Staid Business, But An Impressive Dividend Profile So Far

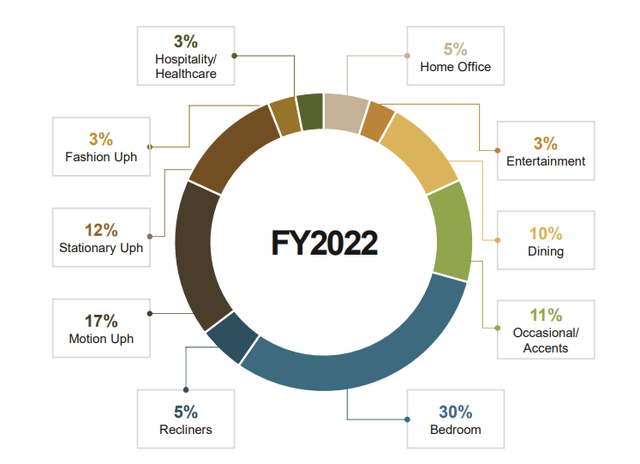

Hooker Furnishings Corporation (HOFT) is a Virginia-based company that is involved in the business of home furnishing (72% of its sales are imported products, although it does also resort to some domestic manufacturing). HOFT’s product profile involves case goods, leather furniture, fabric-upholstered furniture, and customized leather-based furniture, all of which it makes, or procures, for the residential, hospitality, and contract markets of the US. Also, the bulk (~30%) of its product portfolio is oriented towards the bedroom.

2022 Presentation

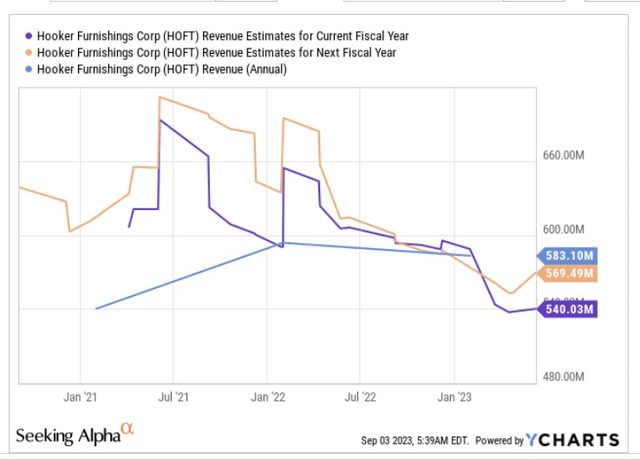

All in all, it’s fair to say that you’re looking at a company that is involved in a rather staid and unremarkable industry. In fact, YCharts consensus shows that even two years from now, the topline of HOFT will still be around 2% short of what was seen last year ($583.1m).

YCharts

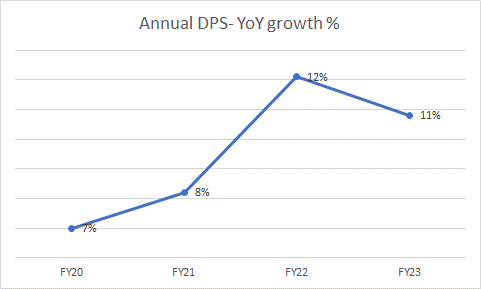

Whilst the core story may not be exciting enough for most investors’ tastes, there’s a very important sub-plot that typically attracts a lot of investors; we’re talking about the dividend profile. You won’t find too many micro-cap stocks that have been doling out dividends for well over two decades. HOFT has also been growing its dividends for seven straight years now, and crucially the cadence of growth has improved in recent years. The annual DPS growth averaged around 8% p.a. during FY20; FY21 has been coming in at double-digit levels in recent years. Besides, if you get in at these levels, you could lock in a very tasty forward yield of over 4%, over 60bps better than the stock’s 4-year average.

10-K

Unsavory Developments Off Late

All this is very well, but if one explores HOFT’s dividend safety rank on Seeking Alpha, it is rated rather poorly with a D- grade. Meanwhile, if one peruses the recent earnings transcript, one would know that the HOFT management is also on record flagging numerous risks such as a “softer retail environment”, “lower sales of major furniture chains and mass merchants”, “economic uncertainties”, “higher discounting”, and “transition to a new leaner business”. Also, note that HOFT does not currently have any explicit long-standing capital distribution policy and in the annual report, management states:

The determination as to the payment and the amount of any future dividends will be made by the Board of Directors on a quarterly basis and will depend on our then-current financial condition, capital requirements, results of operations and any other factors then deemed relevant by the Board of Directors.

The takeaway here is that the dividend isn’t certain, but is rather fluid, and could be susceptible to quarterly dynamics

Nonetheless, given all these considerations, it is understandable if HOFT’s fans are facing some degree of trepidation about the stock’s dividend narrative. Let’s explore the internals and see if there’s a genuine reason to be truly concerned.

Ascertaining The Forward Dividend Coverage

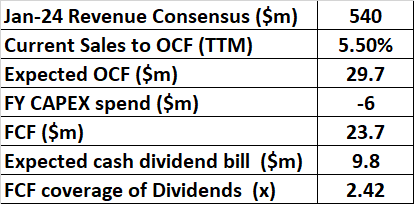

If one looks at HOFT’s recent dividend hikes (the last 4 hikes), they have come in increments of $0.02. Assuming a similar cadence going forward, investors can expect an annual cash DPS bill of $0.90 for the whole year (three-quarters of the existing $0.22 dividend and one-quarter of $0.24). At the current weighted average shares outstanding figure that would translate to a cash dividend bill of $9.8m (it is all but likely that this bill could be lower as HOFT could also buy back shares which in turn would reduce the cash bill). All in all, does HOFT have the innate capability to generate roughly $10m in free cash flow? Well, we think that shouldn’t be a problem given the plans that HOFT has with its inventory (in the Q2 call, management spoke of their desire to reduce inventories by $30m by the year-end).

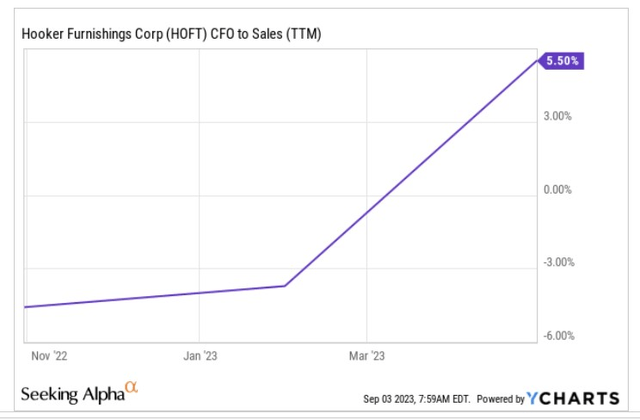

Despite a subdued end market, investors should note that there have been ongoing improvements on the operating cash flow front, which puts the dividend coverage in a better spot. Over a year ago, HOFT was unable to convert any sales to OCF (Operating cash flow), and it was in negative territory, but over the past couple of quarters, that margin has picked up to levels of 5.5%.

YCharts

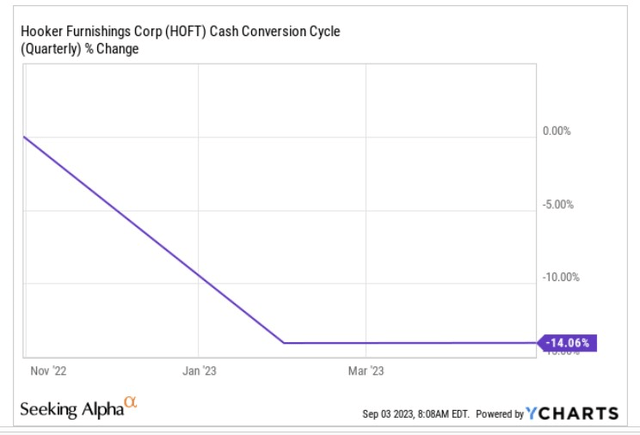

This is mainly on account of improvements on the working capital front, with the days tied up in working capital coming down by 14%.

YCharts

Much of this is driven by management’s goal to get inventories in line with the demand; on a YTD basis, the Hooker Brands division’s inventories are down by $14m, whilst the Home Meridian International Brands division has seen a $9m decrease. Despite the decrease, management noted that inventory still remains elevated versus the 2019 calendar levels, and they will continue to make progress on this front.

All things considered, we feel that investors could expect the OCF to sales margin to trend beyond mid-single digit levels. Now, even if we assume no improvement on the OCF margin and maintenance at the same levels (5.5%), that would still translate to around $30m of potential OCF this year (based on YCharts sales estimates Jan 2024). Then management has also stated that they plan to spend $6m on CAPEX this year (source: Q2 transcript), leaving us with a prospective year-end FCF figure of $24m. In effect, given HOFT’s dividend bill of less than $10m, you’re looking at very healthy FCF to dividend coverage of roughly 2.4x! That would also leave HOFT with ample elbow room to wrap up $5.5m worth of pending buybacks.

YCharts

Given what we’ve just learned, we think the dividend safety quant rank of D- comes across as too harsh.

Closing Thoughts – Technical And Valuation Commentary

If one reviews the valuation and technical narratives of the HOFT stock, one gets a mixed perspective. Firstly, let’s start with what we like. If micro-cap-based investors were looking for suitable mean-reversion trades within the micro-cap universe, we’d like to think that HOFT could be a decent shout. The image below highlights HOFT’s positioning relative to its peers from the iShares Micro-Cap ETF, and we can see that the current ratio is a good 35% below the mid-point of the long-term range.

StockCharts

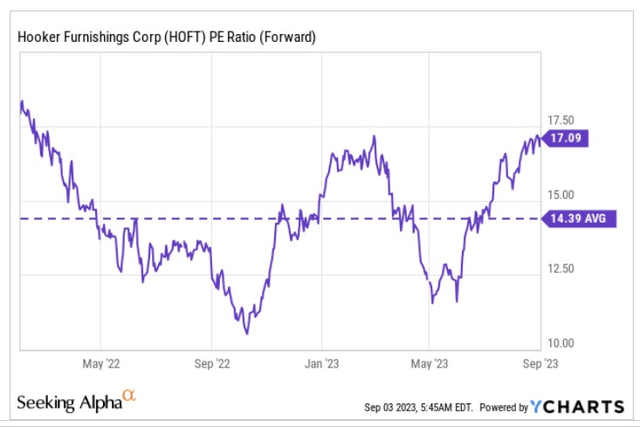

However, to come up as a consummate mean-reversion play, one would also need to see dirt-cheap forward valuations, but unfortunately, that’s not what you’d get with HOFT if you were to stage an entry now. On the recent earnings call, HOFT management did state that they “expect some short-term volatility in sales and earnings at the Home Meridian segment“. Nonetheless, this is expected to leave an adverse mark on overall earnings, making the valuation narrative unappealing. As per YCharts estimates, HOFT is likely to deliver Jan 2024 EPS of $1.28; at the current share price that would translate to a rather expensive forward P/E of over 17x (~20% higher than the stock’s long-term average of 14.4x). Also note that the multiple is pricier than the sector median of 15.2x.

YCharts

Finally, if we switch over to the standalone weekly chart of HOFT, we can’t say that we’re too chuffed with the current reward-to-risk dynamics on offer. This is a stock that tends to be rather unidimensional in its movements for long periods, and since Q2-22 the stock has been trending up in the shape of an ascending channel. Unfortunately, it looks like currently, the price is very close to the upper boundary of this channel ($23 levels), with a huge gap from the lower boundary (sub $17 levels). This is another factor that dampens the buy case.

Investing

Read the full article here