“Our wisest long-term investment is not in the dirty polluting fossil fuels from the past, but in the clean energy of the future.” – London Breed

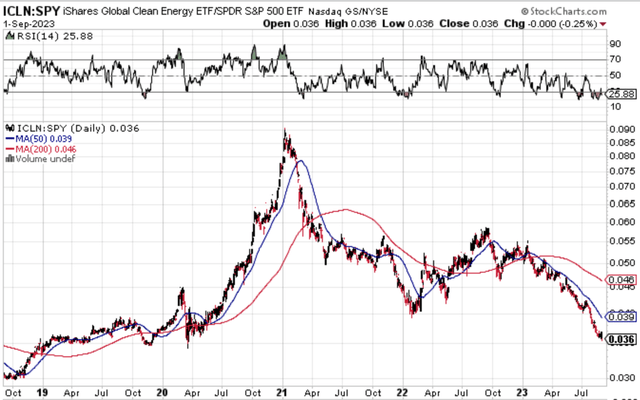

Clean energy has always been one of the more interesting parts of the marketplace to focus on, and often times is also one of the most disappointing. Energy stocks had a phenomenal year last year, but have languished on a relative basis since. Without strong oil, it’s hard for investors to care about alternatives. This might explain why the iShares S&P Global Clean Energy ETF (NASDAQ:ICLN) has performed so poorly since 2020 relative to the S&P 500.

Stockcharts.com

The iShares Global Clean Energy ETF is a fund that tracks the investment results of an index composed of global equities in the clean energy sector. The fund, launched in 2008, is managed by BlackRock and offers exposure to companies that produce energy from renewable sources, including solar, wind, and other low-carbon technologies.

The objective of ICLN is to provide investors with a way to participate in the transition towards cleaner energy sources. However, while the fund’s investment strategy may seem appealing at first, there are several factors that investors need to consider.

I wrote about this fund back in 2021 and conditions have only worsened since then for the space as more and more attention turned to energy and oil given years of underinvestment. Is there any hope for this to at some point become cheap enough to buy? Given the sentiment and narrative changes, it’s a tall task for now.

ICLN Holdings: A Close Look

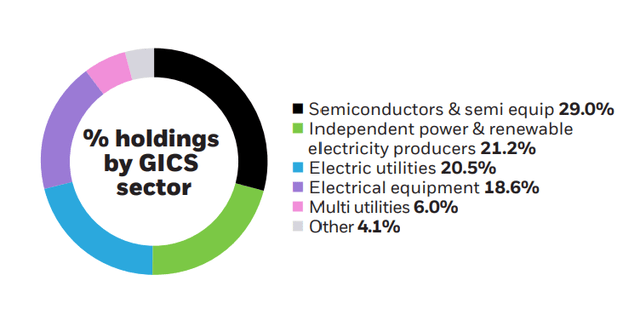

ICLN’s portfolio is concentrated in a few sectors and geographies, offering a particular exposure that may not be suitable for all investors. As of June 30, 2023, the fund’s top holdings were primarily in the semiconductor equipment, renewable electricity, and electric utilities sectors. The fund’s largest holding was First Solar Inc. (FSLR), a U.S.-based solar panel manufacturer, followed by SolarEdge Technologies Inc. (SEDG), an Israeli firm focused on solar micro-inverters and battery energy storage.

iShares.com

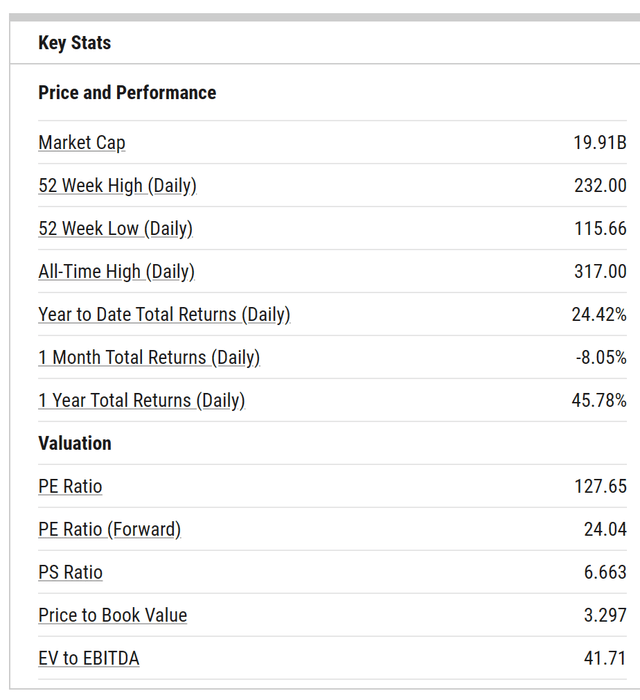

First Solar looks very overvalued. Could it grow into its valuations? Sure – but the reality is this as a top holding is not something I personally am a fan of.

YCharts.com

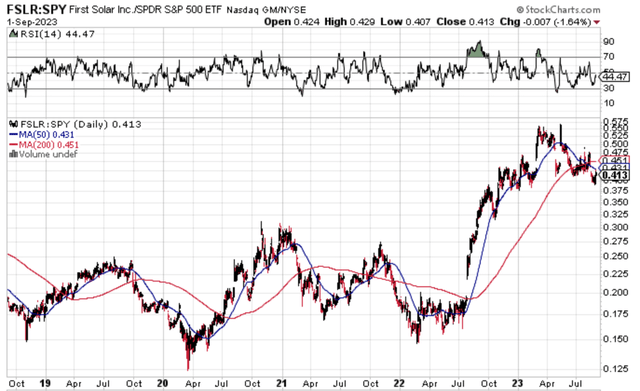

If we look at FSLR relative to the S&P 500 (SPY), a lot of performance has indeed been pulled forward, and it looks like we are at a juncture where relative underperformance is actually picking up.

Stockcharts.com

ICLN’s geographic exposure is also highly concentrated, with nearly 44% of its assets in U.S. companies. China, Denmark, Spain, and Brazil also constitute significant portions of the fund’s geographic allocation.

While this concentration might provide investors with targeted exposure to specific areas of the clean energy sector, it also increases the fund’s risk profile. Extreme concentration in a few sectors or geographies can lead to higher volatility and potential losses if those markets underperform.

Future Challenges for Clean Energy

The transition to clean energy, while promising, is fraught with challenges. Regulatory hurdles, grid capacity limitations, supply chain disruptions, and labor shortages pose significant obstacles to the growth of the clean energy sector.

Regulatory issues, in particular, can delay or derail clean energy projects. For instance, the European Union has experienced extensive administrative delays in issuing permits for renewable energy projects. Similarly, the lack of grid capacity can limit the amount of renewable energy that can be produced and distributed.

Supply chain disruptions, exacerbated by the COVID-19 pandemic, have also slowed down clean energy projects worldwide. For instance, in the third quarter of 2022, clean energy production fell significantly due to supply chain issues.

Labor shortages, too, present a formidable challenge. With many sectors of the economy experiencing a tightening labor market, renewable energy companies are finding it hard to attract and retain skilled workers.

ICLN: A Case for Caution

Given the challenges facing the clean energy sector and the fund’s past performance, investors may want to think twice before investing in ICLN. While the fund offers targeted exposure to the clean energy sector, its high sector and geographic concentration, coupled with the potential headwinds facing the sector, make it a risky proposition.

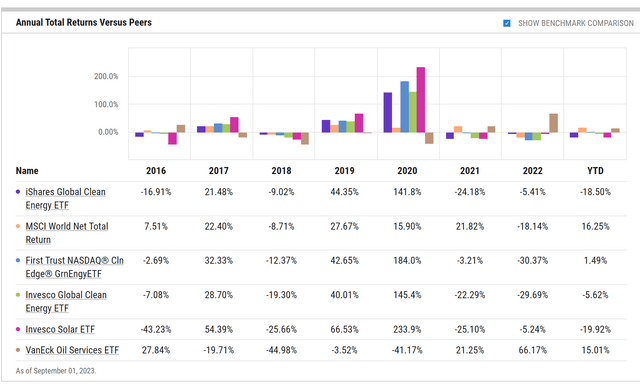

In addition, when compared with other ETFs with similar investment objectives, ICLN falls short.

YCharts

This goes beyond fees and beyond near-term performance. In the case of ICLN, the risks seem to outweigh the potential benefits when looking at the investment case for oil and energy more broadly. While I recognize it’s a different set of core beliefs, the investment case remains far stronger for oil than clean energy given how capital starved the space has been for years. If you’re big on clean energy, it might make more sense to avoid broad based ETFs and look for some selective stock selection opportunities. Either way, this is not a fund for me.

Read the full article here