Introduction

CVR Energy (NYSE:CVI) is a company that has diversified its operations in the petroleum refining and marketing industry and the nitrogen fertilizer manufacturing industry; CVR Energy also produces and markets renewable diesel. In the petroleum refining segment, they refine and market transportation fuels. It is worth mentioning that CVR Energy owns 37% of the units of CVR Partners (UAN), while Icahn Enterprises L.P. and its affiliates (IEP) owned 71% of CVR Energy at the end of 2022.

CVI’s business outlook

Following the start of the energy transition process, CVR Energy focused more on its renewable initiatives, including converting the refinery’s hydrocracker to a renewable diesel unit; moreover, they separated their renewables business by the early months of 2023 and thus would be able to complete their renewable feedstock pretreater project by the end of the third quarter of 2023.

CVR Energy’s solid financials during the second quarter of 2023 provided a pleasant opportunity to issue a special dividend amount of $1 per share in addition to their regular quarterly dividend of $0.50 per share; as a result, the management distributed the profit of their strong earnings results directly to the shareholders. However, it is worth noting that one of the drawbacks of special dividends is that they reduce the share price of the company by the dividend amount in the short term thus, that could be a reason for CVI’s slight decrease in their share price after August 21st, 2023 when they paid their payment. Additionally, CVI holds a dividend yield of 5.7% in TTM, which is very attractive for companies in this industry.

During the second quarter, fertilizer prices kept decreasing as compared to the same time in 2022, and it may decline more by the end of 2024. It is expected that global nitrogen supply will grow by 1.6% by 2024, while global demand will reach a 1.0% annual growth rate; therefore, unfavorable nitrogen prices are expected in the short term. However, thankfully the company had sold more than 40% of its second quarter volume in the first quarter of 2023, thus at higher prices. Overall, lower nitrogen prices were partially offset by higher production levels in 2Q 2022 and thus resulted in $87 million of Adjusted EBITDA. Additionally, there are no worries about their summer and fall fertilizer inventories because they have finalized the ammonia orders for the summer and fall in advance.

CVI’s financial outlook

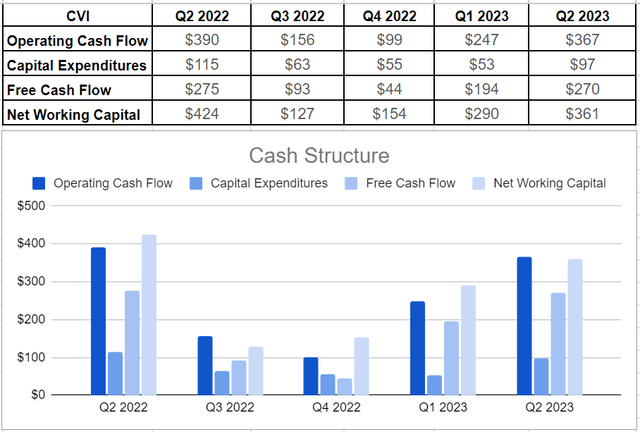

Analyzing CVR Energy’s cash structure illustrates the company’s strong and healthy position to make its payments, and hence absorb its upcoming financial risks. In minutiae, CVI owns approximately 37% of CVR Partner’s common outstanding share. With a $4.14 cash distribution from the partnership, based on their approximately 10,600,000 number of shares, CVI Energy received circa $16.2 million of cash payment from the partnership. In addition, in the second quarter of 2023, the company surged its operating cash flow by over 48% and reached $367 million versus $247 million at the end of the first quarter of 2023. Thankfully, their capital spending of $97 million was not too much and thus led to approximately $270 million of free cash flow. Their capital expenditures were lower than their CapEx at the same time in 2022, which was partially due to lower expenses in the Petroleum segment. In other words, lower natural gas and crude oil prices affected their petroleum direct operating expenses from $6.12 per barrel to $5.46 per barrel.

Following the company’s strong balance sheet condition, its net working capital (NWC) demonstrates its liquidity capabilities during the recent quarter. After a deep drop in their NWC from $424 million in 2Q 2022 to $127 million in 3Q 2022 due to lower commodity and refinery prices in the second half of 2022, CVI could increase its NWC in every quarter and ultimately reach $361 million in 2Q 2023. This metric measures CVI’s liquidity and capability to meet its short-term obligations (see Figure 1).

Figure 1 – CVI’s cash structure (in millions)

Author

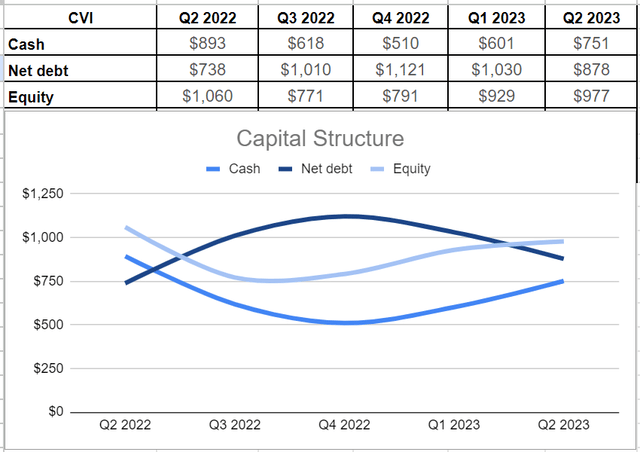

Going through their balance sheet and capital structure indicates that the company was successful in improving its cash balance by circa 25% in 2Q 2023 and generated $751 million of cash versus $601 million at the end of the first quarter. $69 million of cash balance was directly from the Fertilizer segment. Moreover, they declined their net debt level by approximately 15% during the recent quarter to $878 million. It is worth noting that their nearest senior note maturity is due in 2025, and thanks to their minimal capital expenditures, the company will be able to hold cash on their balance sheet to offset their due obligations. Additionally, another positive point about their balance sheet strength is related to their $977 million equity level, which is above their debt levels, thereby decreasing the risk of financing in the future (see Figure 2).

Figure 2 – CVI’s cash structure (in millions)

Author

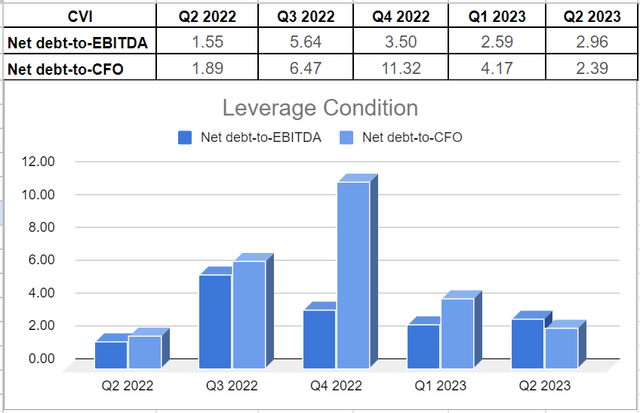

Once looking ahead to the rest of 2023, I believe their net debt will continue to fall, thanks to the management’s guidance for minimal capital expenditures and thus higher free cash flow prospects, albeit it is not possible to be sure due to the volatile nature of this industry. In addition, after analyzing their strong balance sheet structure, it goes with no surprise to see improvements in their leverage condition. In other words, CVI’s leverage condition across the board of net debt-to-EBITDA and net debt-to-CFO illustrate that these metrics have been far lower than almost all previous quarters. In minutiae, CVI’s net debt-to-EBITDA metric sat at 2.9x in 2Q 2023. Also, their net debt-to-CFO sat at 2.3x, which despite being higher year over year compared with 1.89x in 2Q 2022, is far lower than 4.17x in the first quarter of 2023. Overall, it is worth mentioning that the severe fluctuations in their leverage condition are normal to a great extent due to the inherent volatility in their industry and operations (see Figure 3).

Figure 3 – CVI’s leverage ratios

Author

Risks related to CVI’s operations

First and foremost crucial risk associated with CVR Energy’s operations is related to the global oil markets. Recent decisions from OPEC+ countries about cutting crude oil production to reach higher prices may have a negative impact on the company’s operating income and increase their capital spending in the Petroleum segment because they do not produce crude oil and are required to purchase crude oil that they refine. Moreover, the company’s cost to acquire feedstocks and the final price of their refined products highly relies on the supply and demand of crude oil, gasoline, and diesel. Furthermore, although global economic conditions are improving and combatting the supply constraints of last year, continuous global economic uncertainties may adversely affect their liquidity and ability to meet their outstanding obligations. Also, it is worth mentioning that approximately 25% of the net sales of the Petroleum segment and 30% of the net sales in the Nitrogen Fertilizer segment were directly from the two largest customers in 2022. As a result, if the company loses any of these customers for any reason, like their decision to purchase products with lower emissions, it can adversely affect CVI’s financial condition and cash flow.

Conclusion

Notwithstanding the severe natural volatility of their industry, CVR Energy’s financial conditions are healthy and strong enough to absorb future risks to a great extent. The company decreased its net debt levels and expects to decrease more debt by the end of the current year. Thanks to their guidance for minimal capital expenditures and thus higher upcoming free cash flow. Additionally, the increase in their net working capital is a positive sign of their health liquidity condition. When all was said and done, CVR Energy’s strong financials and business outlook make the company a profitable investment option.

As always, I appreciate your time and your comments.

Read the full article here