Dear readers/followers,

Vonovia (OTCPK:VONOY) is a German apartment landlord which operates very similarly to a REIT. The company owns and leases over half a million apartments and represents one of my highest conviction stocks in the market today.

I’ve covered the stock extensively here on Seeking Alpha, most recently in an article where I shared parts of my cash flow model for the company, highlighting the fact that recent disposals have improved the outlook significantly, especially with regards to near term debt maturities.

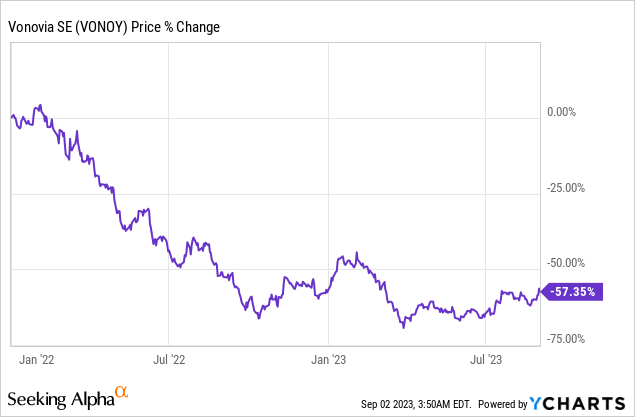

The stock has bounced nicely from the March low of around EUR 15.50 per share for the native share (ticker VNA) and now trades some 40% higher at nearly EUR 22 per share. Still, shares trade 57% below where they were just a year and a half ago and significantly below what I consider fair value, which makes the company interesting even today.

Operational Performance

Once again results have been solid, especially as it relates to Vonovia’s rental segment which represents around 90% of the company’s adjusted EBITDA.

Vonovia’s rental business continues to be very stable with near full occupancy of 98%, near perfect collections of 99.9% and very predictable rent increases of 3-3.5%.

Predictable increases are a consequence of rent regulation, which (simply put) sets a ceiling for rents as the average of market rent over the last 6 years. As a result, Vonovia’s rents lag market rents, but the increases are highly visible and a lot of volatility in market rents gets smoothed out. In turn, rent growth is usually slower in good times, but higher in bad times.

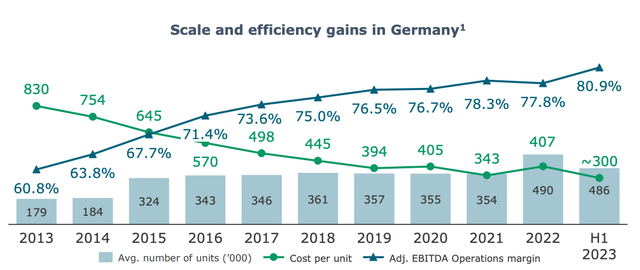

During the second quarter, rental revenues increased by 2.3% (3.5% organic rent growth, but also some disposals). The company also continued to (1) save on maintenance and (2) realize synergies from the incorporation of Deutsche Wohnen and, as a result, posted the highest adj. EBITDA margin ever of nearly 81%.

Vonovia Presentation

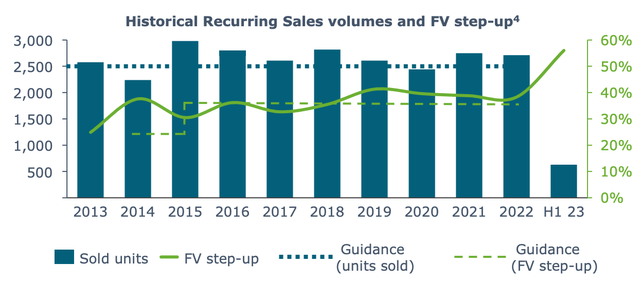

The rest of Vonovia’s segments continued to operate at a similar level seen during the first quarter. Higher cost of material and energy has continued to cause drag on the value-add segment, while low overall investment volume in the market has kept recurring sales low. Despite a slight quarter-over-quarter increase, the number of units sold remains low in comparison to history.

The FV step-up for recurring sales has reached an all-time high of 45%, which means that although the volume is low, at least the company is selling these units at very high prices. Going forward, I expect recurring sales to pick-up gradually as the investment market seems to be coming alive slowly, with investment volumes increasing and several large transactions taking place over the first half of this year. For the time being, however, management has suspended their guidance for recurring sales due to low visibility.

Vonovia Presentation

Overall, total adjusted EBITDA for the first half of the year came in at EUR 1.34 Billion (about 1.2% higher than assumed in the model presented last time).

Guidance for the full year remains strong as organic rent growth has been revised upwards to 3.6-3.9% and the expected Group FFO per share has been confirmed at EUR 2.15 – 2.39.

Notably, the guidance currently calls for the dividend to return to 70% of Group FFO, which is where it has been historically prior to the 50% cut this year.

Frankly, I don’t think it will happen unless interest rates decrease fast and expect the dividend for this year to remain at the current level of 35% of Group FFO so that the company can preserve liquidity for debt repayment. This would be in line with management’s stated focus on cash generation and disposals to delever.

Financing

If you’ve been following Vonovia you know that operational performance is not the reason the stock has sold off so much. The sell off has mostly been related to a high level of debt on the company’s balance sheet and the fear that the company may not be able to meet its near-term debt maturities or that a portfolio revaluation may cause them to breech their debt covenants.

It is true that the company has a lot of debt, largely as a consequence of the acquisition of Deutsche Wohnen which, in hindsight, was poorly timed.

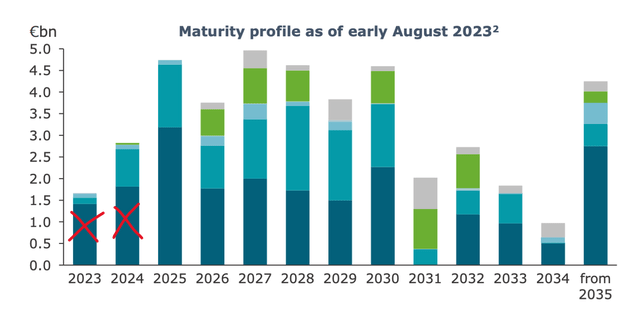

Nonetheless, following previous major disposals to Apollo and CBRE, all of 2023 and 2024 debt maturities are now covered and management can execute their plan to (1) repay all maturing bonds and (2) refinance all bank loans.

Vonovia Presentation, dark blue = bonds, the rest = bank loans

While there have been no further disposals announced since April, the company has identified a potential JV in Northern Germany supposedly similar to the Sudewo deal. If successful, the disposal would allow the company to repay a significant part of bonds maturing in 2025 and would act as a major bullish catalyst for the stock price.

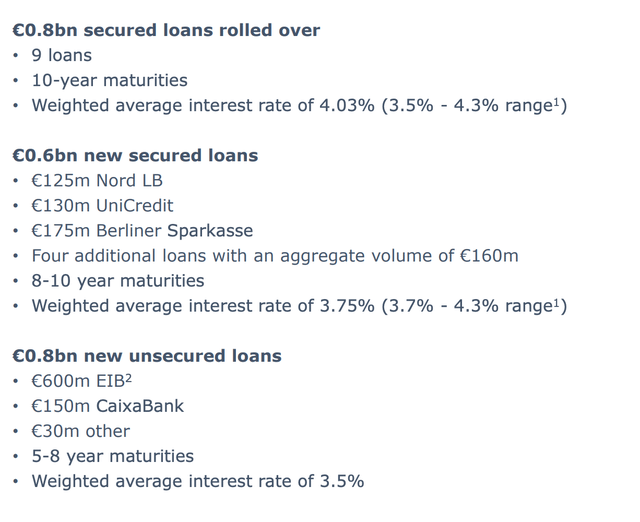

On the refinancing front, Vonovia has done very well over the first half of the year, refinancing EUR 0.8 Billion of loans and securing EUR 1.4 Billion in new loans at reasonable rates of 3.5-4%. This is encouraging, because it’s a clear sign that banks want to continue to work with Vonovia.

Vonovia Presentation

Valuation

Vonovia is a company that is doing exactly what it’s supposed to do on an operational level and despite being somewhat over-levered, it has managed to cover all of its financing needs until the end of 2024 and is now actively working on addressing 2025 maturities.

In the meantime, the valuation has been absolutely hammered.

To understand why I’m so confident that the true fair value is much higher than the current stock price, it’s important to realize just how much housing shortage there is in Germany.

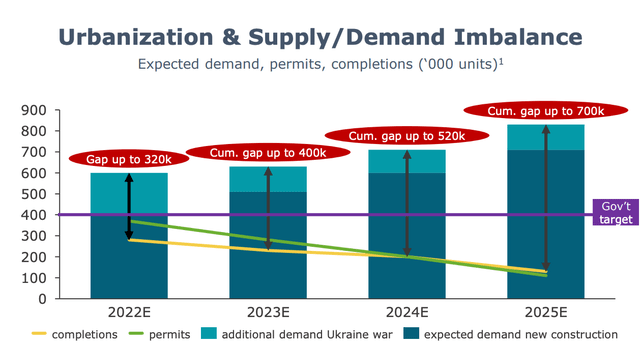

New completions, as well as the number of issued building permits (which is a very accurate proxy for completions 2-3 years later), has been falling for years.

Over the next three years, it is estimated that there will be only about 250 ths. units delivered to the market. This is way below the government’s target of 400 ths. and even further from estimated demand of 600 ths.

Vonovia Presentation

And the thing is that recent events have only made the matter worse. The Ukraine crisis has increased demand and high material and energy prices combined with a higher cost of capital have significantly decreased the pipeline of future projects.

The housing shortage is real in Germany and it will get worse before it (maybe) gets better. In turn Vonovia will benefit by maintaining high occupancy, raising rents and most importantly by owning properties that will be valued more, simply because of their shortage.

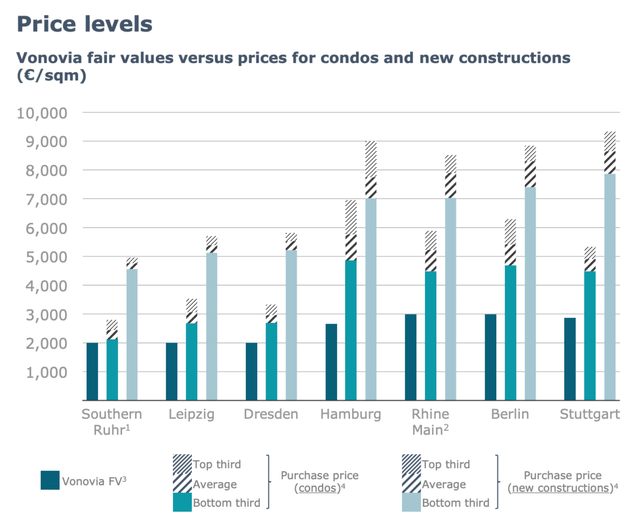

Currently, Vonovia keeps their properties on their books at EUR 2,350 / sqm which is equivalent to NAV per share of about EUR 50. This is way below replacement costs as argued here, and way below market prices for comparable properties.

Vonovia Presentation

And although I do expect the NAV to come down over the next couple of quarters as the company tries to generate liquidity by selling properties (perhaps somewhat below BV), I still see true fair value around EUR 40 per share.

With the stock trading at EUR 22 per share today, that leaves upside of 80%+. I continue to rate the stock a BUY here and don’t plan on reducing my position before at least EUR 30 per share.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here