Investment Thesis

Many home renters aspire to become homeowners, but with rising mortgage rates due to elevated interest rates and high inflation, this goal is hard to attain for many of them.

This and the lack of affordable homes is a tailwind for single and multi-family residential REITs. I estimate that Apartment Income REIT Corp (NYSE:AIRC), also known as Air Communities, is a good pick in this sector. The company boasts a high forward dividend yield compared to its peers, approximately 5.50%, and a favorable price-to-FFO ratio. Additionally, it is expected to experience robust FFO growth in 2023.

Overview

AIRC emerged as a spinoff of AIMCO (AIV) and has been trading on the NYSE since late 2020. It is an internally managed REIT with 25,739 apartment homes in mostly eight key markets, including the Bay Area, Boston, Denver, Washington D.C. Los Angeles, Miami, Philadelphia, and San Diego.

New York City is part of the other markets, but exposure there has been reduced during the last quarter, and management aims to exit this market completely by the end of the year.

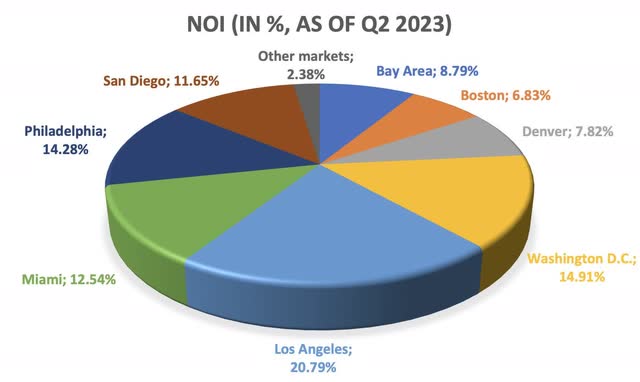

Net operating income is well diversified across these eight markets.

Author’s work, numbers from second quarter 2023 earnings release

Property quality and tenant base

AIRC focuses on high-quality apartments and aims to attract affluent residents. In the last quarter, 58% of its portfolio comprised Class A properties. The average household income of its residents in Q4 2022 was $227,000 which favorably compares to the average of its peers with less than $150,000 income. Despite an average monthly rent of $2797 per unit, I estimate that a high percentage of its residents AIRC should not have problems paying its rent. This can be seen with the low number of delinquencies:

During the Covid-19 pandemic, when eviction protections for residents were in place, the number of delinquencies rose. In March 2023 there were around 250 delinquencies left in all units, AIRC expects this number to normalize to around 50 delinquent renters with the end of governmental protections at the close of the year

AIRC maintains an occupancy rate of approximately 95% across all of its eight markets.

Growth opportunities

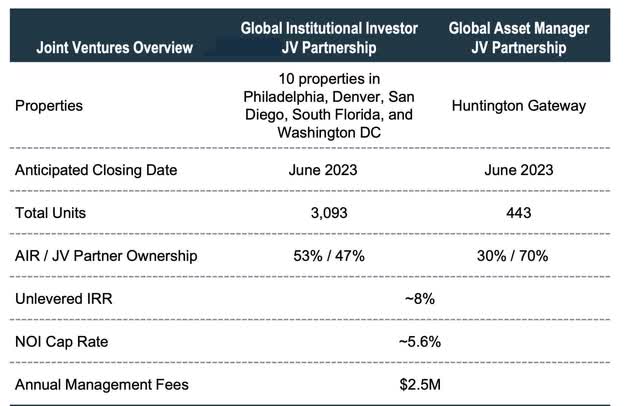

AIRC pursues both internal and external growth strategies. Externally, it has recently initiated two joint ventures with a value of $1.2 billion, comprising over 3500 units.

AIRC – Investor presentation, June 2023

Although AIRC has a 30% stake in the smaller JV, it will obtain half of the cash flow generated by the 443 units. It also has two older joint ventures with a combined gross asset value of $2.9B and approximately 5800 units.

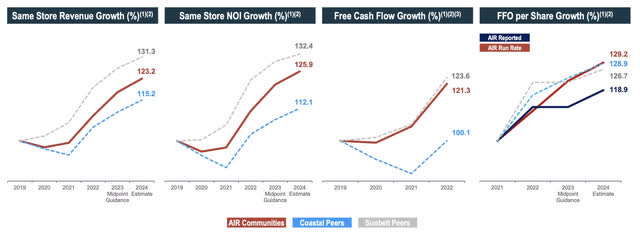

Internally, the company has seen moderate growth since its inception in 2019, with a revenue growth rate of approximately 8.5% since then. It was slower than that of its sunbelt peers Camden Property Trust (CPT) and Mid-America Apartment Communities (MAA), but it is forecast to accelerate and even outperform sunbelt and coastal peers in 2023 and 2024, with a guidance of 8.0% in 2023 and 4.3% in 2024 respectively. The company sees AvalonBay Communities (AVB), Equity Residential (EQR), Essex Property Trust (ESS), and UDR, Inc. (UDR) as its coastal peers.

AIRX – Investor presentation, June 2023

A reason for the estimated growth is also the low increase in operating expenses in the last couple of years. If we look at the same-store operating expenses – excluding taxes, insurance, and costs for utilities – then AIRC had nearly the same costs as five years ago (with less than a 1% increase). In the first quarter of 2023, the costs even declined 20 bps compared with Q1 2022.

Combined with the increase in lease revenues this has led to quite promising growth in FFO since 2020, where the given FFO in 2023 is the mid-point estimate. FFO is expected to be approximately 40% higher than it was in 2020.

Valuation

Debt

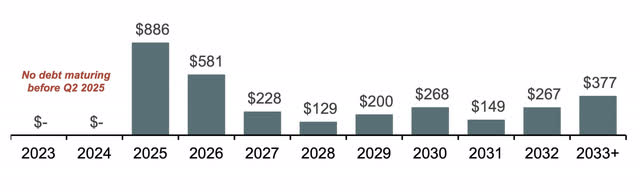

AIRC maintains an investment-grade Standard & Poor’s rating of BBB (Moody’s: Baa2) and managed to reduce net debt to adjusted EBITDA to 5.9x.

I see very little risk from these debt levels. Also, in 2023 and 2024 AIRC has no debt to repay. With the current available liquidity of over $2 billion, AIRC could repay all debt due through 2027, as can be seen in the chart below. It intends to allocate proceeds from its joint ventures toward repaying a quarter of its 2025 debt.

AIRC – Investor presentation, June 2023 (in $M)

Furthermore, only 4% of the debt is exposed to floating rates, and the weighted-average interest rate of all leverage stands at 4.0%.

Discount to net asset value

In June, AIRC traded at an 18.3% discount to net asset value. This discount has expanded since then because the share price has been slightly down since the beginning of June. This discount is slightly higher than that of its peers, with a 17.9% discount for coastal peers and a 17.6% discount for sunbelt peers, according to the investor presentation from June 2023.

Last year AIRC used $317 million of its balance sheet to repurchase shares. This converts to an average price per share of $39.5, which was approximately 15% higher than the share price today. The share repurchases continue in 2023, as the number of shares outstanding has decreased in 2023 by approximately one million.

Dividend and price-to-FFO ratio

AIRC offers an annualized dividend of $1.80, translating to an attractive dividend yield of 5.5%, which may be appealing to income-oriented investors. The dividend yield is significantly higher than that of its peers. The dividend growth has been modest since AIRC’s inception in 2019, with two increases of 1 cent per quarter.

Additionally, AIRC trades at an attractive price-to-FFO ratio compared to its peers. I have compared AIRC to its sunbelt and coastal peers, as AIRC has listed, for example, in its investor presentation from June 2023, and which I have also listed above. The data points for the peers were extracted from Seeking Alpha’s summary pages.

|

AIRC |

AVB |

CPT |

EQR |

ESS |

MAA |

UDR |

|

|

Dividend yield |

5.50% |

3.71% |

3.81% |

4.18% |

3.95% |

3.96% |

4.40% |

|

Price/FFO |

13.72 |

16.83 |

15.28 |

16.67 |

15.6 |

15.38 |

15.29 |

I think it’s quite interesting, that all peers trade at a similar Price/FFO and a comparable dividend yield. With the above-described improvements of its portfolio and the growth prospects in 2023 and beyond, I see no reason for the discount to its peers and therefore rate AIRC as a buy. With a 10% increase in price/FFO, AIRC would trade close to its peers with the lowest price/FFO. Also considering the dividend, I see a high probability of a one-year return of at least 15% with AIRC.

Recent results

AIRC reported Q2 earnings at the end of July. In this quarter it achieved an FFO per share of $0.58 and provided guidance for Q3, expecting FFO to be in the range of $0.61 to $0.64. Notably, same-store net operating income grew by 10.6% in a year-over-year comparison and by 1.8% when compared to Q1. As mentioned earlier, the debt is mostly fixed-rate and the operating expenses have only increased slightly in recent years, implying that increases in net operating income will translate into higher FFO. This trend is also reflected in the same-store net operating income (NOI) margin, which stood at 74.2% in Q2.

AIRC also stated how it plans to utilize a portion of the proceeds from the newly established joint ventures, which amounted to $554 million year-to-date. It “expects to use the balance of proceeds to purchase properties, now in advanced negotiations, with current returns neutral to 2023 FFO and $0.01 accretive to 2024 FFO, with long-term unlevered IRRs in excess of 10%.” An IRR (internal rate of return) of 10% is generally considered a good rate of return.

AIRC maintains an occupancy rate of approximately 95%, though this rate has dipped by approximately 200bps compared to Q1 2023, due to increased evictions and usually lower summer occupancy rates. Compared to Q2 2022 the occupancy rate is down just 1.1%.

Furthermore, the Q2 earnings report also included a narrowing of guidance for the full year 2023: Compared to 2022, AIRC now expects revenue growth between 7.8% and 8.6%, predicts higher expenses in the range from 5.0% to 5.6% and anticipates NOI to be 8.6% to 9.8% higher.

Risks

While demand for rental housing is typically quite resistant during a recession, multi-residential REITs are not immune to economic downturns. If there is a recession before long, tenants may face job losses, making it hard for them to pay rent obligations. This can lead to lower occupancy rates and therefore lower rental income for AIRC. Of course, also changes in demand can affect occupancy rates and rental income. The demand for apartments can shift based on different factors such as demographic trends, population growth, or local economic conditions. Although the operating expenses were astonishingly low in the last quarters, there is no guarantee this could not change in the coming years. With the current dividend and the estimated FFO for 2023, the payout ratio will be close to 75%. Given this moderate payout ratio, I perceive no imminent risk for a dividend cut in the near future.

Conclusion

In my view, the improvement of AIRC’s portfolio quality and FFO growth have not yet been reflected in its share price. With a low price-to-FFO ratio and a high dividend yield compared to peers, I think AIRC presents an attractive investment opportunity in a promising sector.

Read the full article here