Originally published on August 3, 2023

By Mark Paris, Chief Investment Officer, Head of Municipal Strategies, Invesco Fixed Income | Stephanie Larosiliere, Head of Municipal Business Strategies and Development

Here’s our monthly update on what’s going on in the muni market. We ask and answer key questions and highlight munis by the numbers, providing a quick look at some commonly used muni market datapoints. Here’s our insight for August.

Stephanie: There’s a lot of chatter about a potential start of a bull market in Muni bonds during the last few weeks as mutual fund flows turned positive. Do you think we’re there yet?

Mark: I’d love to say that the munis have officially entered bull market territory, but I think it’s too early to tell. It certainly feels good to see positive inflows following months of outflows. Investors put about $1 billion into muni funds during the week ending July 19 – the largest weekly inflows since January 2023.1 That was followed by over $550 million coming in the week ending July 26. While that’s great, flows to muni funds are still negative year-to-date for 2023, with approximately $6.8 billion of outflows.2 We’re significantly ahead of where we were this time in 2022, when year-to-date outflows hit $80.6 billion. Meanwhile, flows to ETFs are solidly positive, at about $2.8 billion year-to-date.2

Stephanie: Let’s talk market technicals. Are the summer months panning out how you expected? Have we seen the net negative issuance seasonality that we’ve been hoping for?

Mark: Yes, so far, the summer months are shaping up as expected. New issuance tends to be low in July and August and that’s on top of the already low supply in 2023, which is down 15% compared to the same period in 2022.3 I expect new issuance to stay low through the end of 2023, which has the potential to be a positive for muni bond prices.

Stephanie: It also seems like munis have been decoupling from Treasuries in the last few weeks. Tax-exempts are holding up well amid Treasury market volatility and have outperformed Treasuries as volatility continues. Have we turned a corner?

Mark: Typically, the need for tax-exempt income is one of the biggest driving factors of how the muni market directionally performs. But since the beginning of 2022, it seems that macro factors like the Treasury market and inflation have mattered more. I can’t say for sure that we’ve turned a corner, but over the last couple of weeks it feels like we’re getting back to the “old” muni market where taxes, technicals, and credit are stronger drivers of performance.

Stephanie: And if we didn’t have enough to contend with on the macro side of things, on August 1, Fitch Ratings downgraded the US sovereign rating from AAA to AA+.4 What do you think this means for munis?

Mark: I think the effects will be limited, not like the 2011 S&P US downgrade, which was closely followed by actions on municipal credits that were directly linked to the US government.5 It’s also unlikely that we’ll see the Treasury market volatility that we saw in 2011, especially given that the US economy is so much different today. The US economy has proven to be resilient in recent months, with a tight labor market further proving that point. It’s very different from spring and fall of 2011, when the unemployment rate ranged between 9.0% and 9.2%.6

Munis by the numbers

A quick look at some commonly used municipal market datapoints.

Fund flows: Weekly and monthly reporters in $ millions, Week ending July 26, 2023

Source: Lipper US fund flows, and JP Morgan, as of July 26, 2023. YTD = year to date.

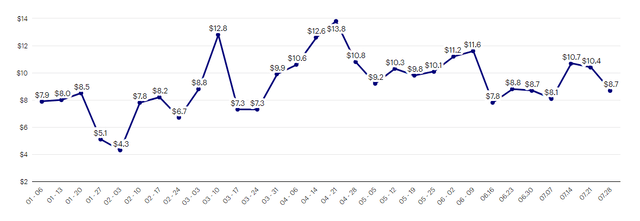

30-day visible supply (billions)

Source: The Bond Buyer from January 6, 2023 – July 28,2023. The 30-day visible supply is compiled daily from The Bond Buyer’s Competitive and Negotiated Bond and Note Offerings calendars. It reflects the dollar volume of bonds expected to reach the market in the next 30 days. Issues maturing in 13 months or more are included.

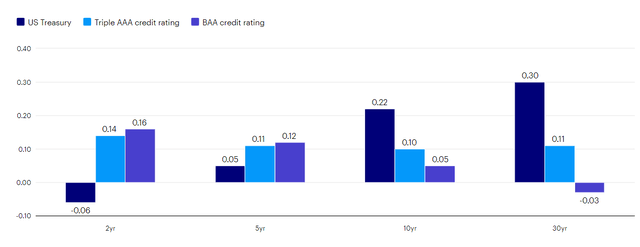

One-month yield change: 7/3/23 – 8/2/23 (percent change)

Source: Refinitiv MMD Curve, and US Department of Treasury, from July 3, 2023 – August 2, 2023. A credit rating is an assessment provided by a nationally recognized statistical rating organization (NRSRO) of the creditworthiness of an issuer with respect to debt obligations, including specific securities, money market instruments, or other debts. Ratings are measured on a scale that generally ranges from AAA (highest) to D (lowest); ratings are subject to change without notice.. For more information on rating methodologies, visit the following NRSRO websites: www.standardandpoors.com and select ‘Understanding Credit Ratings’ under Rating Resources ‘About Ratings’ on the homepage; www.ratings.moodys.com and select ‘Rating Methodologies’ under Research and Ratings on the homepage; and www.fitchratings.com and select ‘Ratings Definitions Criteria’ under ‘Resources’ on the homepage. Then select ‘Rating Definitions’ under ‘Resources’ on the ‘Contents’ menu.

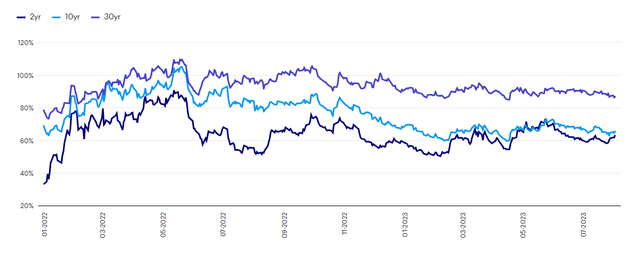

Municipal/Treasury ratio

Source: Thomson Reuters TM3, as of August 2, 2023. Treasuries are backed by the full faith and credit of the US government as to the timely payment of principal and interest, while legislative or economic conditions could affect a municipal securities issuer’s ability to make payments of principal or interest.

Footnotes

- * A call option is a derivatives contract giving the owner the right, but not the obligation, to buy a specified amount of an underlying security at a specified price within a specified time.

- Source: Refinitiv Lipper US Fund Flows, as of July 19, 2023.

- Source: JPMorgan, as of July 31, 2023.

- Source: The Bond Buyer, as of July 25, 2023.

- Source: Fitch Ratings, as of August 1, 2023.

- Source: Standard & Poor’s, as of August 5, 2011.

- Source: US Bureau of Labor Statistics, as of August 5, 2011.

Important information

NA3051961

Municipal securities are subject to the risk that legislative or economic conditions could affect an issuer’s ability to make payments of principal and/or interest.

Junk bonds involve greater risk of default or price changes due to changes in the issuer’s credit quality.

The value of investments and any income will fluctuate (this may partly be the result of exchange rate fluctuations) and investors may not get back the full amount invested.

The values of junk bonds fluctuate more than those of high-quality bonds and can decline significantly over short time periods.

All fixed income securities are subject to two types of risk: credit risk and interest rate risk. Credit risk refers to the possibility that the issuer of a security will be unable to make interest payments and/ or repay the principal on its debt. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa.

Municipal bonds are issued by state and local government agencies to finance public projects and services. They typically pay interest that is a tax in their state of issuance.

Because of their tax benefits, municipal bonds usually offer lower pre-tax yields than similar taxable bonds.

All data as of August 3, 2023, unless otherwise stated.

All data provided by Invesco unless otherwise noted.

The opinions expressed are those of the author, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. It is not intended or written to be used, and it cannot be used by any taxpayer, for the purpose of avoiding tax penalties that may be imposed on the taxpayer under US federal tax laws. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation.

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial professional before making any investment decisions.

Past performance does not guarantee future results. An investment cannot be made into an index.

Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions, there can be no assurance that actual results will not differ materially from expectations.

There is no guarantee the outlooks mentioned will come to pass.

©2023 Invesco Ltd. All rights reserved

Thoughts From The Municipal Bond Desk by Invesco US.

Read the full article here