August 28th ended up being a really interesting day for shareholders of both Kimco Realty (NYSE:KIM) and RPT Realty (NYSE:RPT). Shares of the latter shot up, closing up 17.4%, after news broke that the former had agreed to acquire the latter in a multibillion-dollar all-stock transaction. Although the sizes of the two companies are significantly different, the transaction should bring to Kimco Realty some value, even if synergies predicted by the acquirer are not realized. For shareholders of RPT Realty, however, the deal is not as clear a win as it is for investors in Kimco Realty. However, it does come with a benefit of the significant premium over where shares of the business were trading immediately before the announcement. So when you add that into the picture, I would argue that this transaction should be looked upon favorably by both sides of the deal.

A fine transaction, especially for Kimco Realty

According to the press release issued by Kimco Realty, the company had agreed to acquire all of RPT Realty in a transaction valuing the company at around $2 billion on an enterprise value basis. Based on my own calculations, the number is slightly lower than this at about $1.925 billion. But at the end of the day, that’s close enough. The deal in question will involve shareholders of RPT Realty receiving 0.6049 of a share of Kimco Realty for each share of RPT Realty they currently own. Using closing market prices on August 25th, which was the business day immediately prior to the deal being announced, this translates to a price per share of $11.34 for RPT Realty, which works out to a premium of approximately 19%.

Kimco Realty

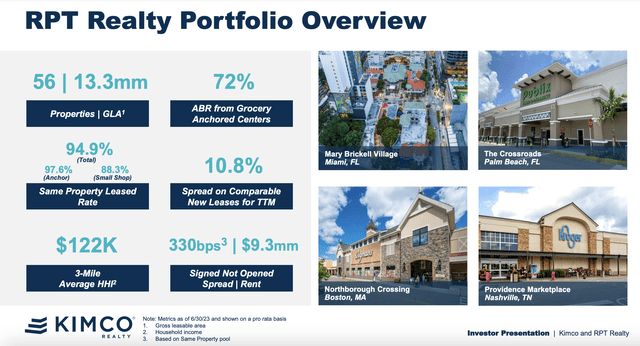

Even ignoring the financial side of the picture, this transaction does make a lot of sense. Both companies have similar assets. The ownership and leasing out of open air, grocery anchored shopping centers. Although there are other assets in the mix as well, such as some mixed-use properties that Kimco Realty owns. Of course, Kimco Realty is significantly larger. As of the end of its most recent quarter, the company had interests in 528 shopping center properties throughout the U.S. market. These were spread across 28 different states and amounted to 90.1 million square feet of grossly stable area. This is on top of another 21 other property interests that come out to roughly 5.5 million square feet. By comparison, RPT Realty has only 56 properties in its portfolio that comprise 13.3 million square feet of space. This covers only the multi-tenant properties that the company has. It also has another 49 properties that are net leased under its RGMZ joint venture. However, the company owns only 6.4% of that venture.

Kimco Realty

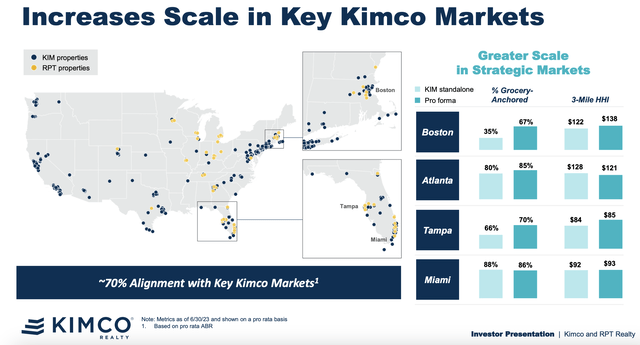

Despite the relatively small size compared to what Kimco Realty boasts, the firms do have some meaningful geographic overlap. Noteworthy locations include Boston, Atlanta, Tampa, and Miami. In fact, the combined company will see its market share of grocery anchored assets expand in three of these four markets as a result of this transaction. What’s more, in three of the four areas, the exposure of the combined business to households with higher levels of income will increase. In Boston, for instance, within 3 miles of a Kimco Realty location, residents have household income of about $122,000 per year. That number should climb to $138,000 thanks to this transaction. In Tampa, we should see an increase from $84,000 to $85,000, while in Miami we should see the figure rise from $92,000 to $93,000.

Kimco Realty

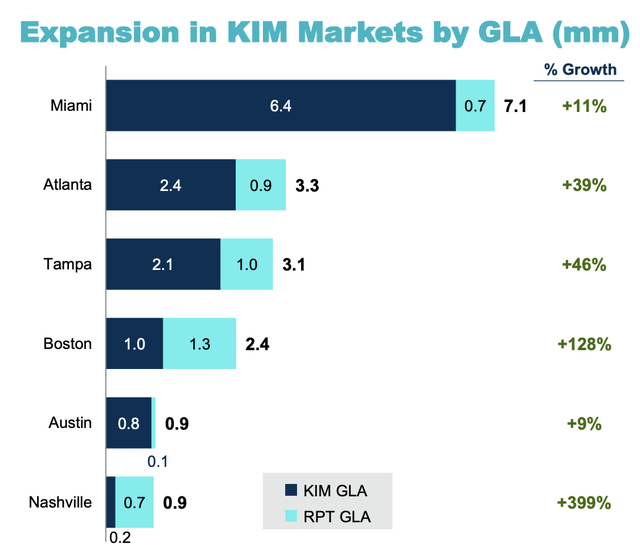

In Miami, gross leasable area for Kimco Realty is expected to rise from 6.4 million square feet to 7.1 million as a result of this purchase. In Tampa, we should see an increase from 2.1 million square feet to 3.1 million square feet. The rise in Boston should be even more impressive, taking the company from only 1 million square feet. And in Atlanta, the rise should be from 2.4 million square feet to 3.3 million.

Of course, these are not the only important markets. Based on the investor presentation released by Kimco Realty, about 70% of properties currently owned by RPT Realty align with key strategic markets that Kimco Realty has identified. This will be instrumental in helping the company to grow and will also lead to cost cutting initiatives. Right out of the gate, Kimco Realty is forecasting annualized cost savings of about $34 million. But there are other benefits on the financial side to this transaction. For instance, the company believes that there’s over $9 million of signed but not open leases and that some of the leases on its books are at rates that are substantially below with the current market demands. We don’t know, however, the full impact this will have on the combined companies top or bottom lines.

Author – SEC EDGAR Data

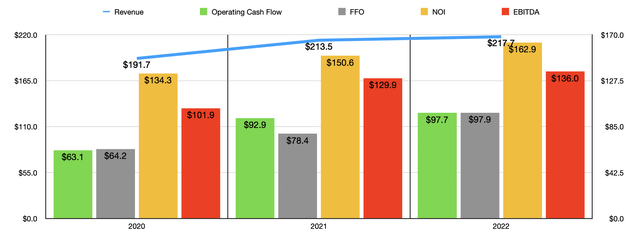

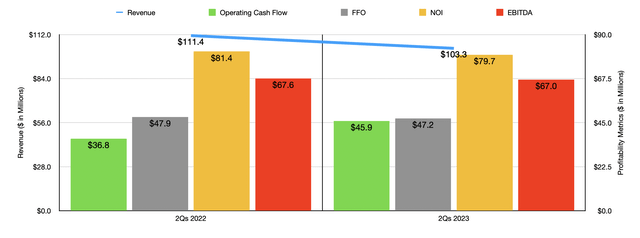

Given how some segments of the retail space have performed in recent years, I can understand why some investors might be wary of Kimco Realty picking up bad assets. However, this does not seem to be the case. Over the three years ending in 2022, RPT Realty did they find job growing the company, with revenue expanding from $191.7 million to $217.7 million. Operating cash flow over this window of time jumped from $63.1 million to $97.7 million. Other profitability metrics have seen a similar increase. FFO (funds from operations), NOI (net operating income), and EBITDA, have all risen nicely over this window of time.

Author – SEC EDGAR Data

This is not to say that everything is fantastic. There are some weaknesses in the current fiscal year. In the first half of 2023, RPT Realty reported revenue of $103.3 million. That represents A decline compared to the $111.4 million the company reported one year earlier. This drop was largely attributable to a $12.5 million hit associated with the company’s decision to sell off certain properties to RGMZ and another subsidiary called R2G. Actual property economics still remain positive, with the occupancy rate of its assets growing from 91.5% in the first half of 2022 to 91.6% the same time this year. But with the decline in revenue came a decrease in most of the company’s profitability metrics. As you can see in the chart above, operating cash flow did increase. However, all of the other profitability metrics declined modestly year over year.

Author – SEC EDGAR Data

One thing that makes evaluating this transaction very simple is the fact that both companies have been very clear about what they expect financial performance to look like for the 2023 fiscal year. For instance, if we take the midpoint of guidance for RPT Realty for its FFO per share, we should anticipate FFO this year of $84.8 million. Based on my own calculations, this should translate to the results shown in the table above. That table also shows the expected figures for Kimco Realty using the same approach.

Kimco Realty

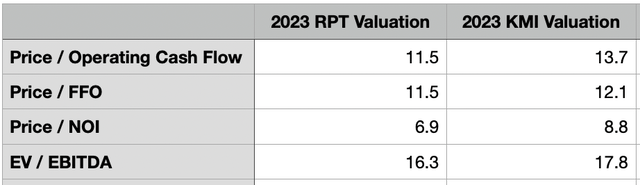

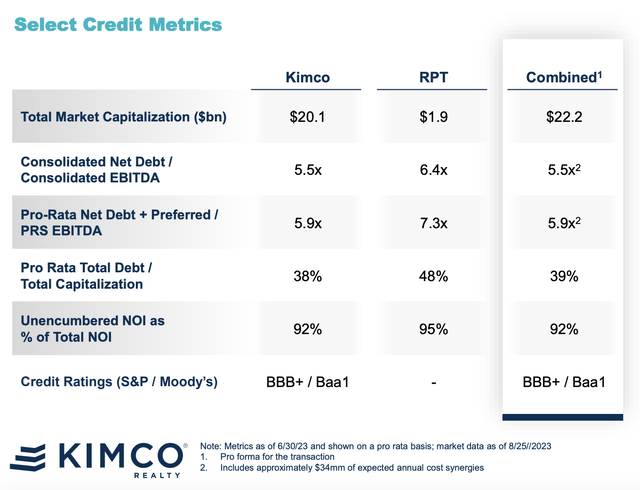

Taking the aforementioned calculations, I then decided to price the companies. On a forward basis, the implied buyout price for RPT Realty translates to a price to operating cash flow multiple of 11.5. That’s lower than the 13.7 rating that we get for Kimco Realty. The price to FFO multiple is 11.5 compared to 12.1 for the acquirer. Moving on to the price to NOI approach, we have a multiple of 6.9 versus 8.8, respectively. And when it comes to the EV to EBITDA approach, we get 16.3 compared to 17.8. And what makes this really great is that it assumes that none of the synergies predicted by Kimco Realty come to pass. Now, it is true that RPT Realty has a higher net leverage ratio of 6.4 compared to the 5.5 that Kimco Realty has. But the combined company should still have a net leverage ratio of only 5.5. This is because the size disparity between the two firms will result in shareholders of RPT Realty receiving only 8% of the new business, while investors in Kimco Realty will get 92%.

Kimco Realty

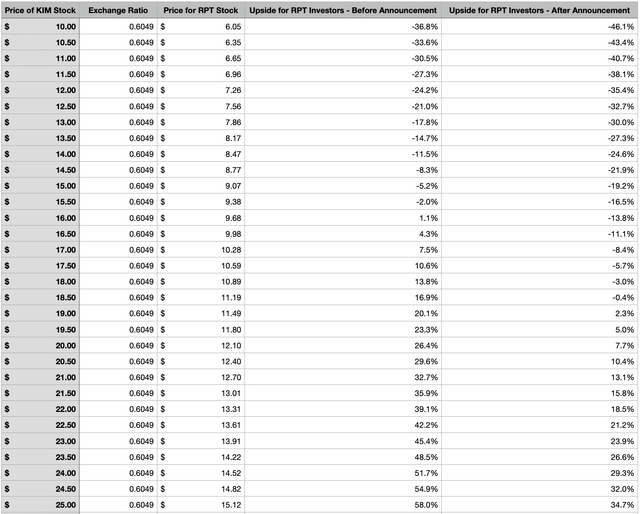

There is one risk that investors should be aware of. And this relates to the fact that the all-stock nature of the deal means that the two companies should move in tandem with one another. Keeping all else the same, in the event that Kimco Realty sees its share price drop by 50%, you would see a 50% drop associated with Kimco Realty. On the other hand, you would see a similar increase a company a 50% rise in Kimco Realty shares. This is not something that you get with an all-cash deal and it is something you only get partially with a cash and stock deal. To get some perspective of how this might look under different pricing scenarios for Kimco Realty, I created the table below. You can see how, for each $0.50 per share that Kimco Realty moves, shares of RPT Realty should move.

Author – SEC EDGAR Data

Takeaway

All things considered, I would make the case that this deal probably makes sense for both parties. If there is a winner, it is certainly Kimco Realty since it is using it’s slightly more expensive stock to pick up a healthy business. Of course, this ignores the synergies that could sweeten the end result even further. But I don’t like to assume that will come to pass. There isn’t really anything I dislike about the transaction. I would argue that upside from here is limited for RPT Realty since the current spread between where shares are today and the implied buyout price is only 1.1%. But if you are bullish about Kimco Realty itself, buying into Kimco Realty then picking up RPT Realty could be a slightly cheaper way to get in on the action.

When it comes to the preferred shareholders of RPT Realty, the management team at Kimco Realty, in a call on the matter, mentioned that the units will be essentially swapped out for units in the new, combined company. They will have interests that are similar in nature to what the existing RPT Realty preferred units have. So there is no reason for investors who liked the preferred units previously to change their mind on them now.

Read the full article here