Looking for a way to gain some income from the Energy sector?

Over the past 3 months, the Energy sector has led all others, rising 13%. This sector is also known for being cyclical, but also has some attractive dividend paying stocks.

One of them, Equinor ASA (NYSE:EQNR) went on a big dividend paying spree in 2022, raising its total quarterly payouts from $.18/share to $.70/share, as energy prices soared in the wake of the Russian invasion of Ukraine. Prices have fallen in 2023, but EQNR’s management still raised the total quarterly payouts to $.90/share in Q1-Q3 ’23.

Company Profile:

Equinor ASA, an energy company, engages in the exploration, production, transportation, refining, and marketing of petroleum and petroleum-derived products, and other forms of energy in Norway and internationally. The company was formerly known as Statoil ASA and changed its name to Equinor ASA in May 2018. Equinor ASA was incorporated in 1972 and is headquartered in Stavanger, Norway.

Equinor’s operations are managed through operating segments, which are:

- -Exploration & Production Norway (E&P Norway)

- -Exploration & Production International (E&P International)

- -Exploration & Production USA (E&P USA)

- -Marketing, Midstream & Processing (MMP)

- -Renewables (REN).

Earnings:

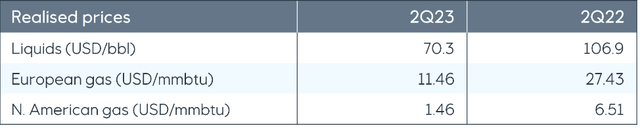

EQNT has had very tough 2022 comps so far in 2023, due to much lower prices. Liquids pricing fell 51%, while European gas fell 58%, and North American gas fell ~77% in Q2 ’23 vs. Q2 ’22.

EQNR site

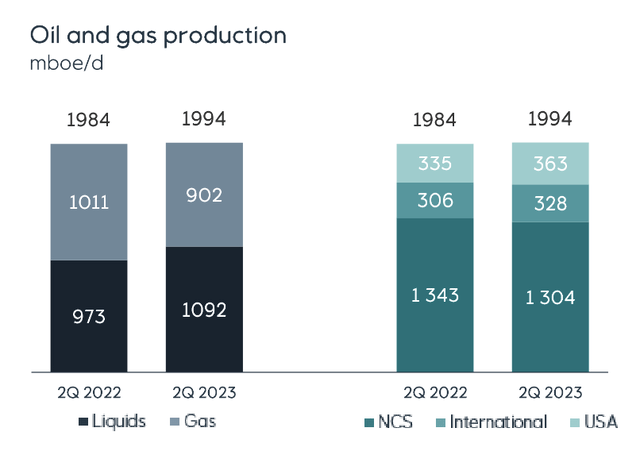

Liquids production rose 12%, whereas Gas volume fell ~11% in Q2 ’23, vs. a year ago. The NCS region’s volume rose 3%, but the international region volume fell ~7%, and U.S. volume fell ~8%”

EQNR site

Norway E&P is the largest segment – it delivered 79% of EQNR’s adjusted earnings in Q2 ’23. E&P International earned 10%, MMP contributed ~9%, and E&P USA earned ~3% of Q1 ’23 adjusted earnings. REN, the Renewables segment had -$84M in Adjusted Earnings.

EQNR site

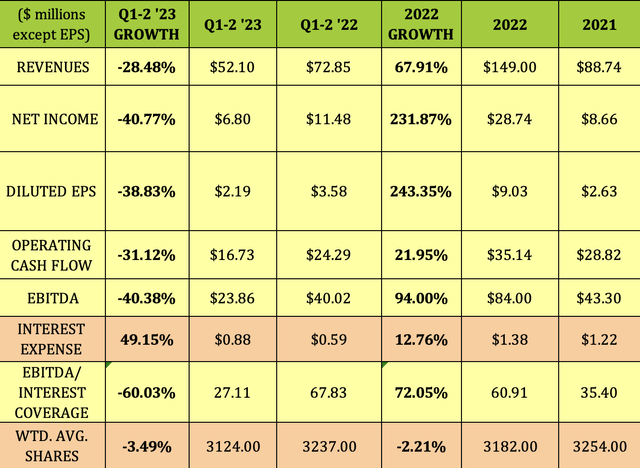

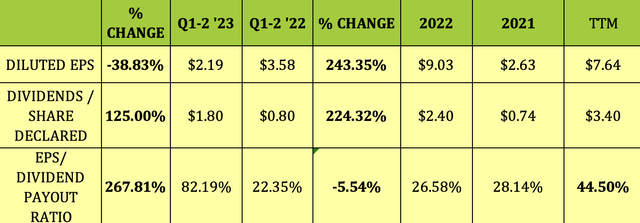

Drastically lower prices and mixed volume growth led to double-digit decreases in revenue, Net Income, EPS, Operating Cash Flow, and EBITDA in Q1-2 ’23. While EQNR has very low debt, Interest Expense still rose 60%, and EBITDA/Interest coverage fell 60%. The share count decreased 3.5%.

Those bleak numbers are in marked contrast to those of 2022, when EQNR enjoyed 3-digit Net Income and EPS growth, 94% EBITDA growth, and 68% Revenue growth:

Hidden Dividend Stocks Plus

Growth Projects:

Management sanctioned 13 projects in 2022, adding around 600M barrels in reserves. They have around 35 exploration wells planned in 2023. EQNR continues to have several large projects in the works for 2023 – 2025 in its E&P Norway and E&P International segments.

By the end of the decade, management expects the production to be on par with current levels, while delivering a 50% reduction in EQNR’s emissions. EQNR has 6 Renewables projects in operation, with an additional one, the Hywind Tampen sanctioned for 2023, and the world’s largest offshore wind farm, the Dogger Bank, being developed in 2024-2026. EQNR owns 40% of this joint venture.

Guidance:

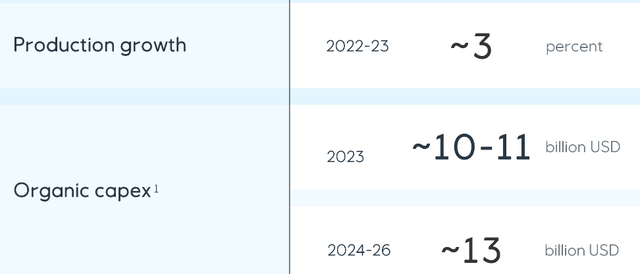

Management guided to ~3% production growth for 2023, with ~$10-$11B in organic Capex.

EQNR site

Dividends:

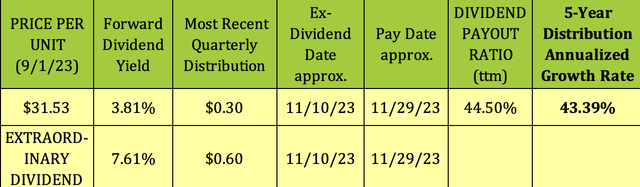

EQNR has a very strong 5-year dividend growth figure of over 43%, due to its rapid escalation, up 224%, in dividends in 2022. That climb reversed EQNR’s formerly negative dividend growth rate. Thus far in 2023, EQNR has paid 3 quarterly $.90 payouts, increasing its base dividend from $.20 to $.30, and paying extraordinary dividends of $.70 in Q1 ’23, and $.60 in Q2-Q3 ’23.

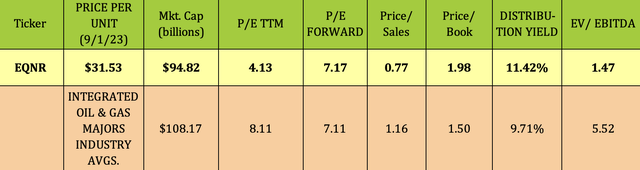

EQNR’s base dividend yield is only 3.81%, but its extraordinary dividend yield is 7.6%, for a total potential forward yield of 11.42%. The big question whether or not management will continue paying those large extra dividends in coming quarters.

EQNR also has share buyback a program for 2023 of $6 billion, and management expects a capital distribution of around $17 billion for 2023.

It has distributed ~$10B in Q1-2 ’23, leaving a ~$7B balance for Q3-4 ’23. With 3.1B shares, the $.90/share distribution totals ~$2.8B/quarter, so it seems that EQNR can continue to reward shareholders with more quarterly $.90 payouts this year.

Hidden Dividend Stocks Plus

The Q1-2 ’23 EPS/Dividend Payout ratio was 82.19%, still tenable, but way up from Q1-2 ’23, when it was only 22.35%.

Hidden Dividend Stocks Plus

Taxes:

While Norway imposes a 25% withholding tax on dividends received by foreign investors, there is a tax credit on foreign taxes paid that you can take on your US tax return. However, you should consult your tax advisor for more info on this matter.

Performance:

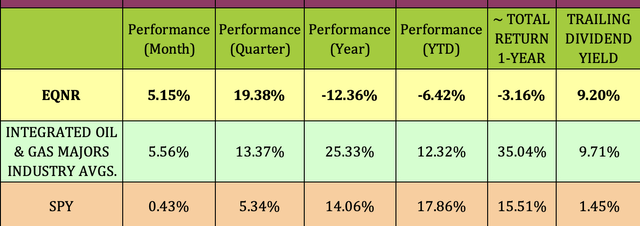

While EQNR has outperformed the S&P 500 over the past month and quarter, it has lagged the S&P and the Oil & Gas Majors industry’s average performance over the past year and so far in 2023 by a wide margin.

Hidden Dividend Stocks Plus

Analysts’ Price Targets:

EQNR just received an upgrade from Morgan Stanley this week, from Underweight to Equal Weight. It also got an upgrade from RBC on 8/9/23, from Sector Perform to Outperform.

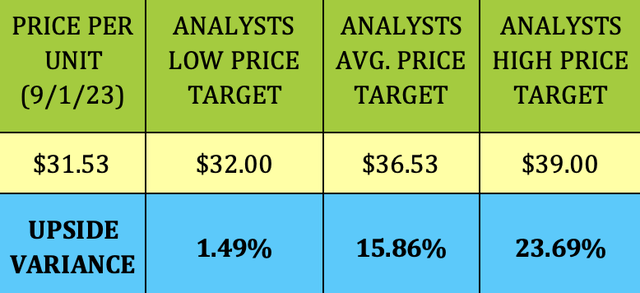

At its 9/1/23 intraday price of $31.53, EQNR was 1.5% below analysts’ $32.00 lowest price target, and ~16% below their $36.53 average price target.

Hidden Dividend Stocks Plus

Valuations:

EQNR looks much cheaper than its industry on a trailing P/E basis, at 4.13X vs. the industry average P/E of 8.11X. However, it’s roughly even on a forward estimated P/E basis. It looks cheaper on a P/Sales basis, and more expensive on a P/Book basis.

EQNR’s EV/EBITDA of 1.47X is very low, due to it having a very small amount of Net Debt.

Hidden Dividend Stocks Plus

Debt, Profitability & Liquidity:

EQNR has remaining long-term bond debt of USD $24.7B, with an average of ~8.5 years to maturity. However, it has $19.65B in Cash, plus ~$23B in short term investments, hence its extremely low Net Debt/EBITDA leverage of just .07X. Its interest coverage is very strong, at over 40X.

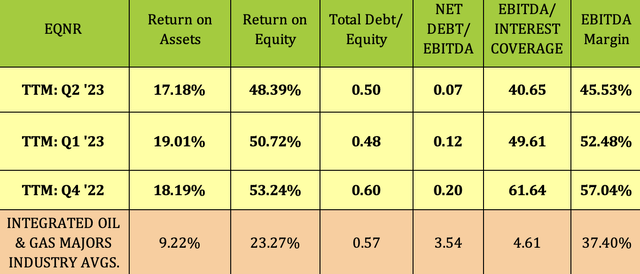

While ROA, ROE, and EBITDA Margin have receded somewhat in Q1-2 ’23, they all remain much higher than industry averages.

Hidden Dividend Stocks Plus

Parting Thoughts:

We rate Equinor ASA a speculative buy, but don’t jump in just yet, wait for a potential market pullback in the treacherous month of September. Another alternative would be to sell puts below EQNR’s price/share.

All tables furnished by our investing group, unless otherwise noted.

Read the full article here