Investment Thesis

The Stem, Inc. (NYSE:STEM) business model is to layer artificial intelligence (“AI”) with energy storage solutions so that the grid is able to operate with other energy supplies aside from baseload supply.

In plain English, this means that its customers can actively choose to get their energy supply from other energy sources aside from coal and natural gas.

The problem for Stem is that, aside from the fact that the need for energy security has faded away from the market’s narrative, to complicate matters further for Stem, it’s burning through significant cash flows while its balance sheet surfaces more questions rather than providing investors with a sense of ease.

This is a mixed-bag investment. Yet, I remain bullish for now, as I believe that most, if not all, of these negative considerations are already in the share price. In fact, certainly, investors’ expectations can’t be that high, after all the stock is already down nearly 70% over the past 12 months and its multiple has compressed from 6x forward sales down to just 1x forward sales.

Why Stem? Why Now?

Stem provides clean energy solutions. Stem offers an array of products and services, including energy storage systems, edge hardware for data collection and real-time control, and an advanced AI platform called Athena.

Athena optimizes the operation of integrated energy storage and solar systems, helping customers reduce energy costs and increase grid reliability. Stem also monitors solar assets through Athena’s PowerTrack application.

Moving on, Stem operates in two key areas: Behind-the-Meter for on-site energy generation and storage, aiding commercial and industrial customers in reducing energy bills and meeting environmental goals, and Front-of-the-Meter for grid-connected systems that contribute to dynamic energy markets, enhancing the value of renewable energy projects. Their mission is to maximize the economic benefits of energy assets while ensuring resiliency, making them an important player in the clean energy transition.

During their recent earnings call, Stem announced a significant energy storage project with Ameresco, a 313-megawatt-hour installation, demonstrating their competitiveness in large-scale front-of-the-meter storage deployments. This contract win will come into service in 2024.

As you can see, on the surface, there’s a lot to like from Stem. But as we dig into its financials a different image surfaces, one which short sellers have been quick to highlight.

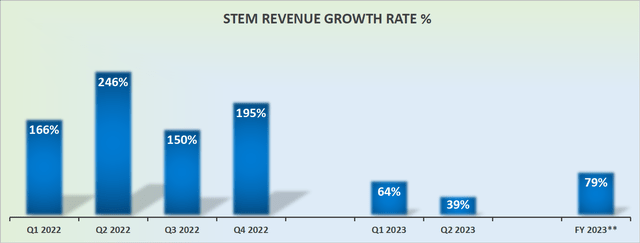

Revenue Growth Rates Slow Down

STEM revenue growth rates

Stem’s revenue growth rates this time last year could be counted on for triple-digit growth rates. Today’s growth rates are on a path to approximately half this growth rate.

Naturally, investors are concerned that Stem’s growth rates could continue to slow down into 2024. If that were the case, what would have looked at one point as a truly revolutionary energy solution company, would soon be seen as a flash in the pan where its best growth days are already long ago in the rearview mirror. Accordingly, if investors come to believe that its best growth days are now in the rearview mirror, this would have an impact on the multiple that investors would be willing to pay for its ongoing prospects. More on this matter soon.

We’ll first turn to discuss Stem’s profitability profile.

Gross Margins Are Not Scaling Higher

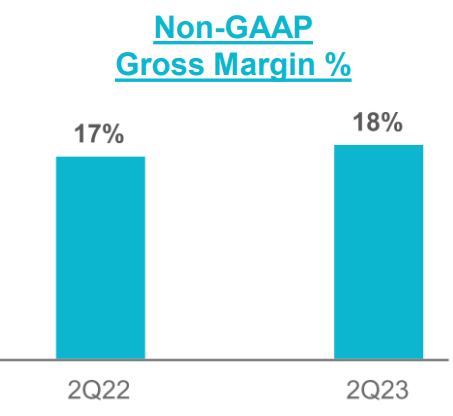

On the one hand, investors can point to Stem’s non-GAAP gross margin expanding slightly from the same period a year ago.

STEM Q2 2023

As you can see above, Stem’s non-GAAP gross margins increased by 100 basis points. That’s obviously a positive, but when we observe that in Q1 of this year, Stem’s non-GAAP gross margins were 19%, this implies a sequential compression in Stem’s gross margins.

Put another way, if earlier in 2023 investors held some hopes that Stem could perhaps become a low 20% non-GAAP gross margin business, its Q2 2023 earnings temporarily put a stop to that line of thought.

To recap, it looks like not only are Stem’s growth rates decelerating, but the attractive possibilities that may benefit from a stronger revenue base translating into greater scale, which could result in higher gross margins, appear to have come to a standstill for the time being.

Further, not only do investors have to weigh up all these considerations, but Stem’s balance sheet isn’t exactly rock solid. Stem consistently declares that it will exit 2023 with at least $150 million of cash and equivalents, as the second half of 2023 will see an improvement in its receivables and more controlled use of cash.

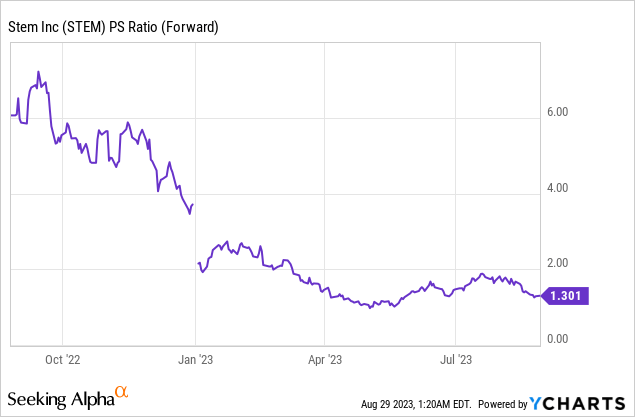

Finally, as I’ve already alluded to earlier, investors’ expectations have already rerated lower. Twelve months ago investors were more than willing to pay more than 6x forward sales for Stem. Today investors are asked to pay 1x forward sales. Meaning that the time to get bearish on Stem has already come and gone.

What’s left is a company with a more attractive risk-reward balance, even though I recognize that this investment thesis is not blemish-free.

The Bottom Line

Stem’s business model combines AI technology with energy storage solutions, allowing customers to choose cleaner energy sources beyond coal and natural gas. While there are concerns about fading interest in energy security and Stem’s cash flow situation, I’m cautiously optimistic, considering these challenges appear to be priced into the stock, which has already declined significantly over the past year.

Stem offers clean energy solutions, including energy storage systems, real-time control hardware, and the AI platform Athena. Their mission is to maximize energy asset economic benefits while ensuring reliability, making them a key player in the clean energy transition. Recently, they won a substantial energy storage project with Ameresco, demonstrating their competitiveness in large-scale energy storage.

However, Stem faces challenges, including slowing revenue growth rates and margin compression. The stock’s valuation has declined, suggesting more realistic expectations. While there are concerns, Stem’s risk-reward balance appears more attractive now, despite some imperfections in the investment thesis.

Read the full article here