Note: All amounts discussed are in Canadian Dollars

On our last coverage of Diversified Royalty (TSX:DIV:CA) (OTCPK:BEVFF), we gave a neutral rating to the common shares and suggested investors go a little higher in the capital chain to make things smoother for returns.

With the current payout ratio and the likelihood of BMO taking over Air Miles, we see the company continuing with steady payments, even through a likely recession. That said, the debentures are still the safest and the best bet. The yield to maturity is at about 7.83% and that is for the debentures maturing in about 4.25 years. We think that is where we will continue to make our stand and escape the volatility of the common shares.

Source: Air Miles Drama Does Not Derail The Thesis

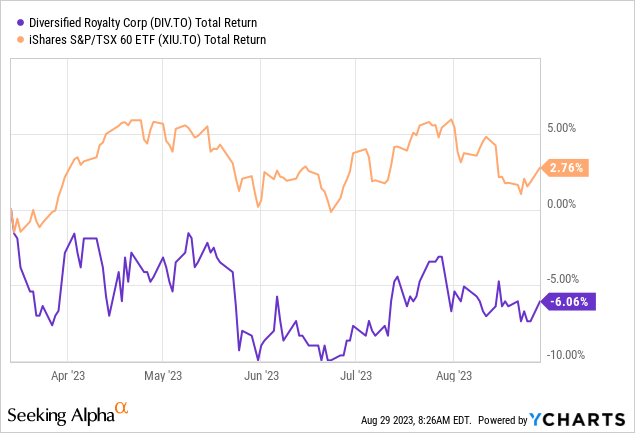

Since the common shares have underperformed the TSX by a solid margin. So sitting out did not cost us one bit on that front.

The debentures we discussed have edged a bit lower with a flattish total return (down 1.5%). But that slight downdraft alongside less time left to maturity has pushed the yield to maturity up to 9.4%! Let’s see if we can double down on our previous play or gravitate towards the common shares in light of the Q2-2023 results.

Q2-2023

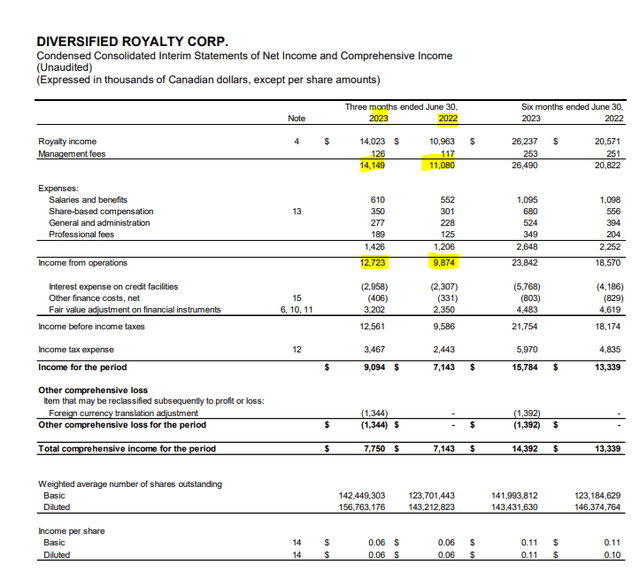

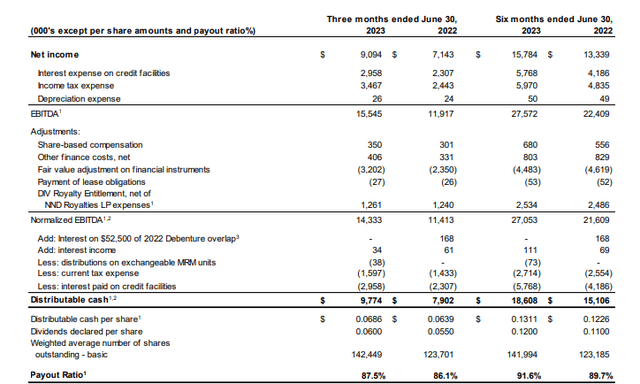

Q2-2023 was the strongest quarter in the company’s history for year over year revenue growth. Top line grew by 27%. Operating expenses were up sharply as well, but lagged revenue growth and came in at an 18% clip.

DIV Q2-2023 Financials

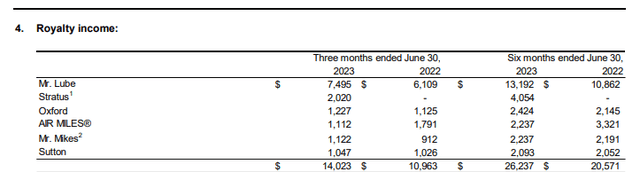

This resulted in operating income moving up 29%. Within the individual royalty plays, we saw that Mr. Lube was the big star and showed a 22% increase in revenues driven by price increases and expanded offerings.

DIV Q2-2023 Financials

Oxford Learning Centers generated same store sales growth of 8.6% in Q2 2023 on a constant currency basis. There has been a steady transition to in-person tutoring over the last several quarters, and this segment is slowly clawing back above pre-COVID-19 levels. Air Miles was the only segment that fell as Sobey’s exited the plan and Bank of Montreal (BMO) took steps to transition the brand under its control. Mr. Mikes restaurant pool delivered another strong quarter with a 23% overall increase. Sutton, which is a fixed royalty structure, generated a slightly higher revenue number from the annual price hike. Finally, Stratus was responsible for the bulk of the year-over-year delta, as this partner was acquired in November 2022.

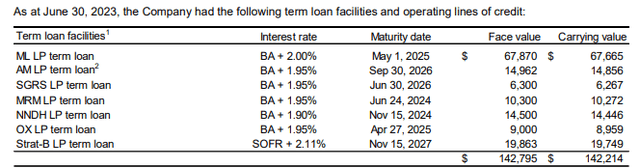

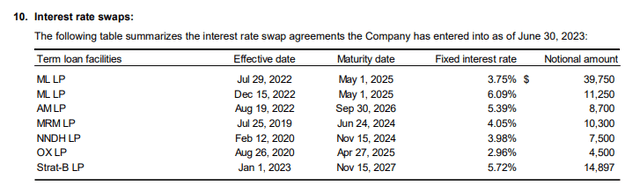

From a risk perspective, Diversified’s interest coverage remained almost identical year over year. How did that happen despite such powerful top-line performance? Well, the Stratus purchase was financed with both equity and debt and that increased finance costs quite a lot. Further, as can be seen below, Diversified has hitched its fortunes on variable rate debt. The bulk are tied to the Banker’s Acceptance Rate, while the new entrant is tied to SOFR.

DIV Q2-2023 Financials

To the company’s credit, there are some locks/hedges in place via interest rate swaps. But this only applies on about 70% of the total.

DIV Q2-2023 Financials

Outlook

It is hard to overstate how good the company’s performance metrics have been over the past 12 months. Being attached to top-line growth has meant that the company has bypassed the margin compression we saw in many other industries. Its own costs have gone up, but considering the addition of Stratus and general inflation levels in Canada and US, this has been at an acceptable rate. If you have to ding it for anything, it would be the higher than necessary variable interest rate exposure. Even adjusted for the hedges (which start running out in 2024), this is still a weak spot for an otherwise strong company. The counterpoint, well interest coverage is still near 4.0X. That is not weak by any stretch of the imagination.

On the dividend front, the company has navigated the very high payout ratios of 2020 and 2021 and is now comfortably in the green.

DIV Q2-2023 Financials

The 8.5% yield looks well covered and we think the metrics will show some further improvement in 2023. The company is trading at a 9.2% free cash flow yield, which is arguably inexpensive, considering the lower volatility royalty model. This model has also got more “diversified” with the addition of Stratus. Still, the numbers are not that appealing here especially considering our primary alternative.

Verdict

Diversified has become a stronger company over the last two years. It has also shown the resilience of its model to inflationary pressures. The dividend yield is appealing at present, but overall valuation is still not compelling.

Now your mileage may vary (especially if you use their Mr. Lube service for oil changes), if you believe that interest rates are about to collapse. But as it stands with risk-free rates at near 5%, the valuation still rings in at only average levels.

The debentures are another matter altogether. Set to mature on June 30, 2027, they have an yield to maturity of 9.45% at the price of $90.01.

TMX

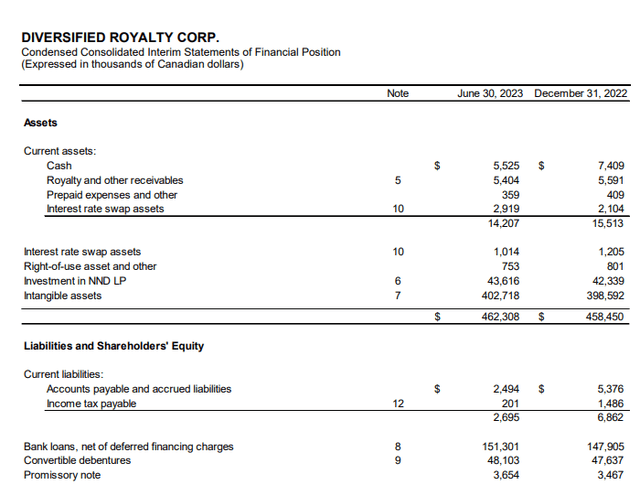

Total liabilities are around $200 million and expected normalized EBITDA should be close to $50.00 million in 2024.

DIV Q2-2023 Financials

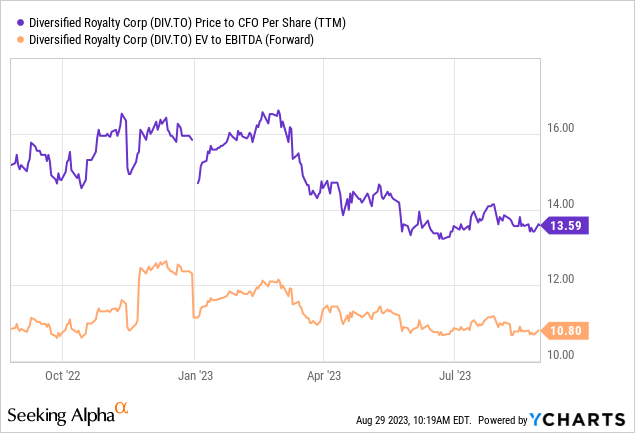

So debt to EBITDA is 4.0X and you have to ask yourself whether you think at least a 4.0X EBITDA multiple makes sense for those business. That answer is of course a strong “yes”. Currently, as shown a little higher up in the article, the EV to EBITDA multiple is near 10.0X, but by buying the debt you just need to it be worth more than 4.0X to have a safe investment. We really like the debentures here and will allocate some additional money over the next few months.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here