In my opinion, some of the best prospects in this market today are those companies that operate midstream energy infrastructure and logistics assets. Examples of these assets include pipelines, storage facilities, terminals for handling commodities and finished products created from commodities, and more. Even though the energy market can be incredibly volatile, firms in this space often achieve steady and growing cash flows over time. This allows them to pay attractive distributions that, often, result in higher yields than dividend paying stocks. One firm in this market that definitely deserves attention is MPLX LP (NYSE:MPLX). While the company is not the cheapest player in its space, its overall financial health is solid and the trajectory that it has taken over the years has been encouraging. Given these facts, I feel comfortable rating the company a ‘buy’ to reflect my view that shares should outperform the broader market for the foreseeable future.

An interesting midstream play

Even though I am active in analyzing companies in the midstream space, I have not dug in too much into MPLX LP since writing about the company back in May of 2019. At that time, the company had agreed to acquire Andeavor Logistics at an equity value of $8.67 billion. Since those days, management has succeeded in further growing the company. But before we get into the fundamental data, it might be helpful to discuss some of its assets.

MPLX LP

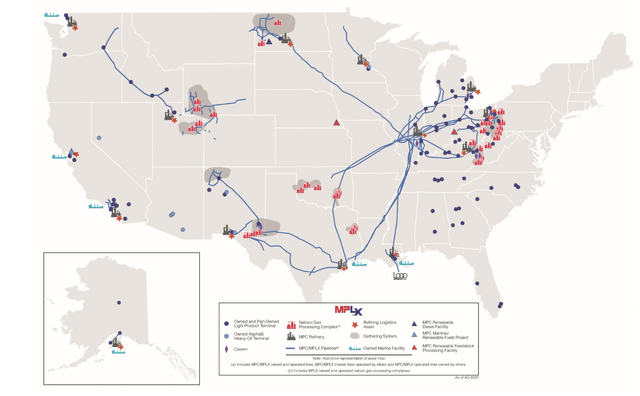

The best way to do this, I believe, is to break the firm up into its two operating segments. The first of these is known as the L&S, or Logistics and Storage, segment. Through this unit, the company focuses on gathering, transporting, storing, and distributing crude oil, refined products, renewable energy sources, and more. The segment also is involved in refining logistics, the operation of terminals, the oversight of rail facilities, the operation of storage caverns, and other similar activities. As of the end of the firm’s 2022 fiscal year, this segment included 15,105 miles of holy and jointly owned pipelines and associated storage assets. It also controlled refining logistics assets for 13 refineries, 89 terminals, and a variety of other properties.

Next in line, we have the G&P segment, also known as the Gathering and Processing segment. This unit, unsurprisingly, is involved in activities such as the gathering, processing, and transportation of natural gas. However, it also provides similar activities, including also fractionation and storage, for NGLs. These assets, at the end of the 2022 fiscal year, boasted 10.4 Bcf per day of gathering capacity as well as 12 Bcf per day of natural gas processing capacity. On top of this, the company also had fractionation and de-ethanization capacity that totaled 829 thousand barrels per day.

MPLX LP

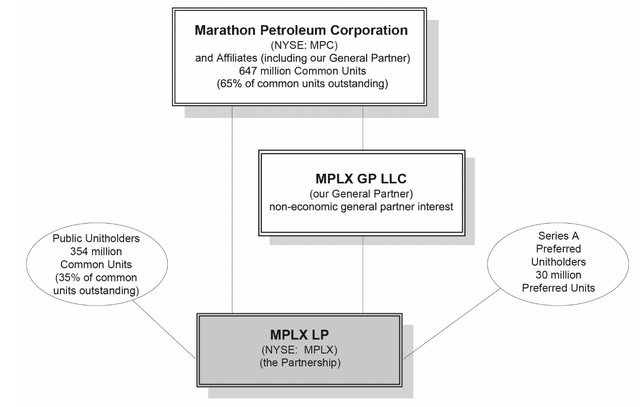

One of the things that makes MPLX LP most interesting and unique is its ownership structure. Approximately 65% of the company’s outstanding shares are owned by Marathon Petroleum Corporation (MPC). That company also has a non-economic ownership over the general partner of MPLX LP. The remaining 35% of outstanding stock, as well as all of the 29.5 million preferred units of the company, are owned by the public. In addition to having control over MPLX LP, Marathon also is responsible for about 47% of the company’s revenue, making it, by far, its largest customer.

Author – SEC EDGAR Data

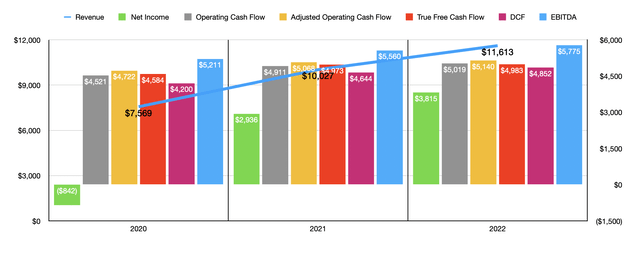

In terms of overall financial performance, MPLX LP has been a really great enterprise. In the chart above, you can see that all of the company’s most important financial metrics have improved over the three years ending in 2022. Revenue jumped from $7.57 billion to $11.61 billion. But even more important than that would be the earnings and cash flow results of the company. The firm went from a net loss of $842 million in 2020 to a net profit of $3.82 billion last year. Operating cash flow grew from $4.52 billion to $5.02 billion. If we adjust for changes in working capital, we get an increase from $4.72 billion to $5.14 billion. DCF, also known as distributable cash flow, grew from $4.20 billion to $4.85 billion, while EBITDA increased from $5.21 billion to $5.78 billion. Another metric I like to look at in this space is what I refer to as ‘true free cash flow’. This is derived from taking adjusted operating cash flow and only stripping out maintenance capital expenditures from it. This prevents the company in question from being punished for its growth-oriented capital expenditures. Over the past three years, this metric expanded from $4.58 billion to $4.98 billion.

Author – SEC EDGAR Data

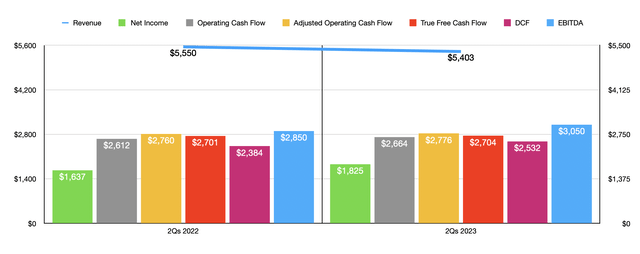

As you can see in the chart above, financial performance for the first half of 2023 is also looking up compared to the same time one year earlier. Yes, revenue is lower year over year. However, profits and cash flows continue to grow. This growth has been made possible in large part by continued spending on growth-oriented initiatives. Over the past three fiscal years, management has allocated $2.40 billion toward capital expenditures. Of this amount, $2.06 billion was focused on growth initiatives, with the rest in the form of maintenance spending. Last year alone, MPLX LP allocated $712 million toward its growth initiatives. This year is slated to be even higher. Total spending should be around $950 million, with $800 million of it attributable to growth.

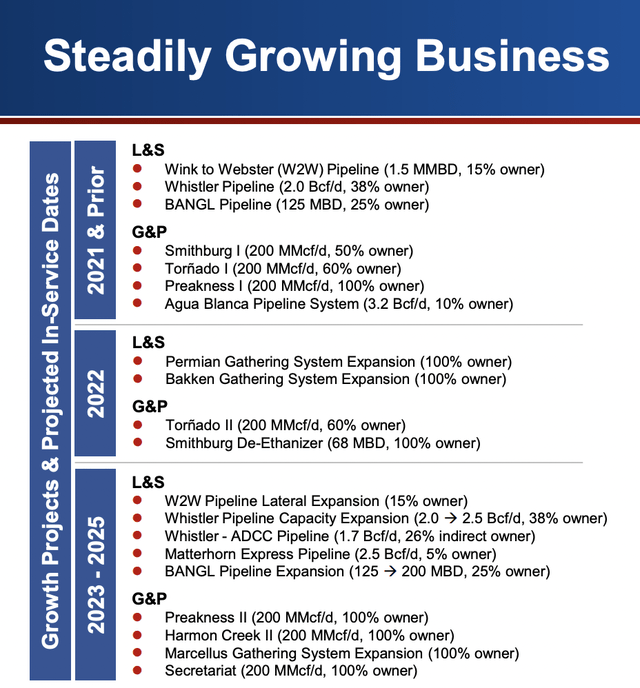

Realistically, investors should expect this kind of capital allocation to continue for the next few years at least. Between 2023 and 2025, for instance, management is allocating an unknown amount of capital toward three different pipeline expansion projects and two complete under the L&S segment. The investments here will increase gas transportation capacity by no less than 4.7 Bcf per day, and will increase NGL capacity by 75 thousand barrels per day. Of course, these are not projects that the company has 100% ownership interest in. In fact, the smallest of these projects they own only 5% of. In addition though, the firm is also allocating capital toward four different projects under the G&P unit. These are all 100% owned and well, collectively, boost capacity by 200 MMcf per day once completed.

MPLX LP

One concern that many investors might have is that it is true that the days of fossil fuels are numbered. But those days add up to decades, not just years. According to energy behemoth Exxon Mobil (XOM), for instance, global energy demand is expected to rise by 14.4% from 2021 through 2050. Actual oil demand should grow by 5.7% over that window of time, while gas demand should climb an impressive 21.7%. So between now and at least 2050, MPLX LP and companies like it should be in a good position to generate significant cash flows for shareholders.

Author – SEC EDGAR Data

*$ in Millions

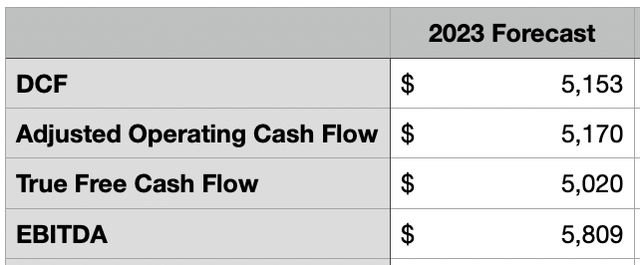

If we continue the pace that we have so far this year, MPLX LP should achieve the financial metrics shown in the table above. These are modest improvements, but improvements all the same. It is worth noting that achieving the EBITDA that I forecasted of $5.81 billion should translate to a net leverage ratio for the company of 3.38. And this excludes any additional cash flows that might reduce net leverage between the end of the second quarter of this year and the end of the final quarter of this year.

Author – SEC EDGAR Data

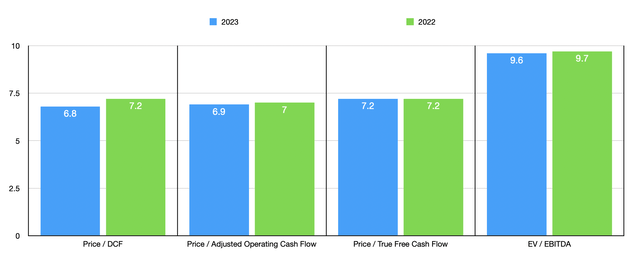

Taking the aforementioned financial metrics, I was then able to create the chart above. In it, you can see just how cheap shares are on a forward basis. You can also see how shares are priced using data from 2022. As part of my analysis, I took two of these metrics and compared the company to five similar firms. On a price to operating cash flow basis, I found that only two of the five companies ended up being cheaper than MPLX LP. This number increases modestly to three out of the five if we rely on the EV to EBITDA approach.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| MPLX LP | 6.9 | 9.6 |

| Energy Transfer (ET) | 4.1 | 7.9 |

| Kinder Morgan (KMI) | 7.4 | 11.0 |

| Cheniere (LNG) | 3.9 | 4.2 |

| ONEOK (OKE) | 8.0 | 9.3 |

| The Williams Companies (WMB) | 7.5 | 10.0 |

Takeaway

I must say that, for the most part, I really like what I see when I look at MPLX LP. The company seems to be in solid shape. Leverage is under control. Shares are attractively priced. And on top of all of this, management continues to invest in growth initiatives in order to create even more shareholder value down the road. Relative to similar firms, MPLX LP looks to be closer to fair value. Plus there are certain risks associated with having such a large shareholder and customer like Marathon. These risks are small and would likely not materialize because the pain inflicted on MPLX LP would also hurt Marathon. But a risk is a risk all the same. Because of these factors, I’ve decided to rate the company only a ‘buy’ as opposed to something more aggressive. But I have no doubt that, in the long run, it will go on to create attractive value for its shareholders.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here