In this article, we take a look at the TriplePoint Venture Growth (NYSE:TPVG) BDC. The company is one we have avoided in our Income Portfolios since the start of our BDC coverage due to its inconsistent and, generally, underwhelming performance. However, the company continues to trade at a premium valuation – a puzzle which we explore below.

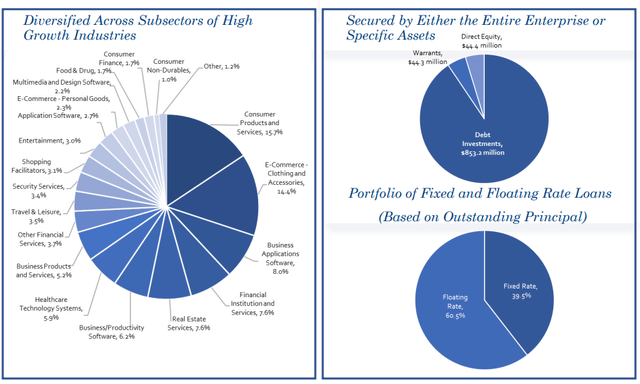

TPVG is focused on debt and direct equity investments to venture growth stage companies in Tech and other growth sectors. Its top allocation sectors are software, e-commerce, and consumer services.

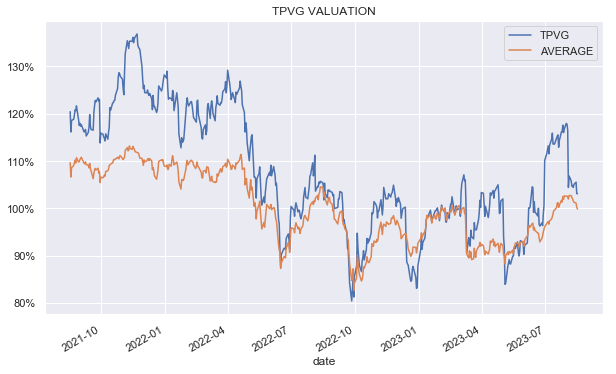

TPVG

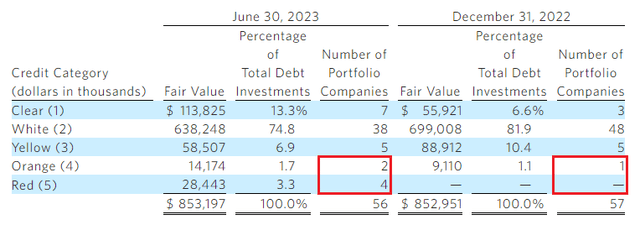

TPVG recently reported its Q2 results. The key takeaway for us is that the portfolio is deteriorating at a quickening pace. We can look at a couple of different metrics here. One is the company’s own internal ratings. Here we see that it went from one holding in the worst two buckets (orange and red) at the end of 2022 to six holdings in the worst two buckets.

TPVG

Interestingly, the orange bucket increased by one holding while the red bucket increased by a total of four. Two of these companies went bankrupt during the quarter, which obviously limits the potential for restructuring and further upside.

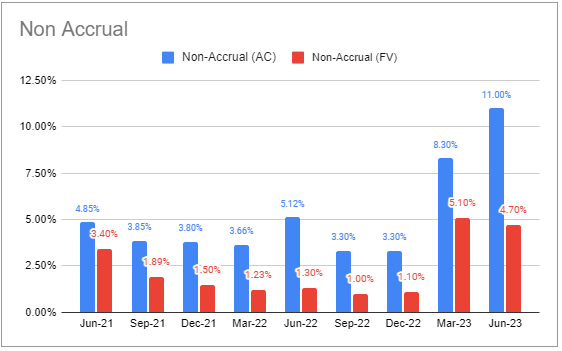

We can also see this worsening portfolio quality trend in the non-accrual numbers, which have not only deteriorated but moved to a double-digit level that is rarely seen in the BDC space. By contrast, the median non-accrual at cost figure for BDCs in our coverage is 1.8% with the non-accruals by fair value of 1.1%.

Systematic Income BDC Tool

TPVG is not the worst BDC on this metric, however, other BDCs in the same neighborhood either trade at much lower valuations (such as BKCC at 79%) or have much stronger total NAV returns (such as GAIN).

This portfolio trend also highlights a lack of diversification in the TPVG portfolio, which has less than half of debt positions than the average BDC. This means that one or two problem holdings can have an outsized impact on the NAV.

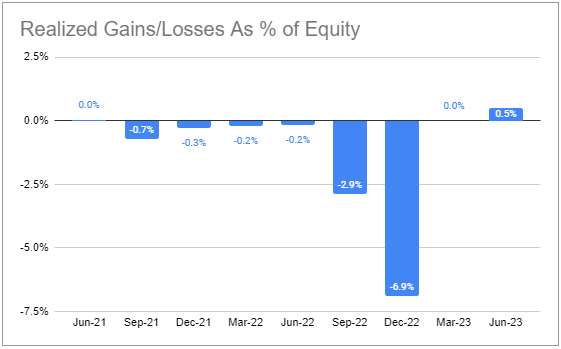

Non-accrual policies can be very different across BDCs, and some will move a holding to non-accrual quicker than others. However, realized gains are where the rubber meets the road, so to speak, and here the figures are bad as well. The last couple of quarters have been fairly benign, however, the last two quarters of 2022 shaved off close to 10% of the portfolio.

Systematic Income BDC Tool

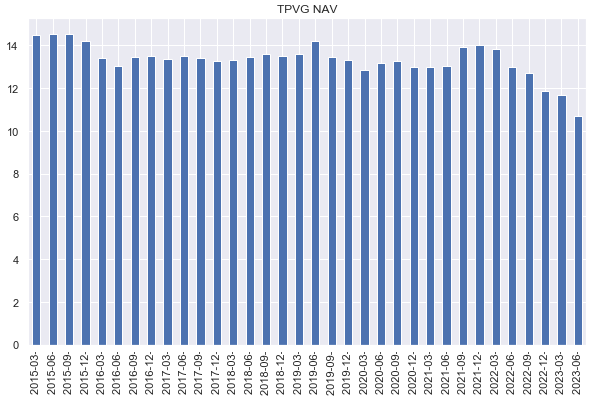

All of this has translated into a sharp drop in the NAV in an environment that has not been all that brutal for BDCs. The rest of the sector has been able to mostly manage just fine with relatively stable or even rising NAVs. On the call, management said the current difficulties are not dissimilar to other credit cycles, however, the chart below suggests something is very different this time.

Systematic Income

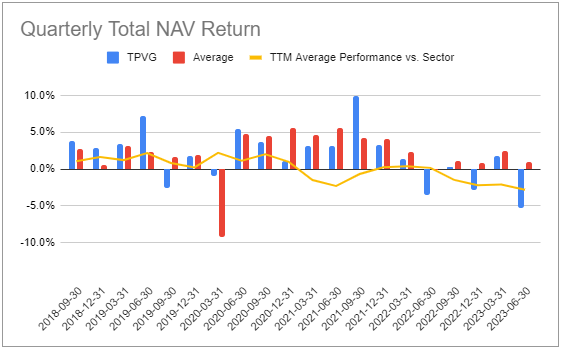

This has also meant that the company has put in a stark sequence of underperformance of 11 quarters out of the last 12. In addition, the pace of underperformance is worsening. We can see this by the yellow line moving lower below zero in the chart below.

Systematic Income BDC Tool

We tend to allocate to BDCs that outperform or those that have underperformed historically but whose underperformance gap is shrinking (i.e., where the yellow line is moving up). TPVG is firmly in the least appealing quadrant of underperformers and companies whose underperformance is worsening.

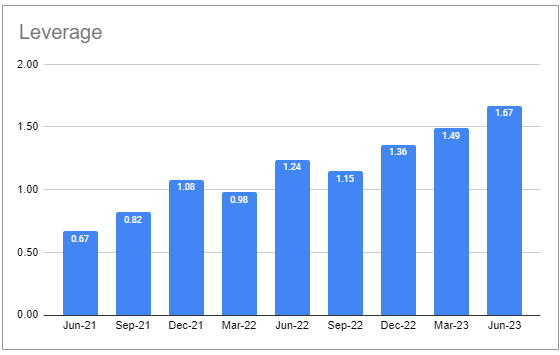

Something else that should concern investors is the fact that the company’s leverage is very elevated. Whereas the median leverage is closer to 1.15x, a TPVG figure of nearly 1.7x is very high. To be fair, net leverage is lower at 1.44x, though still very high by BDC standards.

Systematic Income BDC Tool

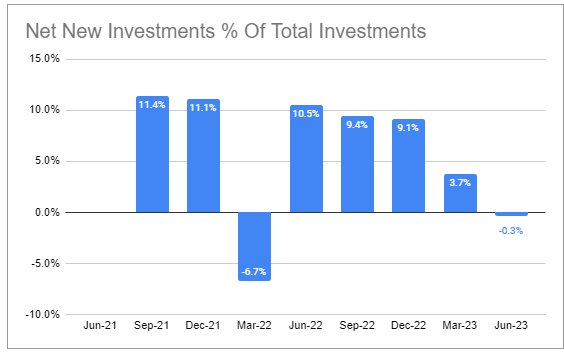

One part of this sharp rise in leverage is the drop in NAVs, but also the fact that the company was very aggressive in adding new holdings as we can see below. This has the look of a company doubling down to climb out of a hole, which can often make things worse. It also suggests that the company is not necessarily pursuing its best ideas in the portfolio.

Systematic Income BDC Tool

It’s our view that there is no reason to avoid BDCs that underperform the sector, so long as this underperformance is more than priced into the valuation. However, TPVG continues to trade at a valuation above the sector average. This may be due to some sort of fairy dust left over from another venture debt-focused BDC HTGC, which has put up fantastic numbers. Or it could be due to decent performance the company put up prior to 2021, or to a hope that TPVG could take advantage of a hole left by SVB. In any case, the combination of fairly consistent underperformance with a premium valuation doesn’t make much sense.

Systematic Income

Takeaways

TPVG stock is a BDC that never made much sense to us as a holding. It has tended to deliver inconsistent and, generally, underwhelming results while trading at an elevated valuation. More recently, its portfolio has taken a number of knocks, which speaks to significant problems in its underwriting process. We can’t exclude the possibility that a soft landing in the economy drives a rally in its NAV due to gains on the warrants and a rise in deal prepayment fees. However, this outcome can also benefit many other BDCs which don’t have the obvious difficulties in portfolio quality. We continue to avoid the company in our Income Portfolios.

Read the full article here