Venture-focused business development companies like Horizon Technology Finance (NASDAQ:HRZN) have seen strong valuation resets since March.

BDCs like Horizon Technology Finance sold off in March following the disaster that engulfed Silicon Valley Bank, which had a substantial focus on venture-backed companies. Since then, Horizon Technology Finance’s valuation has fully recovered up until August before dropping again more recently in light of broader market weakness.

Since Horizon Technology Finance is no longer selling at a discount to net asset value and since I see more value for passive income investors with TriplePoint Venture Growth (TPVG), I modify my stock rating on HRZN to neutral/hold.

Downgrade Motivation

I aggressively doubled down on HRZN in March around the time Silicon Valley Bank collapsed. For the downgrade, I have two reasons:

- Since March, Horizon Technology Finance’s valuation has changed from a discount to a premium valuation.

- The dollar amount of non-accruals increased compared to the end of the first quarter, which indicates a deterioration of credit quality. As of the end of 1Q-23, Horizon Technology Finance had non-accruals amounting to $5.3 million (based on fair value) compared to $15.3 million in 2Q-23 (also based on fair value).

Niche-Focused BDC With Substantial NII Upside In Rising-Rate Environment

Like its peers, TriplePoint Venture Growth BDC or Hercules Capital Inc. (HTGC), Horizon Technology Finance is a niche BDC that invests primarily in technology, life science and healthcare companies. Horizon Technology Finance primarily takes debt positions in its core industries, but the BDC also makes Equity and Warrant investments that have the potential, if the underlying portfolio company strikes a home run, to boost the company’s net investment income.

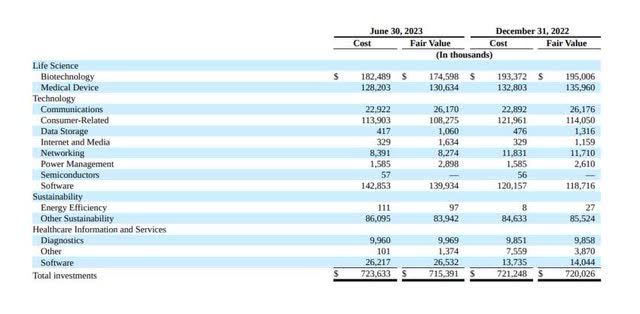

At the end of 2Q-23, Life Sciences were the largest industry in Horizon Technology Finance’s investment portfolio, with Technology ranking second. In total, the BDC owned investments in innovative sectors of the economy worth $715.4 million. 96% of those investments were comprised of debt ($683.9 million) whereas the remainder was mostly made up of Equity and Warrants ($30.8 million).

Investment Portfolio Overview (Horizon Technology Finance Corp)

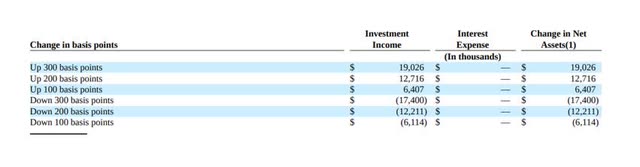

As of June 30, 2023, 95% of Horizon Technology Finance’s debt principal amount was floating-rate, reflecting a decline of 5 percentage points compared to the end of 2022, based on the company’s latest SEC filing. With 95% floating-rate exposure, Horizon Technology Finance is very dependent on the interest rate path set by the central bank and faces attractive prospects for net investment income growth.

If inflation remains high or accelerates again, like it did in July, the BDC, through its portfolio positioning, would probably profit in terms of higher portfolio income, which in turn could lead to a raise in the base dividend or the payment of a special dividend.

According to the BDC’s sensitivity table, a 100% basis point increase would lift its investment income by $6.4 million. As such, Horizon Technology Finance is betting on ongoing interest rate hikes.

Sensitivity Table (Horizon Technology Finance Corp)

Credit Quality And Peer Group Comparison

Horizon Technology Finance had two investments on non-accrual at the end of the second quarter with a fair value of $15.3 million. This translates into a non-accrual ratio of 2.2% (based on the fair value of debt investments).

Hercules Capital had the best credit quality in the peer group, with a non-accrual ratio of 0.0%. TriplePoint Venture Growth BDC had a 4.7% non-accrual ratio as bad loans rose in the second quarter.

Dividend Coverage And Investment Recommendation

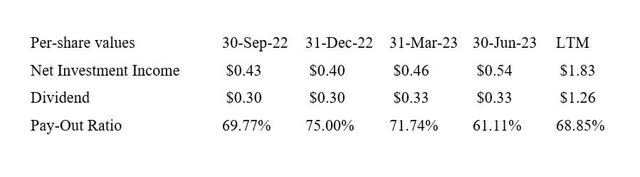

Horizon Technology Finance paid out $0.33 per share per quarter while earning $0.54 per share in net investment income in 2Q-23. This led to a dividend pay-out ratio of 61% in the second quarter and 69% in the last year. The dividend, thus, is well covered by net investment income. All of the following dividend coverage metrics exclude the payment of special or supplemental dividends.

Horizon Technology Finance has good dividend coverage compared to its peers in the venture-backed BDC industry. Hercules Capital had a pay-out ratio of 80% in the last year and TriplePoint Venture Growth BDC paid out 76% of its net investment income in the last twelve months.

Though Horizon Technology Finance has a slightly better pay-out ratio than TriplePoint Venture Growth BDC, I prefer the latter due to its covered 15% dividend yield.

A key feature of Horizon Technology Finance is that the BDC, as opposed to the other two BDCs, pays its dividend on a monthly basis at a rate of $0.11 per share per month. The total dividend pay-out, at a present stock price of $11.95, is 11.05%, and the BDC has already declared $0.11 per share in monthly dividends until the end of the year.

Dividend (Author Created Table Using BDC Information)

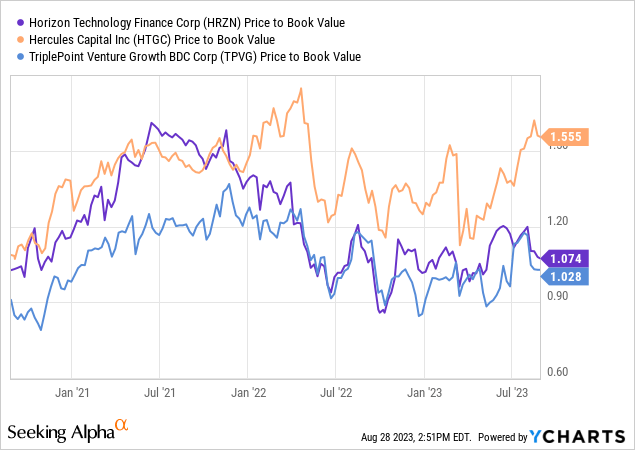

Horizon Technology Finance And BDC Peers Compared In Terms Of Valuation

The motivation behind my rating change is that Horizon Technology Finance is no longer selling at a discount to NAV, which was one reason to buy the BDC as a passive income investor during the March selloff in the stock market.

All three niche-focused BDCs, Hercules Capital, Horizon Technology Finance and TriplePoint Venture Growth BDC, suffered valuation declines in August, however, TPVG now has the lowest NAV multiple in its peer group. HTGC, due to its strong credit quality and distribution history, sells at a substantial premium to NAV.

Why HRZN Might See A Lower/Higher NAV Multiple

Due to its floating-rate exposure, Horizon Technology Finance is vulnerable to the central bank changing its interest rate policy moving forward. An increase in non-accruals, particularly during a recession, would also obviously be a headwind to both the BDC’s net investment income and dividend coverage. Since the dividend is presently well covered by net interest income, I think that the pay-out is safe in the near-term.

My Conclusion

Taking into account that Horizon Technology Finance’s stock no longer has a discount valuation (based on NAV), I adjust my rating accordingly, to neutral/hold.

Horizon Technology Finance covered its dividend with net investment income in the second quarter, but the BDC’s dividend coverage is only slightly better than TriplePoint Venture Growth BDC’s coverage. Though TriplePoint Venture Growth BDC has seen a steep rise in bad loans in the second quarter, TPVG solidly covered its dividend with net investment income in 2Q-23 and offers passive income investors a much higher dividend yield (14.5% for TPVG vs. 11.1% for HRZN).

Horizon Technology Finance has considerable net investment income upside in a rising-rate environment, and the portfolio is growing and performing well, but the valuation is not enticing enough to buy. Hold.

Read the full article here