One of my favorite things about value investing is that, even when the company that you buy stock in experiences weakness, you can still see upside if shares were cheap enough to begin with. One firm that I could point to as an example of this playing out over the past several months is Griffon Corporation (NYSE:GFF), an enterprise that focuses on the production and sale of home and building products like garage doors, rolling steel doors, and more. Thanks in large part to an upward revision from management when it comes to guidance for the 2023 fiscal year, and also thanks to just how cheap shares are, the stock has experienced tremendous upside. The big question now, however, is whether it might make sense for investors to bail and look elsewhere for opportunities. My own view is that, while the ride ahead might be bumpy, and the easy money has been made, there is further upside that still exists from here.

Mixed results are fine in this market

Back in late March of this year, I assigned Griffon a ‘strong buy’ rating. This is incredibly rare for me to do and almost always requires a company that is incredibly cheap and that has other positive attributes to it. These are the companies that I have the most conviction in. And as I have detailed in a prior article, my track record with companies assigned this rating tends to be quite positive. In that particular article, I lauded the company for its financial performance leading up to that point. I also parroted management’s expectation that further growth should be seen in 2023. Add on top of this the fact that shares of the business looked cheap, and I could not help but to rate the firm what I did. Since then, the company has exceeded even my own expectations. While the S&P 500 is up 13.1%, shares of Griffon have seen upside of 43.5%.

Author – SEC EDGAR Data

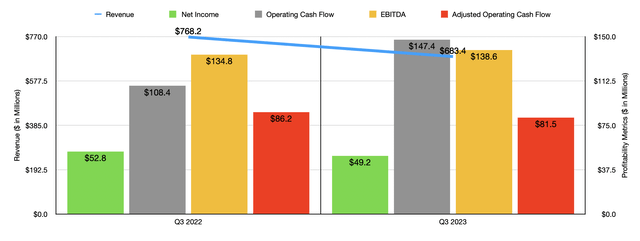

Given this massive disparity between the broader market and shares of Griffon, I could understand somebody thinking that financial performance for the business has been very strong. But that wouldn’t be entirely accurate to say. In some respects, for instance, Griffon has actually seen weakness in its reported data. Revenue during the third quarter of this year, as one example, came in at $683.4 million. That represents a decline of 11% compared to the $768.2 million management reported one year earlier. This weakness was driven largely by the Consumer and Professional Products segment of the company. Sales here dropped 22% from $362.6 million to $282.3 million. This was driven by a 22% reduction in volume across all of the channels and geographies that the company operates in.

The drop associated with its Home and Building Products segment was a far more modest 1%. However, that is because the commercial side of the company reported a 4% product pricing and product mix improvement. It was the residential side of the company that saw some weakness during this time. Sales there dropped about 6.8% year over year, falling from $238.4 million to $222.1 million.

With this drop in revenue came some mixed bottom line results. Net profits took a small hit, dropping from $52.8 million to $49.2 million. To be clear, this looks at only the after-tax profits from continuing operations. The company did benefit from an increase in its gross profit margin from 33.9% to 40.2%. However, this was offset to some extent by a rise in the firm’s selling, general, and administrative costs from 20.5% of sales to 25.2%. There were other factors as well, such as a gain on the extinguishment of debt that the company realized in the third quarter of last year of $5.3 million. Other profitability metrics didn’t really show any clear trend. As an example, even as profits fell, operating cash flow grew from $108.4 million to $147.4 million. But if you adjust for changes in working capital, you would see a decline from $86.2 million to $81.5 million. Meanwhile, EBITDA managed to tick up slightly from $134.8 million to $138.6 million.

Author – SEC EDGAR Data

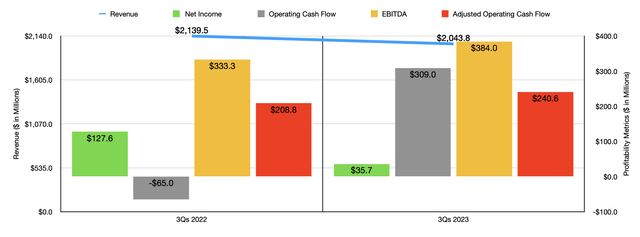

The pain that management reported for the most recent quarter played a significant role in bringing overall revenue for the first nine months of the year down compared to the same time last year. This can be seen in the chart above. Profitability metrics, however, were mostly higher year over year. The one big exception was net income, which dropped from $127.1 million to $35.7 million. But this was driven by a $100 million impairment charge that the company recognized earlier this year.

If you follow Griffon closely, then you likely know that the housing market is in an interesting state at the moment. Backlog amongst home builders has plummeted over the past 12 months. In fact, it was weakening even before that. Concerns about that space certainly impacted shares of our prospect. However, as I detailed in two recent articles, like the following one here, some companies in the homebuilding market are showing signs of turning around. Even though inflation and interest rates are both lofty, there’s no denying that we have a housing shortage of around 3.8 million properties across the nation. Add on top of this the fact that homebuilding prices are dropping to some extent, and it should come as no surprise that management believes that the picture will improve from here.

Author – SEC EDGAR Data

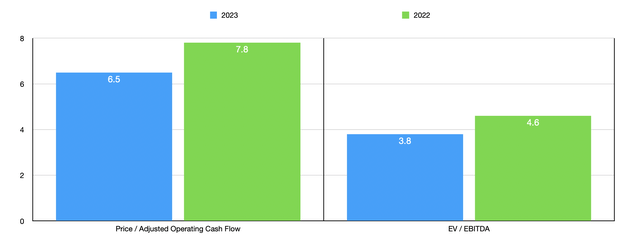

I say this because, according to the company, the expectation for the 2023 fiscal year is for EBITDA to come in at around $550 million. Previous guidance had this metric coming in at ‘at least’ $525 million. Based on these estimates, adjusted operating cash flow for the firm should be around $348 million this year. Taking these estimates, I was able to create the chart above. In it, you can see how shares are priced on a forward basis and how they are priced using data from 2022. In the table below, I also valued the company against five similar firms. Using both the price to operating cash flow approach and the EV to EBITDA approach, I found that Griffon was the cheapest of the group.

| Company | Price / Operating Cash Flow | EV / EBITDA |

| Griffon Corporation | 6.5 | 3.8 |

| Gibraltar Industries (ROCK) | 10.7 | 14.2 |

| Janus International Group (JBI) | 11.9 | 8.2 |

| PGT Innovations (PGTI) | 9.7 | 9.6 |

| Tecnoglass (TGLS) | 14.5 | 5.3 |

| Apogee Enterprises (APOG) | 7.3 | 7.4 |

In addition to the stock being cheap, another boon for the business has been management’s decision to buy back stock. So far this year, management repurchased 2.5 million shares for roughly $85.4 million. That translated to approximately 4.4% of all outstanding stock at that time. The company currently has $172.6 million remaining under its share buyback program that had been upsized in April of this year. Given how cheap the stock is, I applaud this move. And that is saying a lot, because I tend to not favor share buybacks, opting instead for investment in future growth.

Takeaway

Operationally speaking, Griffon has seen some weakness. However, the company is still holding up well and the market has rewarded its performance with a substantial increase in share price. If we assume that management is correct in their assessment, however, the stock still looks incredibly cheap. This is true both on an absolute basis and relative to similar firms. Given these facts and the fact that the company also has virtually no debt and $151.8 million in cash on its books, and I cannot help but to remain bullish. I would argue that the easy money has been made. But given how cheap the stock is, I do feel comfortable assigning the company a solid ‘buy’ rating at this time.

Read the full article here