Steadily growing business travel demand helped the US hotel REIT sector turn in stronger operating results for the second quarter. Buoyed by strong occupancy and room rate, the sector’s same store revenue per available room (RevPAR) grew 3.8% compared to a very strong 2Q22.

S&P Global Market Intelligence

Surpassing pre-pandemic RevPAR metrics, however, hasn’t convinced investors that the sector is opportunistic, and shares are still significantly discounted from their closing 2019 levels. Share price performance over the last twelve months demonstrates no love lost on the lodging sector.

Sector Spotlight: Hotel REITs – 1 year share price performance

S&P Global/ 2MCAC as of 08/23/2023

Source: S&P Global Capital IQ/2MC as of 08/23/2023

With the whole sector trading at a consensus estimated 7.8x forward FFO and a double-digit discount to Net Asset Value, we today make the argument that American Hotel Income Properties (OTC:AHOTF) is among the most undervalued of the lot.

Cheaper

The arrival of COVID shut down the world, but almost no industry was as mortally wounded as lodging. Like every hotel REIT suddenly desperate to conserve cash, AHOTF immediately moved to a suspension of its dividend. The shares crashed.

Seeking Alpha

Source: Seeking Alpha

Surprisingly, as operations recovered and American Hotel reinstated a dividend on February 15, 2022, investors seemed to take no notice. The new $0.18/share dividend, payable in monthly distributions, provided an attractive 5.14% yield as measured against the $3.50 share price of 02/15/22, but the shares have continued to slide. At today’s price of $1.64, the dividend produces a stunning 10.97% yield; almost 3x the sector average.

In its most recent investor presentation, management points out that, not only is the dividend sustainable, it equates to a sub 50% payout ratio.

AHOTF

Source: AHOTF

On a value consideration, they note that shares change hands at a huge discount to analyst consensus NAV of C$3.60 ($2.65 USD). For today’s $1.64 share, you pay less than 62% of NAV.

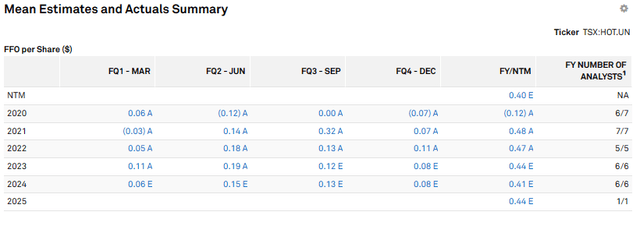

On an earnings consideration, the related consensus indicates the shares are currently trading at 4.08x forecast FFO vs. the sector average of 7.4x.

S&

Source: S&P Global Capital IQ

These basic metrics of yield, discount to NAV, and P/FFO make a reasonably convincing argument that AHOTF shares might be cheaper than those of its peers. It’s less clear as to why.

The Differences

AHOTF is better known, and more widely held, as American Hotel Income Properties REIT LP, which trades on the Toronto Stock Exchange under the ticker (HOT.UN).

S&P Global

The company is headquarted in Vancouver, British Columbia, but its properties are all in the United States.

AHOTF

Source:HOT.UN

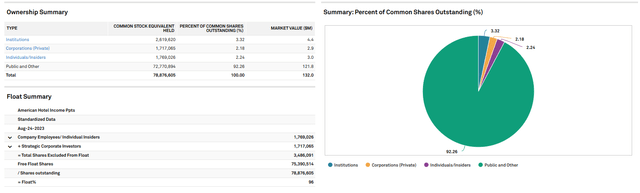

Unlike most established REITs, AHOTF/HOT.UN shares are predominantly held by individuals, not institutions. And most of those individuals are Canadian, eh. Our experience with other Canada based REITs with US property portfolios (think BSR Real Estate Investment (OTCPK:BSRTF), Slate Grocery (OTC:SRRTF), or Flagship Communities (OTCPK:MHCUF)) is that they trade at premiums when Canadians are enthused about investing in US real estate and at discounts when they are not. At present, we are not seeing much enthusiasm.

S&P Global Capital IQ

Source: S&P Global Capital IQ

Another difference is the dividend. While AHOTF reports financial results and pays dividends in US dollars, shareholder returns are reported on a K-1 and not your custodian’s consolidated 1099. Though many investors disdain K-1s and avoid them, the reporting affords highly tax efficient treatment of the dividends.

The Similarities

Though AHOTF is a Canadian domiciled enterprise, it reports all of its financial results and pays its dividends in US dollars. The similarities to other US hotel REITs don’t stop there.

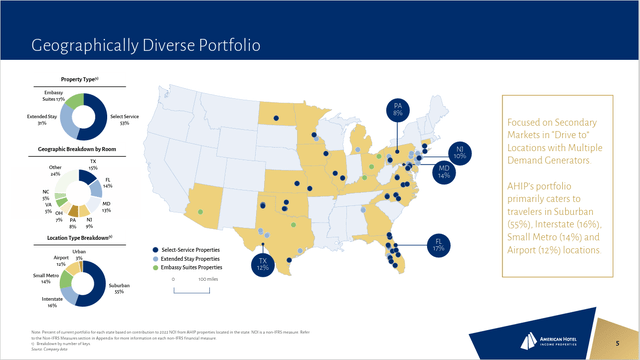

AHOTF has more than 7,900 guest rooms in 70 properties scattered across 47 US cities.

AHOTF

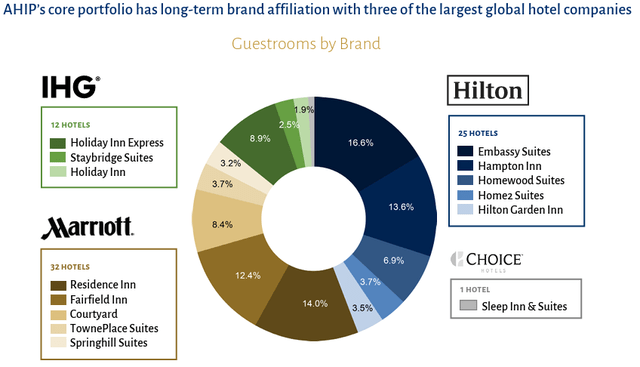

Its hotels are flagged by Marriott, Hilton, and IHG. These are brands you will see in other hotel REITs like Apple Hospitality (APLE), Chatham Lodging (CLDT), RLJ Lodging (RLJ), and Summit Hotel Properties (INN).

AHOTF

AHOTF’s mix of extended stay, limited service, and full service hotels are very similar to those in other REIT portfolios. While AHOTF’s discounted share price might be explained by the differences noted above, the discounts are amplified by risks (perceived and real) of investment in the hotel industry.

Hotels are the most beleaguered sector in commercial real estate

The pandemic, government relief programs, high inflation, and higher interest rates have been hard on all business. For the lodging industry, it has been even more difficult.

When COVID shut down all business, it shut off revenues to hotels like turning off a spigot. Though they had no revenues, they still faced operating costs and debt service expenses (like most hotel REITs, AHOTF carries significant debt). Thus, the dividend suspensions and, in many cases, requests for debt forbearance.

When hotels finally reopened, operators experienced supply chain bottlenecks, labor shortages, and inflated wages just like all other businesses. Maybe just more so.

Though leisure travel has robustly resumed, business travel has had a slower recovery. For the 2nd quarter, the whole sector reported improvements in weekday occupancy (business travel), but it still lags 2019 levels.

Higher interest rates negatively impact all real estate and lodging is no exception. As loans have come due, we have seen some REITs elect to turn properties back to their lender, most notably Ashford Hospitality (AHT) and Park Hotels (PK). AHOTF has paid down some indebtedness and hopes to continue to with surplus cashflows, but it remains highly leveraged.

While expenses have inflated across all real estate operations, property and business insurance rates are rising fast. Two AHOTF hotels were damaged in late 2022 extreme weather events. The hotels are now coming back into service, but in their 2Q earnings release, management revealed new related costs:

“As a result of the claims noted above, higher replacement costs and generally higher premiums, AHIP completed its property insurance renewal effective June 1, 2023, with a significant increase in premiums compared to the expiring policy. On an annualized basis, the increase from the prior year is approximately $3.5 million, which will be recognized in earnings over a twelve-month period.”

Rising insurance costs are not unique to AHOTF or the hotel sector, insurance rates are rising ubiquitously. Hotel REITs have been so badly beaten, it might just be harder to woo back investors.

Risk and Reward

We approach investing in hotel REITs with great trepidation. The industry is vulnerable to every bad economic trend, from competition to inflation to recession.

AHOTF’s high dividend and discounted share price are compelling. We are long.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here