Investment thesis

Photronics (NASDAQ:PLAB) is an IC and Flat Panel Displays (FPD) photomask producer that is benefiting from the increasing demand for consumer electronics, innovative medical devices, and displays for mobile devices and ultra-large screen televisions. Photomasks are components that have been used to manufacture nearly every semiconductor that has ever been made and have made semiconductor manufacturers able to produce in a high-volume efficient way. Due to the strong demand trends in the semiconductor market, Photronics’ financial results in its second quarter of fiscal year 2023 were strong, and with higher demand for IC and FPD photomasks in Taiwan, China, South Korea, the United States, and Europe, I expect PLAB’s revenue and net income to improve further in the following years.

The global semiconductor photomask market is estimated to grow at a CAGR of 15% from 2023 to 2029, and Photronics is known to be one of the top major prominent players in the industry. PLAB expects its FY24 revenue to be between $900 to $975 million, its free cash flow to be between $250 to $300 million, and its diluted EPS to be between $2.35 to $2.65, significantly higher than the company’s revenue, gross margin, and diluted EPS in the twelve months ending 30 April 2023. In the long-term, Photronics is a buy, and if you take a look at the company’s rating summary (SA Analysts, Wall Street, and Quant), you will realize the reason. The stock’s price decreased by 12% in the past month, which can be seen as a correction to PLAB’s rally from 1 May 2023 to 30 July 2023 (the stock’s price increased by 84% during this period). Also, the foreign exchange movements in the third quarter of fiscal year 2023 are not as favorable as in 2Q FY23. Thus, the recent drop in the stock price can also be attributed to investors’ expectations for lower foreign exchange gain in 3Q FY23. Anyway, the question is whether the current stock price is a good entry point or not. My answer is yes.

The company achieved record revenue in the second quarter of fiscal year 2023 as the company’s IC photomasks sales and FPD photomasks sales increased by 14.6% and 6.0%, respectively, driven by higher sales in Taiwan, China, and the United States. Photronics gross profit increased from $70 million in 2Q FY22 to $76 million in 1Q FY23, and increased further to $84 million in 2Q FY203, implying that in the past few quarters, PLAB has been able to sell more of its IC and FPD photomasks while managing its cost of goods sold efficiently.

In the past 10 years, PLAB’s revenue increased at a CAGR of 7% and its cost of revenue increased at a CAGR of 5%. Also, in the past five years, the company’s revenue increased at a CAGR of 12%, and its cost of revenue increased at a CAGR of 6%. It simply means that Photronics has been continuously increasing its ability to turn every dollar it pays as the cost of revenue into cash. In the past few quarters, PLAB managed to keep its operating expenses at a stable level and decided to offset higher selling, general, and administrative expenses with lower R&D expenses. As a result, driven by higher revenue that wasn’t offset by higher operating expenses, the company’s operating income increased from $49 million in 2Q FY22 to $56 million in 1Q FY23 and increased further to $67 million in 2Q FY23.

Due to favorable foreign currency transaction impacts (as a result of favorable movements of the South Korean won and the New Taiwan dollar against the U.S. dollar which exceeded the unfavorable movement of the RMB against the U.S. dollar from 29 January 2023 to 30 April 2023), PLAB managed to turn its non-operating loss of $14 million in the first quarter of fiscal year 2023 into a non-operating income of $14 million in the second quarter of fiscal year 2023. It is worth noting that PLAB’s non-operating loss of $14 million in 1Q FY23 was due to the unfavorable movements of the South Korean won and the New Taiwan dollar against the U.S. dollar exceeding a favorable movement of the RMB against the U.S. dollar from 31 October 2022 to 29 January 2023.

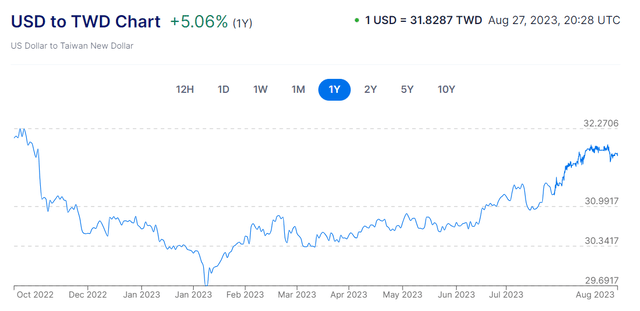

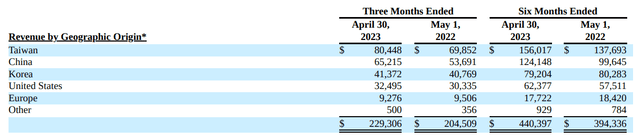

According to Figure 1, in 1Q FY23, the New Taiwan dollar appreciated against the USD, which was unfavorable for PLAB in Taiwan (it is important to know that according to the company’s revenue by geographic origin, Taiwan accounts for 35% of PLAB’s total revenue, followed by China, Korea, United States, and Europe (see Figure 2). Thus, the USD rate against the New Taiwan dollar plays the most important role in determining PLAB’s non-operating results. Also, according to Figure 3, in 1Q FY23, the South Korean won appreciated against the USD, which hurt PLAB’s non-operating results. According to Figure 4, in the same period, RMB appreciated against the USD, and in contrast with the appreciation of the South Korean won and the New Taiwan dollar against the USD, the appreciation of RMB against the dollar is favorable for Photronics.

In the second quarter of fiscal year 2023, the New Taiwan dollar, South Korean won, and Chinese RMB depreciated against the USD, and the depreciation trend of the New Taiwan Dollar and RMB against the USD is continuing. However, the depreciation trend of the South Korean won against the USD stopped in 3Q FY23. It simply means that in the third quarter of the fiscal year 2023, Photronics benefited from favorable movements of the New Taiwan dollar against USD; however, suffered from the unfavorable movements of the South Korean won and RMB against USD. As a result, I don’t expect PLAB’s foreign currency transactions net impact in 3Q FY23 to be as favorable as in the previous quarter; however, I still expect the company to report a positive non-operating income in its 3Q FY23 results.

As we can see in Figure 1 and Figure 3, New Taiwan dollar, and South Korean won experienced a significant depreciation against USD in the past few weeks, implying that the foreign exchange transactions net impact on Photronics non-operating results in 4Q FY23 can even be better than in 2Q FY23. I estimate PLAB’s non-operating income in 3Q FY23 to be between $5 to $10 million, and I expect its non-operating income in 4Q FY23 to be between $15 to $20 million. It is worth noting that in 2Q FY23, PLAB’s non-operating income of $14 million accounted for 17% of its income before income tax provision. Also, in 1Q FY23, the non-operating loss of $14 million, decreased the company’s income (before income tax provision) by 20%. Thus, PLAB’s non-operating income or loss is not negligible and plays an important role in determining the profitability of the company. In 2Q FY23, PLAB reported a diluted EPS of $0.65, compared with a diluted EPS of $0.23 in the previous quarter. Excluding foreign exchange effects, I calculate 1Q FY23 and 2Q FY23 diluted EPS of $0.32 and $0.54, respectively. Thus, the foreign exchange movements in the following months can significantly improve PLAB’s financial results.

Figure 1 – USD to TWD

www.xe.com

Figure 2 – PLAB revenue by geographic origin

PLAB’s 2Q FY23 results

Figure 3 – USD to KRW

www.xe.com

Figure 4 – USD to CNY

www.xe.com

Why I might be wrong?

RMB’s depreciation against the USD in the past few months (which is unfavorable for PLAB) was due to China’s weaker-than-expectations economic results. Evergrande, one of the biggest real estate companies in China reported a huge loss in the first half of 2023, implying that the real estate sector of China is facing serious challenges. On the other hand, as a result of the Federal Reserve’s tight monetary policies, inflation in the United States seems to be tamed, and the economic outlook of the United States is now better than a year ago. Also, as the Federal Reserve starts cutting high interest rates which I expect to happen in the next 6 to 9 months, the U.S. economic condition may improve, resulting in the appreciation of the dollar against RMB. The People’s Bank of China (PBoC) is trying to support Yuan, but PBoC might turn out to be unable to stop Yuan from falling further. U.S. appreciation against the New Taiwan dollar and South Korean won is favorable for Photronics, and China’s economic challenges can have large negative effects on the economy of South Korea and Taiwan (causing the Taiwan New dollar and South Korean won to depreciate more against USD). However, PLAB’s foreign exchange loss from the unfavorable movements of the RMB against the USD can be more than the company’s foreign exchange gains from the favorable movements of the New Taiwan dollar and South Korean won against the USD. Thus, despite what I expect, PLAB may experience a foreign exchange loss again in 4Q FY23 or 1Q FY24.

Conclusion

Photronics is well-positioned to benefit from the increasing demand for IC and FPD photomasks around the world. In the long-term, the stock is a buy. Also, the recent drop might have made a good entry point for short-term and mid-term investors, as I see the net impact of the foreign exchange movement to be favorable for PLAB. The company’s non-operating income can increase to more than $15 million in the fourth quarter of FY23. However, the company’s non-operating income in 3Q FY23 was lower than the previous quarter, which can partly explain the stock’s recent drop.

Read the full article here