Originally posted on August 26, 2023

In this weekly outlook, I examine the asset classes, sectors, equity groups, ETFs, and individual stocks that are leading the market higher, and which market segments are lagging behind.

By keeping an eye on the leaders and laggards, we can get a sense of where the big money is going, and where it’s coming from. Signs that market participation is broadening out are continuing to show up in the data. As this trend continues, it is improving the durability of the rally.

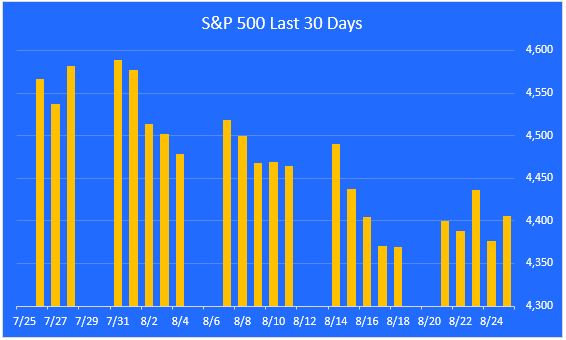

The S&P 500 pullback continues.

After making a new 2023 high on July 31, the market is now in the process of consolidating its gains and expanding its participation. For the week, the S&P 500 was up 0.8%.

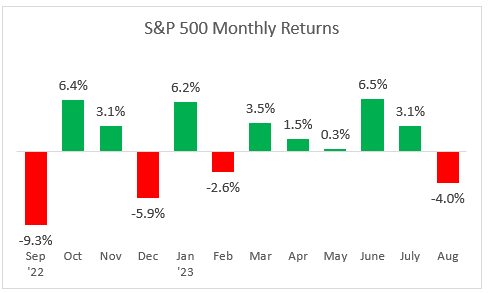

A look at monthly returns.

This chart shows the monthly returns for the past year. The August pullback has erased all of the July gains. It looks like we’re getting the 5%-7% decline I have been expecting.

ZenInvestor

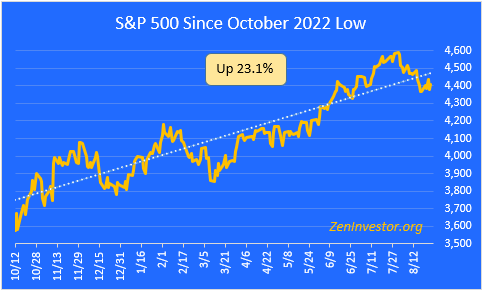

The bull market dips below the trend line.

This chart highlights the 23.1% gain in the S&P 500 from the October 2022 low through Friday’s close. The index is now 8.1% below its record-high close on January 3, 2022.

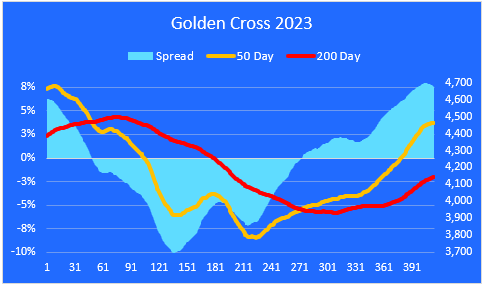

The Golden Cross.

The market entered a Golden Cross configuration (a Golden Cross occurs when the 50-day moving average crosses above the 200-day) on February 2, 2023.

The spread between these two moving averages is widening. Today it stands at 7.7%, more than three times as wide as the long-term average of 2.3%. This widespread is one of the reasons I’m expecting a pullback of 5-7% for the S&P 500.

ZenInvestor

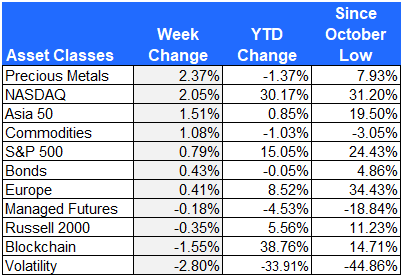

Major asset class performance.

Here is a look at the performance of the major asset classes, sorted by last week’s returns. I also included the year-to-date returns as well as the returns since the October 12, 2022, low for additional context.

The best performer last week was Precious Metals, as investors looked for ways to protect their gains from further downside in the market.

The worst-performing asset class last week was Volatility. Blockchain companies lost more ground, due to continued weakness in the Crypto space.

ZenInvestor

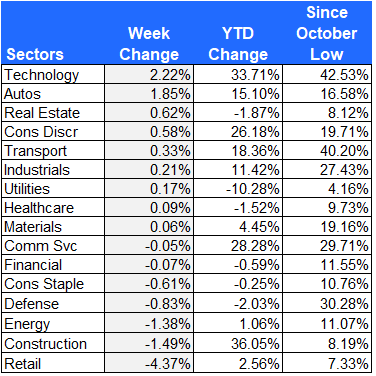

Equity sector performance

For this report, I use the expanded sectors as published by Zacks. They use 16 sectors rather than the standard 11. This gives us added granularity as we survey the winners and losers.

Technology stocks led the way higher last week after NVIDIA (NVDA) blew the doors off of analyst earnings estimates. The company also raised guidance for the next few quarters.

Retail was the hardest hit, losing -4.37% for the week. The financial media blamed the poor showing on weaker-than-expected back-to-school spending.

ZenInvestor

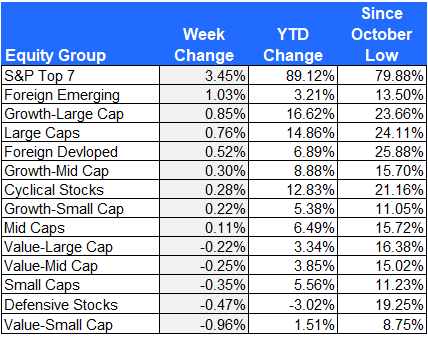

Equity group performance

For the groups, I separate the stocks in the S&P 1500 Composite Index by shared characteristics like growth, value, size, cyclical, defensive, and domestic vs. foreign.

The S&P Top 7 stocks by market cap led the way higher, inspired by big moves by NVDA and TSLA.

The worst-performing group was small-cap value, which lost -0.96%.

ZenInvestor

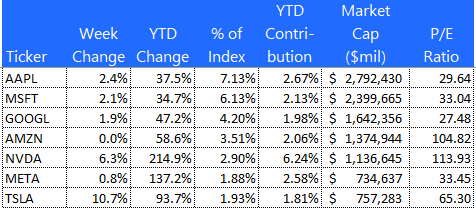

The S&P Top 7

Here is a look at the seven mega-cap stocks that have been leading the market all year. Nvidia was up 6.3% for the week. Tesla was the biggest winner, up 10.7%.

ZenInvestor

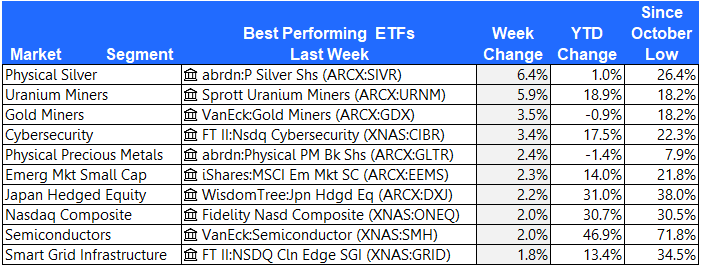

The 10 best-performing ETFs from last week

Silver, Gold, and Uranium ETFs were big winners last week. Cybersecurity also did well.

ZenInvestor

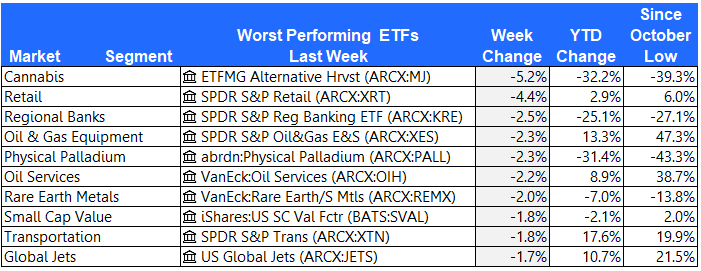

The 10 worst-performing ETFs from last week

Cannabis had another tough week, down -5.2%. The ETFMG Alternative Harvest ETF is down -32.2% year-to-date. Retail stocks also had a tough week.

ZenInvestor

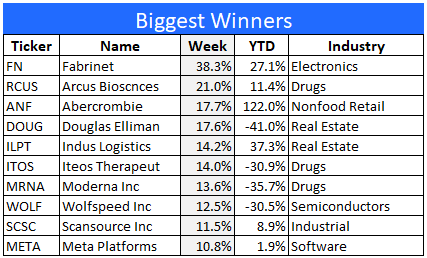

The 10 best-performing stocks from last week

Here are the 10 best-performing stocks in the S&P 1500 last week.

Fabrinet (FN), an electronics company, was up 38.3% last week. The company posted sales and earnings that came in better than Wall Street had anticipated.

ZenInvestor

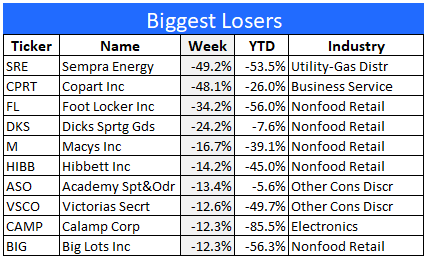

The 10 worst-performing stocks from last week

Here are the 10 worst-performing stocks in the S&P 1500 last week.

Both Sempra Energy and Copart split 2-for-1 last week, making it look like the stocks were cut in half. The shares of both companies actually made small gains for the week.

Foot Locker (FL), Peloton (PTON), and Dick’s Sporting Goods (DKS) all crumbled after they announced earnings, dragging footwear and fitness stocks lower.

ZenInvestor

Final thoughts

The S&P 500 was up 0.8% last week, but the near-term trend is still lower. The gain can be attributed to the strong showing by the top 7 market leaders, which were up by 3.45% on average. This masks a weaker market. On an equal-weighted basis, the market was down by -0.2% for the week.

This tells me that the current pullback is not over yet. We have given back 4% of the market’s gains since the recent peak on July 31st. I’m sticking with my 5-7% decline for now.

Are you looking for more high-quality ideas? Consider joining The ZenInvestor Top 7, my Marketplace service. The Top 7 is a factor-based trading strategy. Its screening algorithm prioritizes reasonable price first, then the momentum, and finally projected earnings growth. The strategy produces 5-7 names and rebalances every 4 weeks (13 times per year). The goal is to catch healthy companies that have gone through a rough period, and are now showing signs of making a strong comeback. Join now with a two-week free trial.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here