Thesis

Franklin International Core Dividend Tilt Index ETF (NYSEARCA:DIVI) is one of the few large ETFs to aim for a dividend-focus methodology while exposing you to international markets. The fees are fair, the performance has been relatively impressive so far, and the current yield is high enough to be worth a closer look.

I think that you cannot go wrong here, but in this post, I will nonetheless include an alternative if you’d prefer a more attractive yield at lower average earnings and book value multiples.

What Does DIVI Do?

DIVI was launched by Franklin Resources, Inc. on June 1, 2016, and is managed by Franklin Advisory Services, LLC. It currently has about $430 million in AUM and charges a 0.09% expense ratio.

It’s a smart-beta ETF that seeks to replicate the performance of the Morningstar Developed Markets ex-North America Dividend Enhanced Select IndexSM (the underlying index) which is maintained and calculated by Morningstar, Inc. The underlying index, in turn, uses as its available universe the constituents of the Morningstar Developed Markets ex-North America Target Market Exposure Index (the parent index), which range from mid- to large-cap stocks.

The goal of the underlying index is to deliver a higher dividend yield than what the parent index offers and at the same time minimize its tracking error relative to the parent in order to offer more or less the same level of exposure the parent does. This is why DIVI is named a “core dividend tilt” ETF; it’s supposed to provide the kind of access to the ex-North America developed equity markets of the parent index, but with an emphasis on dividend yield.

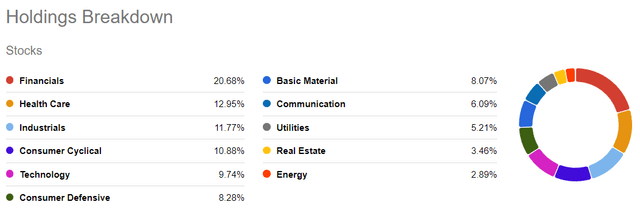

Therefore, it’s not surprising that the sector allocation profiles between DIVI and the JPMorgan BetaBuilders International Equity ETF (BBIN), which tracks the parent index, do not differ in a major way. Here are the current allocations of DIVI:

Seeking Alpha

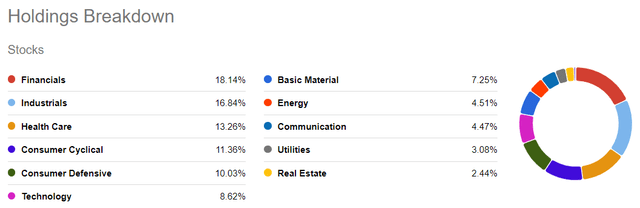

And here are those of BBIN:

Seeking Alpha

What mostly stands out is the energy weight, with DIVI allocating significantly less than BBIN there.

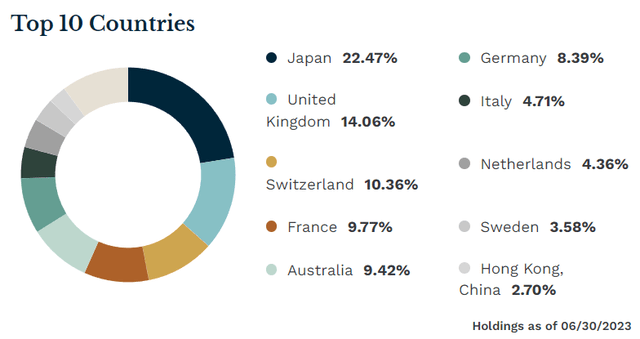

However, when it comes to DIVI’s geographical exposure profile, it’s very similar to that of BBIN. Here it is:

ETF.com

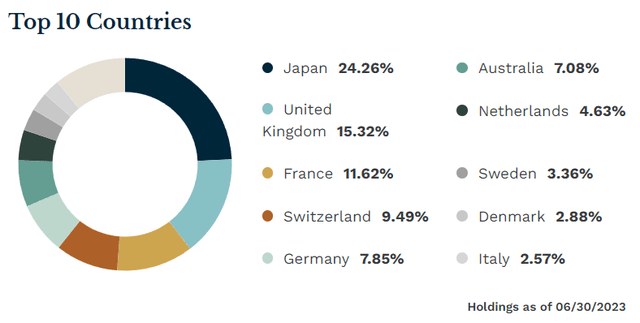

And here are BBIN’s allocations:

ETF.com

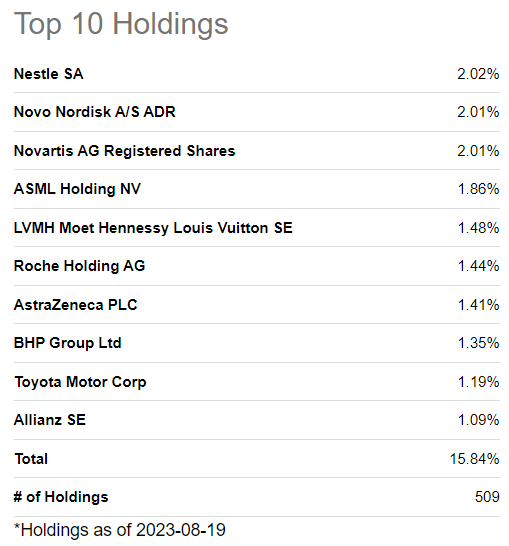

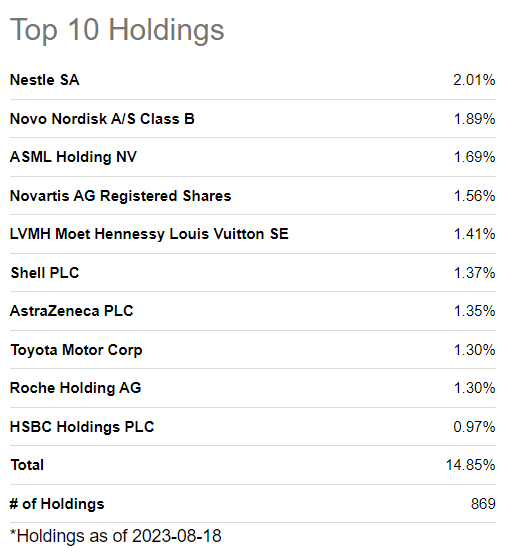

The top 10 holdings of each fund offer more insight. Here are those of DIVI:

Seeking Alpha

And here are those of BBIN:

Seeking Alpha

Observe how they’re mostly similar except for the weightings. DIVI seems to be maintaining a balance between allocating most of the funds into the holdings BBIN has and giving weighting priority to the stocks with the higher dividend yield.

Time to see how this approach has served DIVI and its investors so far…

Performance

First, let’s examine how well the ETF tracked the underlying index. As you can see from the table below, DIVI realized average annual price returns of 8.27% since it launched, while the underlying index increased by an average of 8.57% per year.

franklintempleton.com

While this looks OK, the tracking error observed between the underlying index and the parent one can appear significant (8.27% versus 9.59%). But that is to be expected when an emphasis on dividend returns is given here. In this context, I am actually surprised it’s not worse.

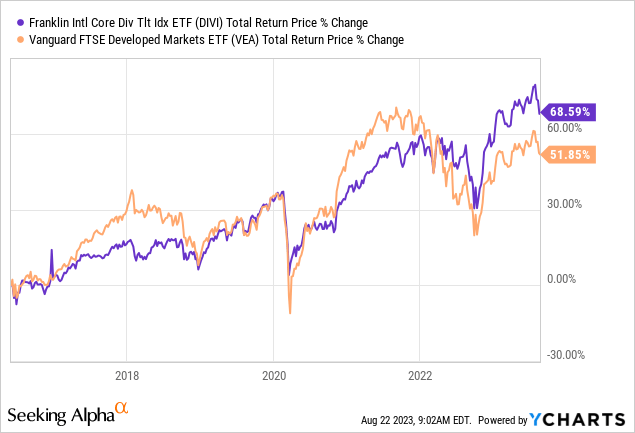

A comparison to the Vanguard FTSE Developed Markets Index Fund ETF Shares (VEA) better illustrates how well DIVI has performed:

Also, take a look at this:

portfoliovisualizer.com

So, not only has DIVI significantly outperformed its vanilla counterpart, it has done so with lower volatility, a much less severe maximum drawdown, and a lower correlation to the U.S. market, all while offering a more attractive dividend yield.

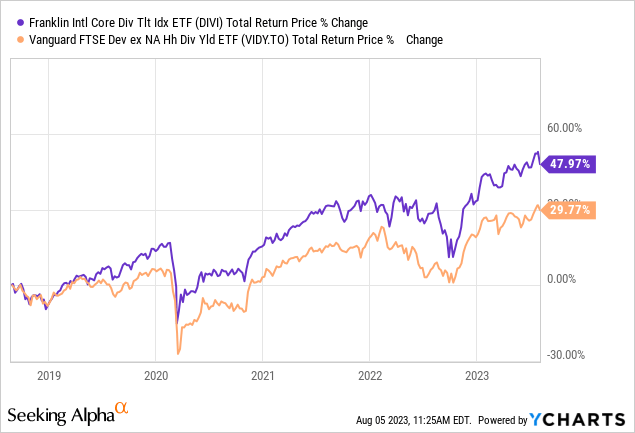

Speaking of which, I could only find one ETF that fits the profile of DIVI so well; the Vanguard FTSE Developed ex North America High Dividend Yield Index ETF (VIDY:CA). Other options would create an unfair comparison as they lack at least one of the following criteria: exclusion of the N.A. markets, similar geographical exposure, dividend income focus.

VIDY currently sports a TTM dividend yield of 4.32%. DIVI has a TTM yield of 5.82%. Due to the uncertainty of the dividend income for both funds, this difference can appear insignificant. I, myself, wouldn’t choose one or the other based on the yield. But DIVI has been around for a longer time than VIDY (06/01/2016 vs 08/21/2018), trades on USD and not CAD, charges a lower expense ratio than VIDY (0.09% vs 0.28%), manages assets about 4 times larger than VIDY’s, and has far greater trading volume.

For what it’s worth, since VIDY was launched, DIVI significantly outperformed it as well:

Yield

This is one of the rare cases where I find the selection of a smart-beta ETF so straightforward. I believe there simply isn’t any other ETF offering what DIVI does: decent yield, acceptable tracking error, similar geographical/sector exposure to the vanilla counterparts, impressive relative performance, and fair fees.

With that being said, I recently mentioned another ETF in this post, called iShares International Select Dividend ETF (IDV), which basically aims to offer international exposure with a focus on dividend income. Its TTM yield is 7.45% at the moment.

However, this fund includes the Canadian market and has a very large exposure to it at that. In short, it is far from offering an accurate representation of the global market. But if you have no problem with this, the yield is not the only attractive aspect here; it also trades at a net P/E ratio of 5.76 and a P/B of 0.87. These averages look very good when compared to those of DIVI (P/E: 11.42 and P/B: 1.58).

Risks

Now, if you are considering buying DIVI, make sure to understand the risks involved by examining the prospectus. Here, I will briefly mention the most significant ones:

- Market risk: DIVI is exposed to the usual dangers that come from investing in foreign markets, such as political and regulatory developments that can negatively impact a country’s equity market.

- Foreign stock risk: Since the ETF invests in stocks outside the U.S., that introduces some new risks like more volatile equity markets and subpar accounting/reporting standards.

- Concentration risk: The fund’s index doesn’t place any allocation restriction in order to efficiently track the global market and it is, therefore, subject to concentrating in a particular sector or industry.

Verdict

In conclusion, DIVI offers an efficient way to track the performance of the ex-North America developed markets around the world while enjoying a superior yield. Also, the fees are low enough, considering it doesn’t face any serious competition as far as I can see.

I rate this as a BUY, but I would nonetheless pick IDV over it because I don’t really mind perfectly tracking the global market as much as I care about getting international exposure for as cheap as possible, valuation-wise.

What about you? Let me know in the comments and let’s start a discussion. I would love to know your thoughts about this. Thank you for reading.

Read the full article here