DICK’S Sporting Goods (NYSE:DKS) declined over 20% immediately following Q2 results. Slashed profit guidance was the primary culprit. And this was due in a large part to issues surrounding retail theft (“shrink”) as well as to softness experienced in their outdoor category.

But all else considered, results weren’t overly disappointing. The company increased transactions and continued to gain market share. They also reported better than expected comparable sales growth, while also making strides in new store openings.

Perhaps the significant pullback following the release was overdone. In one day, DKS lost all its year-to-date gains. And following the losses, shares are now down 3% during the period.

Seeking Alpha – DKS Basic Trading Data

DKS may provide just the right opening for opportunistic investors seeking to capitalize on the recent selloff.

DICK’s Sporting Goods Q2 Results

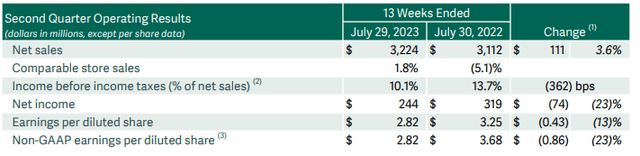

DKS reported total overall sales of +$3.2B in Q2. This was up 3.6% YOY but +$20M shy of consensus estimates. Comparable store sales, on the other hand, grew 1.8%, surpassing estimates for a 1.1% gain. This was driven primarily by a 2.8% increase in transactions, as well as by gains in market share.

Gross margins came in at 34.4%, down from 36% in the same period last year and the 36.5% reported in the prior quarter. Similarly, operating margins were also lower at 10.1%. This compares to 13.7% and 11.6% last year and in the prior quarter, respectively.

DKS Q2FY23 Earnings Release – Snapshot of Q2 Operating Results

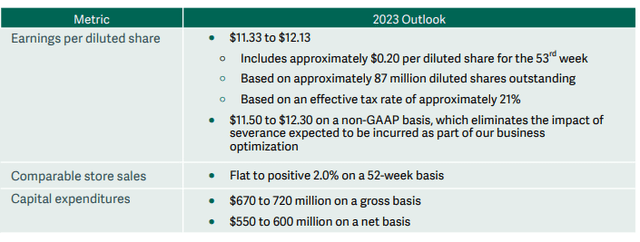

At the bottom line, EPS was $2.82/share, nearly $1.00/share lower than consensus. Looking ahead, DKS did leave their comparable sales expectations intact, with flat to 2% growth. But they significantly lowered their EPS range to $11.33/share to $12.13/share. This represents a midpoint of $11.73/share compared to a prior midpoint of $13.35/share. Consensus targets were also forecasting full-year EPS to be higher at $12.03/share.

DKS Q2FY23 Earnings Release – Summary of FY23 Guidance

Why Did DKS Stock Decline Following Results?

DKS dropped over 20% immediately following the release. This was most likely attributable to the significant cut in the full-year EPS range because of declining margins relating to shrink.

In addition, DKS also guided for approximately +$20M of severance-related expense in Q3 as part of their efforts in streamlining their overall cost structure, an aspect of which includes the elimination of certain positions at their customer support center. The savings should offset the severance costs, but these will be realized more gradually over the next twelve months.

DKS was also at heightened risk of a pullback, given their YTD performance leading up to the release.

What Is The Outlook For DKS Stock?

Consistent with my prior update on DKS, I continue to view the outlook as positive. The issues DKS had during Q2 were primarily related to shrink, which impacted profitability during the period as well as their forward expectations.

The demand drivers, however, appear in line with my expectations. The company opened seven new stores during the period and retained guidance for capital expenditures. This shows the management team is committed to growing their stores, especially the specialty concepts.

Overall retail spending on sporting goods also remains strong, as evidenced by the growth reported in the Commerce Department’s monthly release. The demand strength also was reflected in DKS’ results, which showed a comparable sales beat, as well as growth in transactions and market share gains.

Participation in team-based sports also is seen as synonymous with essential spending, since equipment, such as bats, gloves, and masks, often need replacement. This creates a healthy runway for the in-place demand drivers.

Is DKS Stock A Buy, Sell, Or Hold?

In one sense, DKS was at heightened risk of a pullback heading into their release. As of the close of trading yesterday, for example, the stock was up over 20% YTD and was sitting on gains of over 30% during the past year.

With heightened attention on profitability, markets were understandably disappointed in the slashed profit outlook. The additional costs expected to be incurred as part of their business optimization strategy likely caused further disappointment.

But all else, DKS appears to be on track. They are making progress on store openings, specifically those relating to their immersive House of Sports. In addition, despite the miss on overall sales growth, they still beat on the more important comparable store sales metric. And they also continued to gain market share.

The restarting of student loan repayments does pose a potential headwind to sales, but DKS hasn’t struggled yet in this area. In fact, the demand drivers largely remain in-line. Sure, the company did experience softness in their outdoor category. But weather-related factors could have played a part in this. The primary issue, instead, appears to be related to shrink. And on this, it’s not an issue unique to DKS. For opportunistic investors, it’s worth seeing past this.

With the pullback, shares trade at a more attractive forward valuation. At about 10.2x forward earnings, the stock still trades below their five-year historical average. Consensus estimates saw shares fairly valued at about $155/share prior to today’s release. This will likely be scaled back but likely not to the $120/share level. The negative guidance revision was a setback. But, in my view, for more longer-oriented investors, the significant post-release decline presents an attractive buying opportunity.

Read the full article here