Today I’m taking a look at Genco Shipping & Trading Ltd (NYSE:GNK), a shipping company operating in the dry bulk segment. The company reported their Q2 2023 earnings a few days ago, beating estimates on both EPS and revenue. More specifically, Genco reported an EPS figure of $0.27 per share, beating estimates by $0.07, while revenues reached $90 million for the quarter, outperforming estimates by $30 million. In this article I will explain why these results are the starting point of putting the company in my radar for a long position, by taking a look at factors which, in my personal opinion, will help the share price increase in the next quarters.

Fleet structure and modernization

The company currently owns a total of 44 vessels, comprised of 17 Capesize and 27 Ultramax / Supramax vessels. The average fleet age is 11 years, with older vessels being in the Supramax segment. As I’ve written many times in some older articles about shipping companies, larger vessels are associated with higher volatility of freight rates, while smaller vessels are more versatile and provide more stable returns. What I like in Genco, is they have structured their fleet in such way, so that they can go after higher returns in their Capesize segment, while keeping their overall risk lower, with their Ultramax / Supramax segment.

In addition, despite their medium average fleet age, the company has completed the fitting of scrubbers in all of their 17 Capesize vessels. Therefore, they are in a position of taking advantage of the VLSFO/HSFO oil price differential. However, at this point, this spread has decreased substantially, as compared to the summer of 2022.

Finally, the company’s management is committed to renewing their aging fleet. This was also confirmed by the company’s CEO in their latest earnings call.

Index-linked time charter contracts

The company is following a mixed strategy for their vessels, with some of them being chartered out on longer term time charter contracts. At this moment, Genco has four time charters in place, with three of them having rates that are linked to the BCI index plus a specific percentage plus an additional premium for the installed scrubbers. This is a strategy which lifts a good amount of risk in the quite volatile segment of Capesizes. The earliest expiration of these time charter contracts is in early 2024.

Strong TCE performance and balance sheet support a hefty dividend

For the three months ended in June 30, 2023, the company reported a TCE figure of $15.5k per day, compared to $13.9k in Q1 2023 and to $28.7k per day in Q2 2022. The company has also booked 61% of Q3 2023 available days at a TCE rate of $12.2k per day. In addition, Genco has a strong liquidity profile, with $53.9 million in cash and another $207 million in their revolving credit facility. At the same time, Genco’s expected breakeven rate is $9.7k for the next quarter.

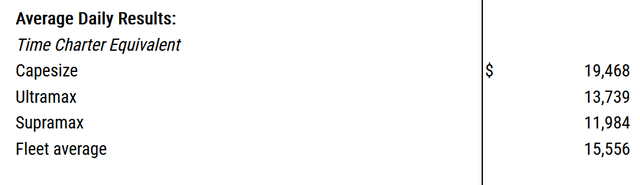

Genco’s TCE rate by vessel type (Genco’s Q2 2023 earnings report)

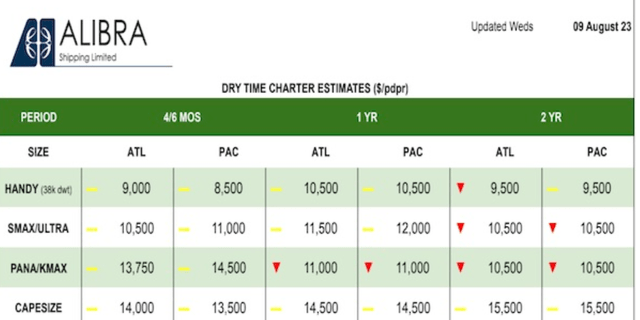

In the picture listed above you can see the TCE breakdown by vessel type, for Q2 2023. In the table listed below, you can see the current TCE rates for various vessel types. It seems that, for now, Q3 2023 TCE rates will be softer.

Current TCE rates for various vessel types (Hellenic Shipping News)

However, this quarter’s strong performance enabled the company to declare a cash dividend of $0.15 per share. In fact, based on their dividend formula, the dividend per share should be equal to $0.13, but the management decided to increase it to $0.15, by adding funds from the company’s quarterly cash reserve. At this amount, we’re looking at a dividend yield of 8.4%, which is not bad at all.

In addition, the company has taken big steps to the direction of debt reduction, reducing its debt to $153 million, from $296 million in 2021. This is a huge reduction of leverage. Moreover, the company doesn’t face any mandatory debt repayments for the next three years, although the plan to voluntarily prepay another $8.75 million of debt during Q3 2023.

Risks

The main risk of the company has to do with the performance of their Capesize vessels. In other words, if steel trade expands, Capesize rates will increase. As iron ore exports from Latin America are expected to grow and Chinese iron ore inventories are at their lowest since 2021, favorable supply – side fundamentals are developing. However, a prolonged global recession or a potential Chinese giant real estate collapse have the power to reverse these dynamics.

Such scenarios will establish the already reported trend on the TCE rate. No matter how low the break-even rate will be, with $8.75 million voluntary debt repayment announced, $5.5 million of capital expenditures, OpEx and cash reserves, there will be little to no funds for a dividend. And this could have a quite negative effect on the share price, at least for the short to medium term.

Bottom line

Traditionally, the third and fourth quarter of each year are the strongest for shipping companies. Despite the soft TCE rate, I would still opt for a long position in Genco, as Capesize returns could increase rapidly as we progress on the current quarter. After all, I believe that the company could postpone its voluntary debt prepayment or take a portion of the planned quarterly cash reserves to provide their shareholders with a better dividend. Q4 2023 doesn’t have any planned CapEx so they may be able to make up “loss” at that time. So, an investment in Genco is justified, in my opinion.

Read the full article here