HEICO Corporation (NYSE:HEI) just released its fiscal third quarter earnings. At the time of writing, the stock is down around 6%. After-hours activity is not always a strong indicator of the market hours reaction, but it is still interesting to discuss the results and see whether there is any justification for the lower after-hours prices.

About HEICO Corporation

For those unfamiliar with HEICO Corporation, I have sourced the company description from our in-house developed evoX Financial Analytics tool.

HEICO Corporation is a manufacturer of jet engine and aircraft component replacement parts. The Company operates through two segments: Flight Support Group and Electronic Technologies Group. The FSG segment consists of HEICO Aerospace Holdings Corp. and HEICO Flight Support Corp. and their subsidiaries. The FSG segment designs and manufactures jet engine and aircraft component replacement parts. In addition, the FSG segment repairs, overhauls and distributes jet engine and aircraft components, avionics and instruments for domestic and foreign commercial air carriers and aircraft repair companies, as well as military and business aircraft operators. The ETG segment consists of HEICO Electronic Technologies Corp. and its subsidiaries. ETG segment designs, manufactures and sells various types of electronic, data and microwave, and electro-optical products, including infrared simulation and test equipment, laser rangefinder receivers and electrical power supplies.

Does HEICO Pay A Dividend?

HEICO currently pays a dividend of $0.10 every 6 months, with 6 years of consecutive dividend increases with a 22% CAGR on the total return. Currently, the 0.12% dividend yield is not quite attractive, but its 22% CAGR over the past 30+ years certainly is.

HEICO Corporation

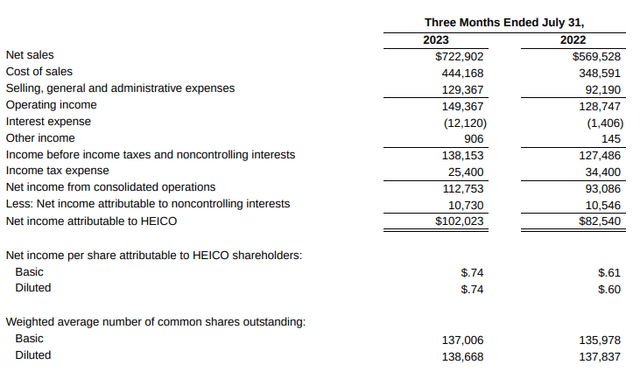

HEICO booked $722.9 million in sales, up 27% and beating analyst estimates by $15.9 million. Sales in FSG were up 22.6% while ETG sales growth was up 33.4%. What has disappointed investors was the operating income which grew only 16% driven by 40% higher selling, general and administrative expenses and 27% higher cost of sales. The cost of goods and services were in line with revenue growth, and it was the higher SG&A that eroded pressured the operating income.

It seems that the margins are the only thing that could have been somewhat disappointing to investors in the third quarter results, but they also portray the reality of the industry, so I am not quite sure whether that should really catch investors by surprise.

Furthermore, it should be noted that the Flight Support Group saw its margins strengthen from 21.4% to 22% on demand strength for commercial aerospace products and services as air travel continues to grow. It was the Electronic Technologies Group cost of goods and services and SG&A that provided the headwind with sales being a third higher but operating income being only 9% higher and that pressure will linger it seems as the company warned of inflationary pressures and supply chain issues pushing material and labor costs higher.

The results were not bad, but primarily on the weak end in the ETG business, but it likely was the warning of the sticky items on costs that set the share prices lower.

HEICO Stock Price Valuation: A Difficult Story

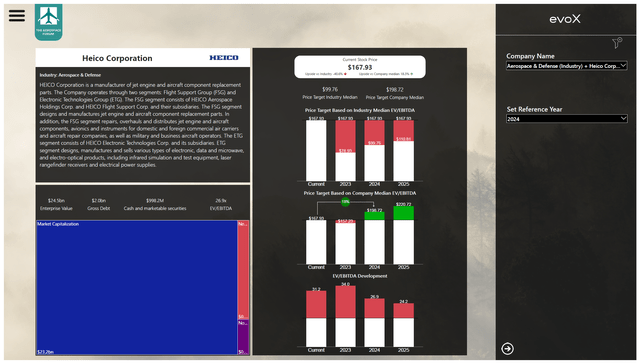

I am impressed with HEICO’s CAGR and the company has a good track record of acquiring and integrating companies, so its recent acquisition of Wencor should be a net positive. So, what makes the valuation difficult? The answer is quite simple: The current EV-to-EBITDA. Using the current EV-EBITDA, I would put the price target at $194.60 providing 16% upside which is lower than the CAGR of 22% but still quite good.

Valuation HEICO Corporation using evoX Financial Analytics (The Aerospace Forum)

Usually I use the 10-year median EV-to-EBITDA to determine any upside for a stock and that is where the issue arises for HEICO is that it is a company that fuels its growth to a significant extent by mergers and acquisitions and integration in those companies benefiting from the organic growth of the industry.

Around 2016, the EV-EBITDA has started expanding, and I also observed that HEICO has purchased 49 companies, of which 23 in the past five years. So, instead of working with the 10-year EV-EBITDA for HEICO, I have used the 7-year figure, which provides around 18% upside. We also see that the company is overvalued with the industry median in mind, but that I would think that is driven by the M&A strategy the company pursues.

If HEICO stock indeed opens lower following its third quarter report, that could open up an opportunity for investors to buy the dip and acquire HEICO stock at more or less fair value with 25% upside.

Conclusion: Lower Stock Price Could Offer Entry Point

HEICO Corporation has an almost permanent premium compared to peers, which I would attribute to its growth strategy focused on M&A coupled to organic growth of the industry with relatively low debt. The Q3 2023 results did include some margin pressure and wording in the press release suggest that these pressures are sticking, but overall I do believe that the company does offer value. It is not a great investment if you look for a nice dividend yield with yield on cost significantly improving year-over-year, but its complete business approach does offer value for shareholders.

Read the full article here