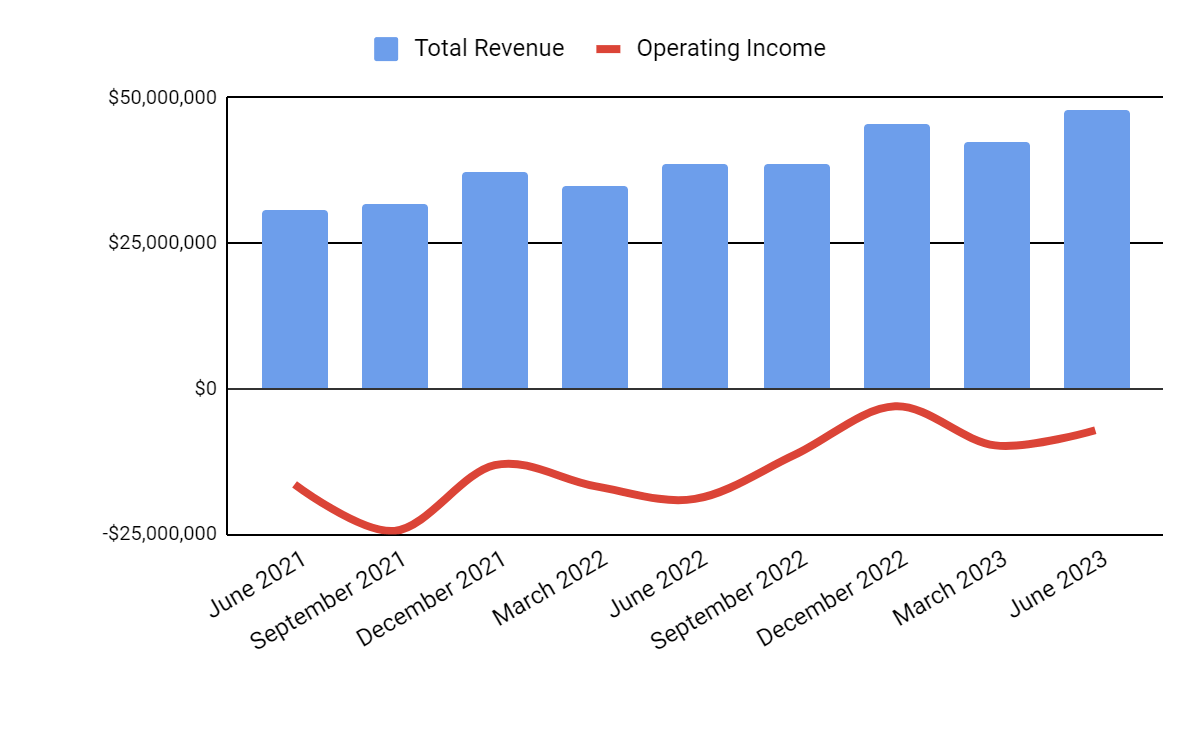

Total revenue by quarter has continued to rise due to growing demand for international ecommerce in LatAm. Operating income by quarter has grown and trended toward breakdown from rising gross profit and reduced SG&A expenses even as revenue has increased.

Total Revenue and Operating Income (Seeking Alpha)

-

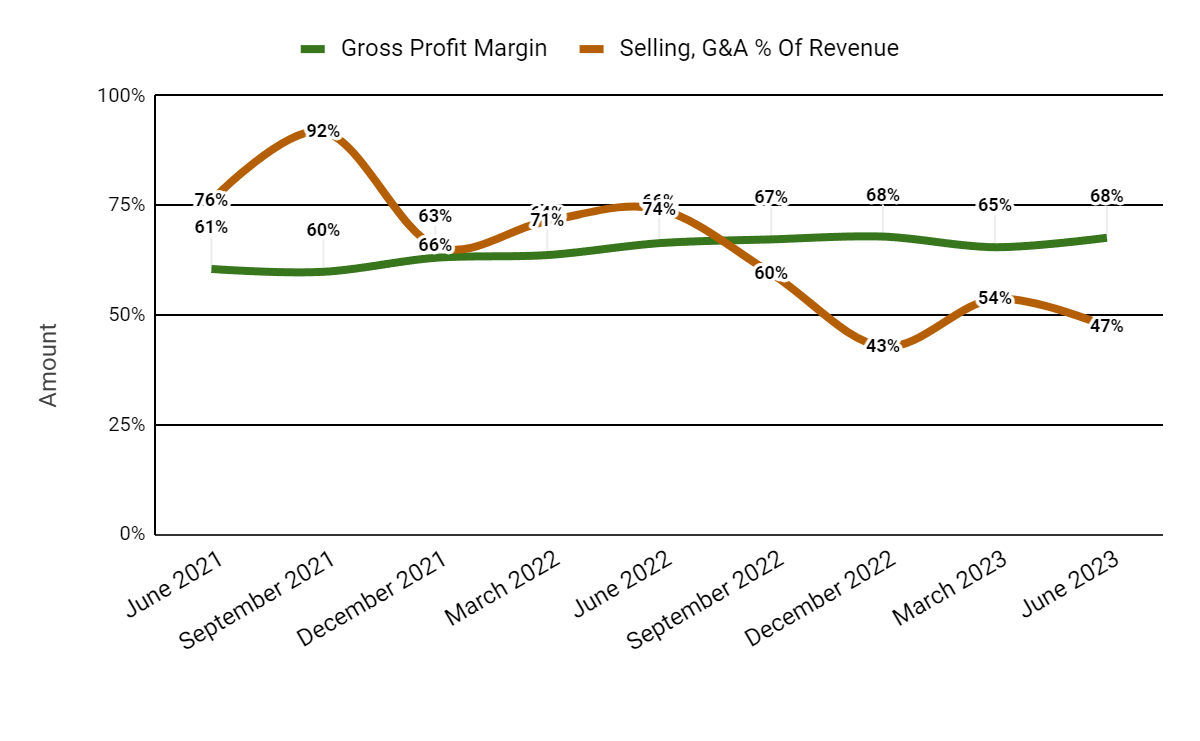

Gross profit margin by quarter has increased as a result of migrating non-core services to lower-cost hosting providers and optimizing its support cost structure. Selling and G&A expenses as a percentage of total revenue by quarter have dropped because of its previous organizational restructuring efforts.

Gross Profit Margin and Selling, G&A % Of Revenue (Seeking Alpha)

-

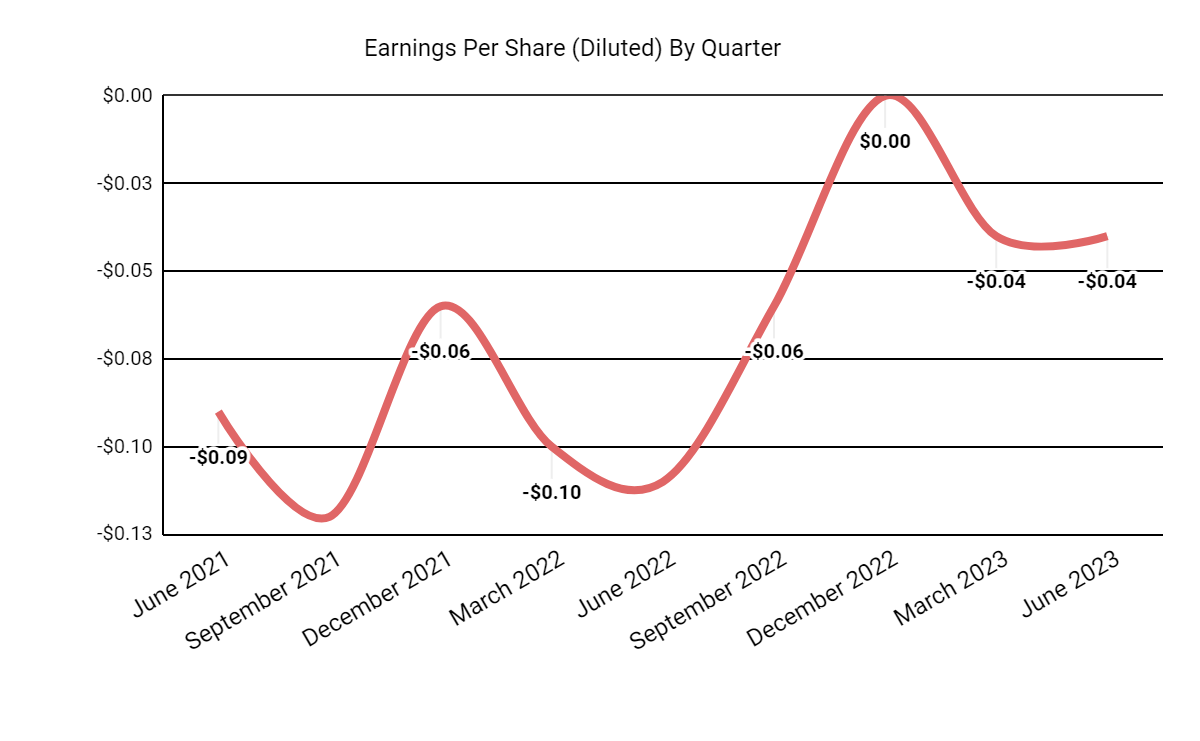

Earnings per share (Diluted) have trended closer to breakeven due to the operational efficiencies gained in recent quarters as well as increasing revenue.

Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

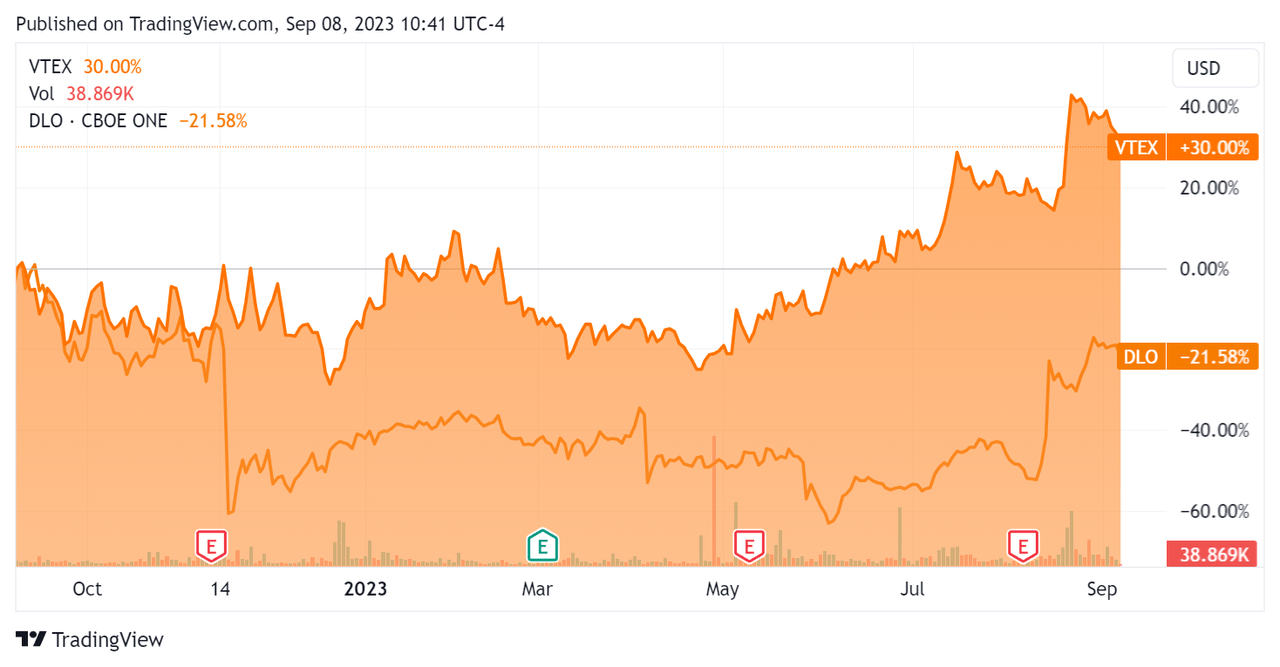

In the past 12 months, VTEX’s stock price has risen 30% vs. that of DLocal’s (DLO) fall of 21.58%:

52-Week Stock Price Comparison (Seeking Alpha)

For balance sheet results, the firm ended the quarter with $222.5 million in cash, equivalents and short-term investments and no debt.

Over the trailing twelve months, free cash used was negative ($3.3 million), during which there were no capital expenditures. The company paid $3.6 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For VTEX

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

5.2 |

|

Enterprise Value / EBITDA |

NM |

|

Price / Sales |

6.4 |

|

Revenue Growth Rate |

22.5% |

|

Net Income Margin |

-15.1% |

|

EBITDA % |

-16.1% |

|

Market Capitalization |

$1,120,000,000 |

|

Enterprise Value |

$898,540,000 |

|

Operating Cash Flow |

-$8,770,000 |

|

Earnings Per Share (Fully Diluted) |

-$0.14 |

(Source – Seeking Alpha)

VTEX’s most recent unadjusted Rule of 40 calculation was 6.4% as of Q2 2023’s results, so the firm has improved since Q4 2022, but still needs substantial further improvement, per the table below:

|

Rule of 40 Performance (Unadjusted) |

Q4 2022 |

Q2 2023 |

|

Revenue Growth % |

25.3% |

22.5% |

|

EBITDA % |

-29.9% |

-16.1% |

|

Total |

-4.6% |

6.4% |

(Source – Seeking Alpha)

Sentiment Analysis

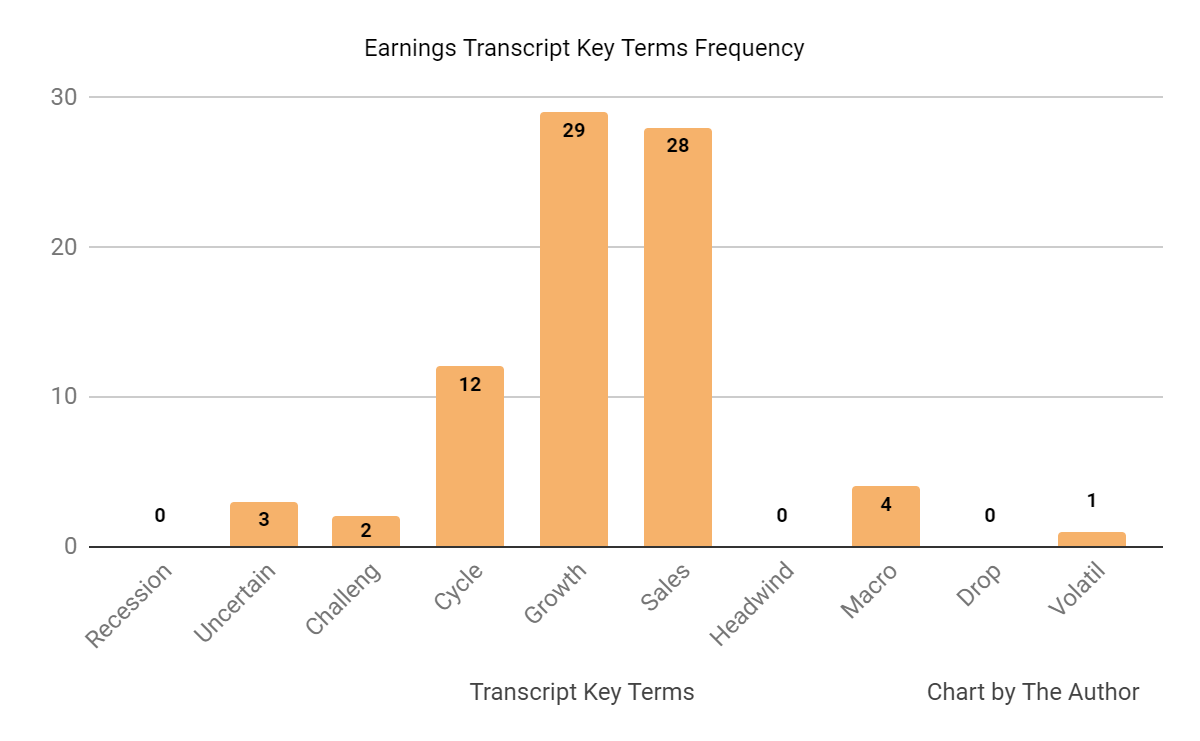

The following chart shows the frequency of various words used in the most recent earnings conference call by management for analysts.

Earnings Transcript Key Terms Frequency (Seeking Alpha)

Analysts questioned the company about competitive pressures, capital allocation and sales cycle dynamics.

Management responded that it hasn’t been seeing any changes in the competitive landscape or in pricing pressures.

Also, the recent stock buyback allocation is a result of opportunities from its strong balance sheet and also provides an offset from the dilution from stock-based compensation in the quarter.

Leadership said that its current guidance assumes sales cycle stabilization and not yet for an improvement or recovery back to a more normal sales cycle.

Commentary On VTEX

In its last earnings call (Source – Seeking Alpha), covering Q2 2023’s results, management highlighted the gross merchandise value [GMV] growth of 23.4% year-over-year.

Same-store sales grew in the ‘teens range, although slightly below historical levels.’

Management also noted that its international expansion efforts have been ‘progressing’, with a number of large international customer wins in the quarter.

Leadership did not provide any client or revenue retention rate metrics but characterized its retention as ‘low annual revenue churn’.

Total revenue for Q2 2023 increased by 23.8% year-over-year and gross profit margin grew by 1.2%.

Selling and G&A expenses as a percentage of revenue dropped by 26.8% YoY, indicating sharply improved efficiency in generating incremental revenue and operating losses were reduced by an impressive 62.4%.

The company’s financial position is reasonably strong, with ample liquidity, no debt and a small amount of negative free cash flow over the last twelve months.

VTEX’s Rule of 40 performance has been low and in need of improvement, but increasing sequentially somewhat.

Looking ahead, consensus revenue estimates put 2023 growth at around 23.6% over 2022.

If achieved, this would represent a slight decline in revenue growth rate versus 2022’s growth rate of 25.4% over 2021.

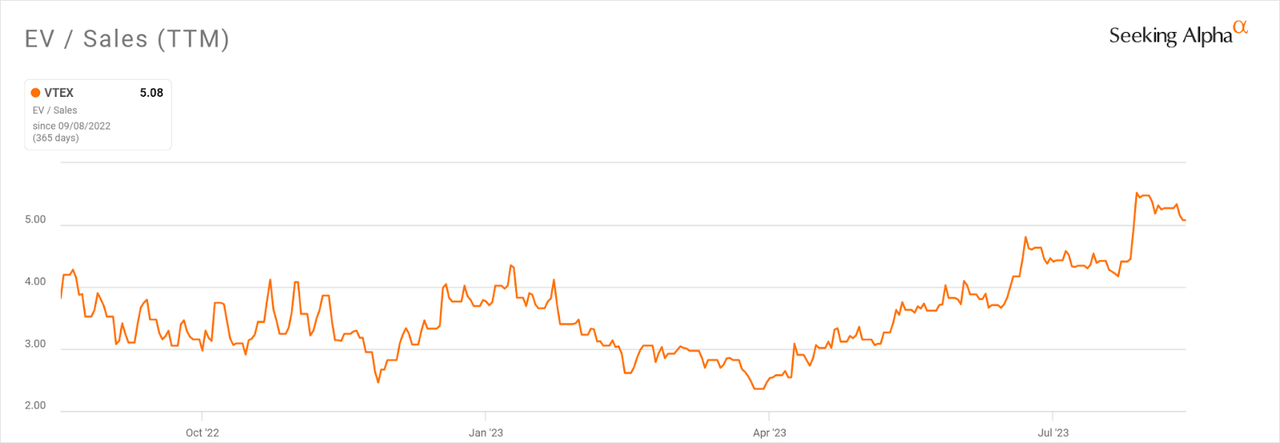

In the past twelve months, the firm’s EV/Sales valuation multiple has risen a net of 33%, as the chart from Seeking Alpha shows below:

EV/Sales Multiple History (Seeking Alpha)

A potential upside catalyst to the stock could include continued strength in the Brazilian Real against the US Dollar.

However, this strength has been confined to the past year. Over the longer term, the Brazilian Real has depreciated against the US Dollar, providing long-term headwinds to the company’s revenue growth as denominated in dollars for US shareholders.

With revenue growth appearing robust, sharply reduced operating losses, continuing momentum with its international expansion and a strong balance sheet, risk-on investors may wish to consider VTEX.

My outlook is a Buy for VTEX at around $5.60 per share.

Read the full article here