Chinese electric vehicle maker XPeng (NYSE:XPEV) announced on Sunday that it was acquiring DiDi Global (OTCPK:DIDIY)’s smart vehicle unit which could potentially result in XPeng moving faster into high-volume production of electric vehicles. XPeng only recently announced a $700M investment/collaboration partnership with German car brand Volkswagen which is meant to share development costs and risks. The latest deal with DiDi Global could help XPeng expand its leadership position in the autonomous vehicle market, on one hand, but also includes risk as XPeng is set to launch a new EV brand in FY 2024. I am going to discuss the pros and cons of the deal between XPeng and DiDi Global and explain why I am not yet ready to change my rating to buy, despite shares soaring after the deal announcement!

Changing brand strategy, pros and cons of the XPeng-DiDi Global deal

According to the disclosed deal terms, DiDi Global will sell its smart vehicle unit to XPeng for $744M and XPeng said that it will, using DiDi Global’s mobility ecosystem, build a Class-A electric vehicle under a new brand name in FY 2024. By doing this, XPeng is set to target the low-price EV market segment in which it hopes to achieve mass production capabilities and to expand its leadership position in autonomous vehicles.

I believe the deal has both positives and negatives, meaning the deal is exclusively a good thing for XPeng shareholders. On the positive side, XPeng has the opportunity to expand its leadership position in autonomous driving technology, especially now that the company brought to market the G6 coupe sport utility vehicle which is a direct competitor to Tesla’s Model Y and which is equipped with XPeng’s self-driving technology. The outfitting of its EVs with self-driving technology could translate to a competitive offer for buyers of an XPeng electric vehicle, especially because Tesla’s sell-driving tech is not available in China.

Only in the second-quarter did XPeng announce that it was piloting full self-driving tests in Beijing for some of its electric vehicle models, including the P7, G9 and P5. Earlier this year XPeng launched its advanced driver assistance system, called XNGP, which is the equivalent of Tesla (TSLA)’s Full Self-Driving (FSD), in cities such as Guangzhou, Shenzhen and Shanghai. Tesla’s FSD is not available in China and companies that offer such technology, like XPeng, have a major competitive advantage over manufacturers that don’t offer such features. XPeng aims to roll out its advanced driver assistance system to all drivers of a XPeng vehicle (through software updates) by the end of FY 2024.

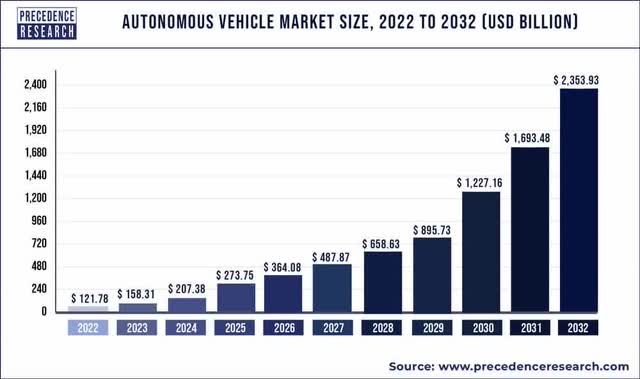

The autonomous driving market is set for strong growth in the next ten years which could give companies like XPeng an accelerant for growth. The global autonomous vehicle market is expected to see strong growth as AD technology matures and appears set to reach mass market potential in the near to medium term. The autonomous vehicle market is expected to grow from $122B in FY 2022 to $2.4B in FY 2032 which represents an implied annual growth rate of 34% over the next ten years. In total, the autonomous vehicle market is expected to grow by a factor of 10X over the next decade… which helps create a massive opportunity for XPeng which has invested heavily into its own self-driving tech.

Source: Precedence Research

While XPeng could profit from the acquisition of DiDi Global’s smart vehicle unit, the launch of a new low-price EV brand is a separate issue and comes with considerable risks, in my opinion.

XPeng seeks to enter the market with a low-price EV (below 150 thousand Chinese Yuan) under a new brand name in FY 2024 which may increase volume, but may also weigh on average sales prices and margins as a result. Additionally, the entry into the low-margin mass market represents a change in EV strategy for XPeng which comes at a time when producers of EV vehicles are struggling with eroding pricing power.

XPeng’s margin situation is deteriorating and the EV manufacturer reported a negative vehicle margin of 8.6% in Q2’23. While XPeng is planning to adopt a high-volume strategy in its new EV segment, given the low price sticker as well as deteriorating pricing environment, I believe investors can be less hopeful of a major margin improvement following the announcement of the XPeng-DiDi Global deal.

XPeng’s valuation: best to sit on the sidelines for now

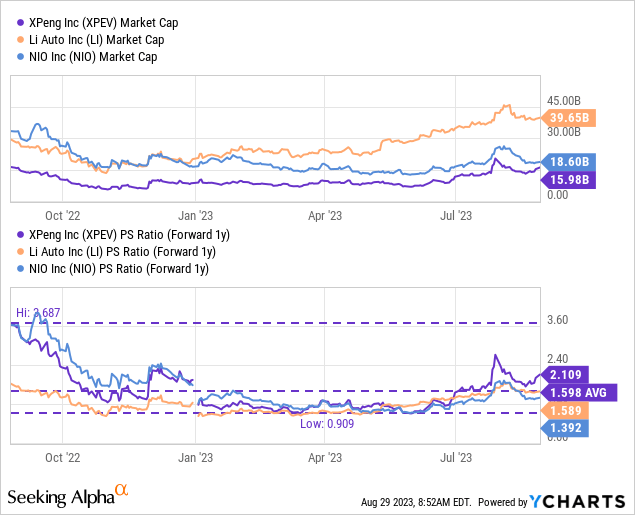

XPeng’s shares soared after the EV maker reported the deal with DiDi Global, but from a valuation perspective I would not recommend buying XPeng… for reasons I already stated: XPeng has fallen behind its direct EV rivals in China regarding delivery growth and the margin situation is not resolved yet. Additionally, XPeng appears rather expensive when compared against EV makers with stronger delivery achievements.

As a result, I would recommend investors to stay on the sidelines following the DiDi deal and potentially wait for a correction that improves XPeng’s relative valuation metrics. While XPeng still has the lowest market cap in its industry group, the company remains the most expensive of the three Chinese EV makers with a P/S ratio of 2.1X.

I believe investors would consider buying/adding to XPeng (and changing my rating) if the share price drops to ~$12 which is when the firm’s revenue prospects are valued in-line with its historical P/S average of 1.6X.

Risks with XPeng

The biggest risk for XPeng does not relate to missing out on the opportunity in the autonomous vehicle market in China. Rather, I see a much bigger risk with regard to the company’s vehicle margin trend which has significantly deteriorated in the second-quarter and the launch of a new low-price, low-margin EV brand may only help to compound this problem. If XPeng fails to turn things around in terms of vehicle margins, the company may have a harder time convincing investors that it can mass-produce electric vehicles profitably.

Final thoughts

The XPeng-DiDi Global deal allows XPeng to fortify its position in the Chinese autonomous vehicle market and the company’s ambition to bring its advanced driver assistance software to all Chinese cities by 2024 is an ambitious goal that improves XPeng’s appeal to prospective electric vehicle buyers, especially with Tesla’s FSD not being available in China.

While I very much like the deal with DiDi Global from an autonomous driving point of view, the strategy in the entry-EV market segment indicates that margin pressures are likely to remain high… and this is the reason why I believe the market overreacted to the deal announcement this week. For those reasons, as well as the fact that XPeng’s valuation remains high relative to its EV rivals, I reaffirm my hold rating following the XPeng-DiDi Global deal and believe investors should wait for a drop before buying shares in the EV company!

Read the full article here