One of the two major economic/market events that occurred last week (week of August 20) was the stellar performance of Nvidia (NVDA) which, unlike the retailers, beat on both top and bottom lines and whose stock price has soared from a 112 low last October to a high print of nearly 503 early on Friday morning (August 25). That’s nearly a 450% rise in less than a year. As a result, on Friday, shareholders began taking profits as the stock closed within pennies of its low for the day at just over 460, down -8.5% from its early morning high.

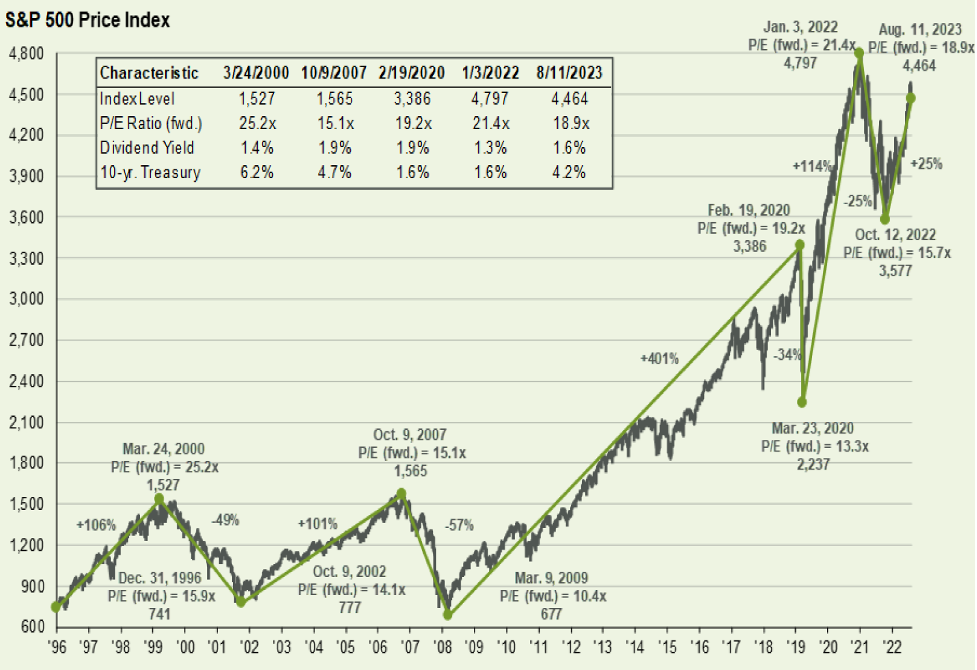

Nvidia’s one day performance feels very much like a compact version of the S&P 500’s performance over the past month. After a monster rise of 28% from last October 12th’s low point (3577) to its July 24th high (4582), over the next month (to August 24) the S&P 500 fell -4.6%, closing at 4369 on Thursday before a small rally on Friday. We attribute this small rally to Fed Chair Powell’s recognition, in his keynote speech at the Fed’s annual Jackson Hole symposium, that progress has been made on the inflation front and that there is uncertainty over the timing of policy lags on the economy. Hints, perhaps, that the tightening cycle may be nearing its end.

Despite the August pullback in equity prices, markets continue to be convinced that the economy will have a “soft-landing.” This is the same attitude market participants had prior to the tech-wreck Recession at the turn of the century and to the Great Recession. Given that those participants listen to the business media which, in turn, listen closely to the economists employed at the major Wall Street firms, a “soft-landing” scenario is always going to be the “official” forecast prior to any Recession, lest those economists suddenly become unemployed! As readers of this blog know, we are not in that “soft-landing” camp. Incoming data say so!

The Retailers

In past blogs, we noted the rapid rise in credit card balances as consumers tried to maintain their living standards in the face of rapidly rising prices. For the first time in Q2, credit card balances exceeded $1 trillion, up $270 billion over the past year, well in excess of the $120 billion that Rosenberg Research says is the long-term average growth rate. Unpaid balances, according to Rosenberg, are up 16% (with credit card interest rates above 20%), and delinquencies, at 2.8%, are up large from 1.8% a year ago. Eventually, credit card lines of credit get maxed out leading to spending cut-backs. And such behavior appears to already have started as gleaned from Q2 financial reports from the nation’s major retailers.

- Dick’s Sporting Goods (DKS) missed on earning (-25% from year earlier levels). They also cut forward guidance and announced layoffs.

- Footlocker (FL) missed on top line revenues, suspended their dividend, and cut their outlook. Sales are now forecast to fall -6.5% to -8.0% for the fiscal year.

- Macy’s (M) sales fell -8.4% for the year ended in Q2 while earnings fell a huge -74%! They also noted a rise in credit card delinquencies and a large decline (-41%) in credit card revenues over the prior 12 months.

- Target

TGT

- Home Depot (HD) reported a fall in top and bottom lines in Q2 from 2022 levels. Revenues were off -2.0% and EPS -7.9%.

- Dollar Tree

DLTR

- The Gap

GPS

All the above retailers and others cited rampant theft and shoplifting as a major issue, both for Q2 and going forward (a symptom of the DeSantis “country in decline” theme at the August 23rd Republican debate). It appears that the impact from the 2021 stimulus checks has begun to wear off. Walmart

WMT

“Soft-Landing?” – we don’t think so! Remember, consumption is 70% of GDP.

Commerce

Last week we noted the large fall in the Cass Freight Index and remarked that, if goods aren’t moving, the economy isn’t doing well. Some of the Regional Federal Reserve Banks do monthly surveys in their regions. The Richmond Fed Manufacturing Index came in at -7 for August, now negative for 15 months in a row. Employment was negative too (-3 in August vs. +5 in July).

New Orders were down (-11 for August), and Backlogs (-26) and Vendor Delivery Delays (-17) all show weakening demand. On the inflation front, Prices Received were up +3.1% from a year earlier in August vs. +4.6% in June and +8.9% a year earlier (August 2022), a continued and welcome cooling. The Kansas City Fed’s Mfg. Index showed a big fat 0 in August vs. -11 in July. New Orders at -3 have been negative 12 months in a row, and Exports at -8 are down four months running. The workweek fell to -6.

The Philly Fed’s Non-Manufacturing Index for August was -13.1, now negative in five of the last six months. The New Orders Index fell to -16.0 from -13.3 in July. It too has been negative in five of the last six months. August revenues from the surveyed participants scored -5.7 vs. +4.0 for July. Views of economic conditions in six months, while still positive at +8.2 in August, were down significantly from July’s +20.5. Perhaps we are seeing less buy-in to the “soft-landing” mantra.

S&P’s Global Manufacturing PMI fell to 47.0 in August from 49.0 in July. (50 is the demarcation between expansion and contraction). According to S&P, both the U.K. and Europe appear to have entered Recessions.

Heavy Industry

The health of heavy industry is normally an indication of overall world-wide economic conditions. Global steel production is flat to last year (-0.1% year to date). China’s production was down (-0.6%) in June vs. a year earlier, and the outlook for the second half of 2023 is for further deterioration (-0.9%). Given the weakness in China’s economy, that outlook appears generous.

The aluminum market appears to be in even worse shape. Worldwide, production has slowed for seven months in a row. Production in China fell -1.4% (July) from year earlier levels, and it’s down -8.7% in central Europe.

U.S. Housing

Mortgage rates are now at their highest level since 2002. It is the major culprit in the lowest level of affordability since the 1970s.

Mortgage purchase applications fell -5% the week ending August 18 and are down 30% from a year earlier. This isn’t a wonder! Because the Fed held the Fed Funds Rate near 0% from the end of the Great Recession until 2022, most homeowners have mortgages in the 3% range.

Selling a $500,000 home with a $400,000 30-year mortgage at 3%, and moving to another home with a $400,000 mortgage but at a 7% interest rate, increases the monthly mortgage principal and interest payment from $1,686/month to $2,661/month, a 58% increase (nearly $1000/month). In today’s world, unless one has to move (job change etc.), most rational people will wait for lower rates. Thus, the -17% fall in Existing Home Sales over the year ending in July. The only good news here is that, for the first time in a very long time, even despite the tight supply of inventory, the median home price fell in July (-0.8%), not much, but better than a rise and perhaps the beginning of a trend!

Lending

The left side of the chart below shows that, in the Dallas Fed’s latest survey, huge declines have occurred in current and expected future loan demand. The right-hand side shows current and expected Non-Performing loans. Clearly, bankers aren’t seeing sunny skies ahead!

Non-Farm Payrolls

Two weeks ago, this blog discussed our skepticism about the strength of the July Non-Farm Payroll data. For us, the conclusion from the data that the labor market remained robust just didn’t add up to what we were seeing in the rest of the economy. To reiterate, the Household Survey showed up as +268K net new jobs. That was composed of a loss of -585K in full-time jogs offset by +853K part-time jobs. Oddly, the Bureau of Labor Statistics (BLS) counts full-time and part-time jobs as equal, so the net number was calculated as +853 – 585 = +268. Common sense says that part-time jobs are not equal to full-time jobs, else why would someone have to hold two or more part-time jobs to make ends meet, but only one full-time? Scoring part-time as half leads to a very different conclusion about the strength of the labor market, i.e.: (853/2)-585 = -158.5 which we think is a better indicator of the state of the jobs market.

So, it isn’t surprising to us that BLS revised payrolls down for the 12 months ending in March by -306K. That’s -25K/month. While job growth over the year was still substantial, the overstated figures may have been a key reason behind the Fed’s rate hikes and their steady stream of hawkishness. We suspect that, at the next revision release, the April 2023 and forward months will also show downward revisions.

Final Thoughts

Markets are very sensitive to Fed thinking and market rates can move rapidly one way or the other depending on what markets interpret from any public statements by FOMC members, especially from the Fed Chair. Powell has to stay hawkish, lest the bond market prematurely (in the Fed’s view) move interest rates lower. So, he must be quite careful in what he says. In his Jackson Hole speech, he did acknowledged progress on inflation and that monetary policy acts with long and variable lags. But he remained hawkish saying that interest rates will remain “higher for longer” and that the Fed will continue tight monetary policy “until the job is done.”

- Retailers did not have a banner Q2 and expect further deterioration going forward.

- In October, student loan payments restart. That, along with the apparent exhaustion of “excess savings” (from the free money giveaways of 2021) is going to put even more downward pressure on retail sales.

- The Fed’s own Regional Bank Manufacturing and Non-Manufacturing Indexes are all showing weakness. Worldwide, China looks like it is already in Recession as does much of Europe.

- The banks have tightened lending standards which means less credit going forward. Credit is the lifeblood of the U.S. economy, so less credit implies economic deceleration. Auto and credit card delinquencies are rising rapidly and the Dallas Fed sees soaring non-performing loans in the near future.

To summarize: Poor reports from the large retailers; falling home sales; the lagged impact of monetary policy tightening, including a fall in the money supply over the past year (another 100% Recession indicator); rapidly falling inflation (a symptom of falling pricing power); ongoing weakness in manufacturing; the restart of student loan payments; and a deteriorating banking outlook are the hard realities. We remain in the Recession camp.

(Joshua Barone and Eugene Hoover contributed to this blog)

Read the full article here