Grove Collaborative (NYSE:GROV) is a plastic-neutral retailer offering personal care and household products. They posted Q2 FY23 results, and I will review the results in this report. They have struggled to achieve profitability, but the management is working towards it. Still, I think it is quite risky to invest in it. In addition, the technical chart of GROV is quite bearish, and I won’t recommend investing in it at the current level. Hence, I assign a hold rating on GROV.

Financial Analysis

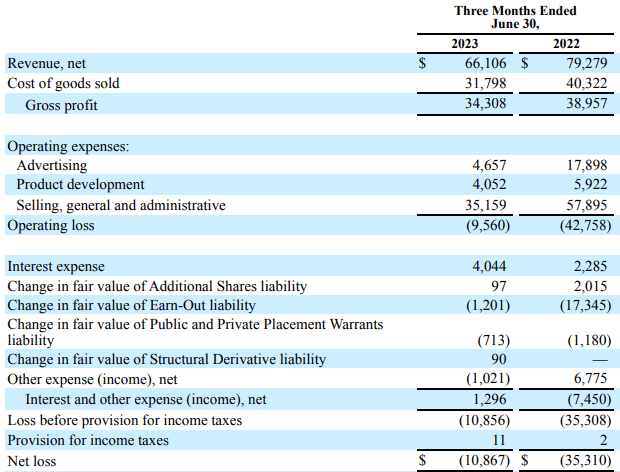

GROV announced its Q2 FY23 results. The revenue for Q2 FY23 was $66.1 million, a decline of 16.6% compared to Q2 FY22. I think a decline in DTC orders due to fewer active customers was the main reason behind the revenue decline. The management attributed lower spending on advertising to the customer decline. The gross profit margin for Q2 FY23 was 51.9%, which was 49.1% in Q2 FY22. Carrier mix optimization and higher pricing were the major reasons behind the improvement.

Seeking Alpha

Due to better cost control, they were able to lower the net loss. The net loss for Q2 FY23 was $10.8 million compared to a loss of $35.3 million. Although the revenue decline is a concern, I think one positive came out from Q2 FY23 results. The management mentioned at the start of the fiscal year 2023 that their main aim in FY23 will be to focus on profitability, and due to the cost control efforts of management, they were able to limit their losses. Despite lower revenues and gross profit, the management limited the operating loss, which is impressive.

Technical Analysis

Trading View

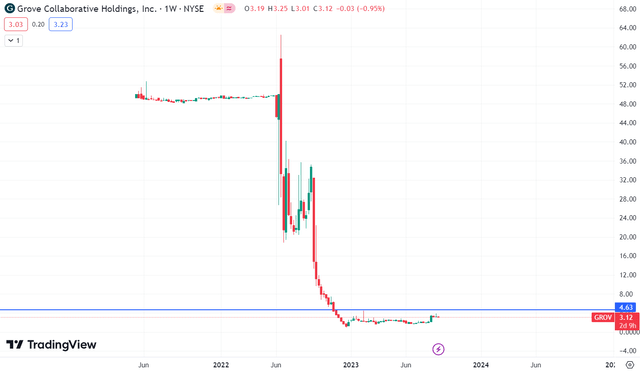

This stock has been a nightmare for the investors. It has gone down by 93% from its IPO level. The stock tried to form a base at $20 in 2022. But, after consolidating for about four months, the stock gave a huge breakdown and continued to fall. This has been the nature of the stock since its debut. The stock consolidates in a range for months and continues to fall. Now, talking about the recent price action, the stock has been consolidating in a small range for the last eight months, and there is a high chance that we might see a breakdown in the stock. So, I would suggest that one should ignore the stock right now. Talking about the buying scenario, it would only arise if the stock breaks the $4.6 level because the last time the stock tried to break $4.6, it failed miserably. So $4.6 becomes an important level because if it crosses $4.6, we might see a trend reversal. But until then, I would advise you to ignore it.

Should One Invest In GROV?

I mentioned earlier that the cost control by the management was impressive, and the management is working towards profitability. But they have yet to achieve profitability, and if we look at their past performance, we can see that they have never been profitable. That is one of the major reasons that I would be hesitant to invest in GROV, which might be why the market has punished its stock price since its debut. Additionally, the results of the company have been quite volatile over the years. In FY19, their net loss was $161.5 million, and in FY20, it came down to $72.3 million, but in FY21, the loss again increased to $135.9 million, and in FY22, it reduced to $87.7 million. So the results don’t depict a isn’t a clear picture. So, investing in such companies can be risky, and the results can be volatile. Hence, I would suggest not investing in GROV till they achieve profitability. I usually don’t recommend investing in such loss-making companies because, most of the time, loss-making companies are unable to provide returns to their shareholders, and it is the same in the case of GROV. Hence, I assign a hold rating on GROV.

Risk

Since its beginning, the corporation has suffered enormous losses. They experienced net losses of $87.7 million, $135.9 million, and $72.3 million, respectively, for the years ended December 31, 2022, 2021, and 2020. They had a $577.9 million cumulative loss as of December 31, 2022. As they increase their customer base, broaden their retail distribution platform, improve their current direct-to-consumer website and mobile application, expand their research and development efforts to grow the product assortment offered by their Grove-owned brands, purchase or create additional Grove-owned brands, and hire more personnel to support these initiatives, they anticipate continuing to experience significant costs and operating losses for the foreseeable future. Grove has historically focused most of its financial and non-financial resources on sales and marketing, including a significant increase in their marketing team and budget, continued business growth, product-related research and development, and general administration costs, such as legal, accounting, and other expenses. They might not be able to raise sales in a way that will be sufficient to cover these higher costs, since they have historically relied on their mobile application and online direct-to-consumer website. Failure to raise sales while they undertake business-growth efforts could keep them from being profitable.

Bottom Line

The management’s cost control efforts proved quite beneficial, and as a result, they were able to limit the loss. But still, they are not profitable, and I don’t suggest investing in loss-making companies. In addition, the technical chart of GROV is quite bearish. So I would advise you to ignore it. Hence, I assign a hold rating on GROV.

Read the full article here