Arcos Dorados Holdings Inc (NYSE:ARCO) is recognized as the largest restaurant operator in Latin America and the Caribbean, leveraging the McDonald’s Corp. (MCD) brand recognition through more than 2,317 franchise locations. It’s fair to say consumers in the region are Lovin’ It, based on the impressive growth the company has seen accelerate since the pandemic.

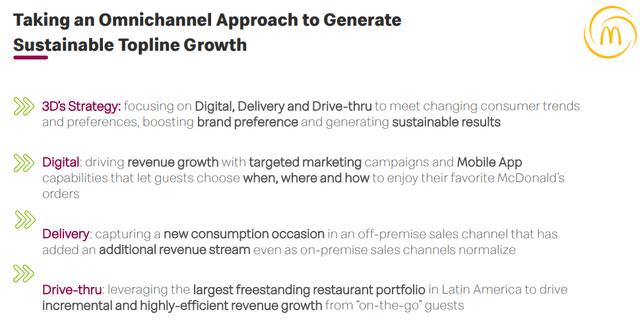

Indeed, the company just reported its latest quarterly results highlighted by record systemwide sales, finding success in its “3D’s Strategy” focusing on Digital, Delivery, and Drive-thru initiatives to support higher earnings.

This is a stock we covered back in 2021 with a bullish note and can reaffirm that position here with an expectation for more upside. While shares are currently under pressure amid broader market volatility, our take is that fundamentals remain positive with shares well-positioned to rebound.

ARCO Q2 2023 Earnings Recap

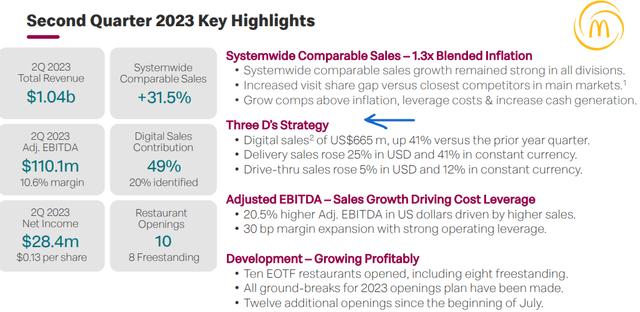

Arco reported Q2 EPS of $0.13, up from $0.07 in the period last year, and in line with expectations. Revenue reached $1.0 billion, increasing by 17.1% from Q2 2022.

Considering the smaller portion of the business based on sub-franchising to separate operators, total systemwide comparable sales were 31.5% higher y/y. Management explains that this figure is evidence of the underlying momentum in restaurant traffic across the region and also reflects market share gains against quick-service restaurant competitors.

We mentioned the Three D’s strategy, digital sales capturing orders placed online or through in-store kiosks climbed by 41% y/y driven by investments in the technology and wider customer adoption. Separately, delivery sales increased by 41% in constant currency which has represented a new growth opportunity at many locations.

The idea here is to support higher margins and profitability between optimized pricing and cost savings. The efforts appear to be working as the adjusted EBITDA margin of 10.6% climbed from 10.1% in Q1 and 30 basis points higher from the period last year.

source: company IR

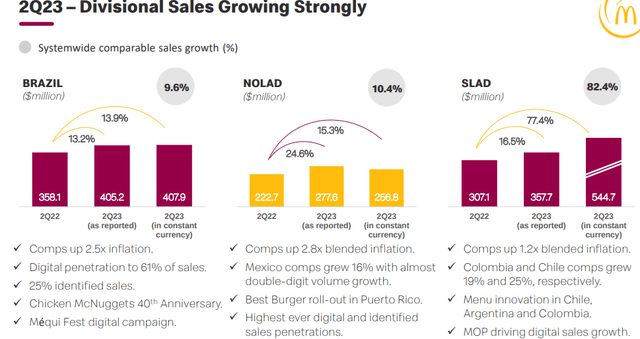

By division, the operational strength has been across the board, outpacing inflation in the region as a benchmark. With Brazil contributing approximately 40% of total revenues, comparable sales in the country were up 10% y/y. Within the Northern Latin American division (NOLAD), Mexico was a standout, with comp sales up 16%. Overall, Arcos opened 10 new restaurants during the quarter, continuing its trend of steady expansion in the region while targeting geographic diversification.

Finally, we’ll note that Arcos ended the quarter with a balance sheet position between $222 million in cash and equivalents against $695 million in long-term financial debt. Considering $52 million in adjusted EBITDA over the last twelve months, we consider the net leverage ratio at 1.1x as stable and positive within the company’s investment profile.

source: company IR

What’s Next For Arcos Dorados?

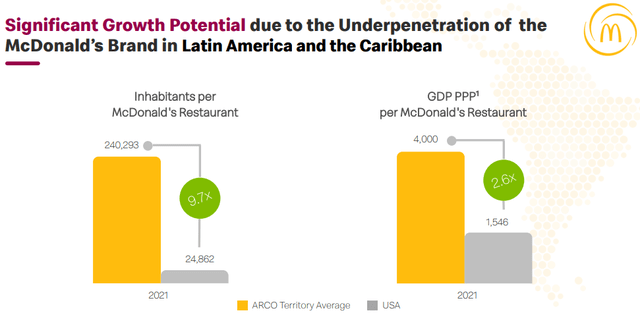

Beyond what we view as solid financial metrics and operating trends, we make the case that this is a growth story still in the early stages. The data that stands out to us, is the market research from Arcos suggesting the McDonald’s brand and total restaurant locations in the territory remain significantly underserved compared to the USA as a benchmark.

For example, while there are approximately 25k people per McDonald’s location in the USA, that figure is nearly 10x higher in the Latam and Caribbean regions. While we don’t see a convergence anytime soon, the potential to just narrow that spread through new restaurant locations highlights the significant growth runway for Arcos that could play out over the next decade.

source: company IR

The efforts to modernize and push technology into traditionally “low-tech” fast food provide a new facet for growth adding to the convenience and reputation of quality that comes with the McDonald’s brand.

At the end of the day, digital ordering options and new consumption channels like delivery and drive-through format both add to the top line and generate financial efficiencies. We expect the company to continue and will look for the adjusted EBITDA margin to trend higher as a key monitoring point.

source: company IR

Is ARCO a Good Stock?

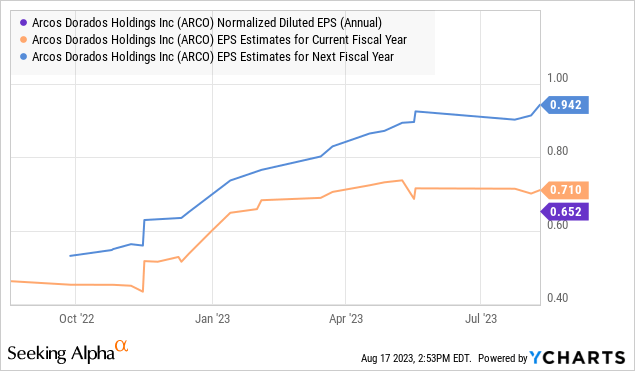

According to the consensus, ARCO EPS is expected to reach $0.71 this year, up 9% compared to 2022. Looking ahead, the market sees earnings growth accelerating in 2024 toward $0.942 per share, an increase of 33% higher.

This would be achieved through some upside in margins, getting past the inflationary cost pressures that defined 2022 and the start of this year. The bullish case for the stock is that there is an upside to these estimates which we believe could be achieved on the demand side supporting a higher top-line.

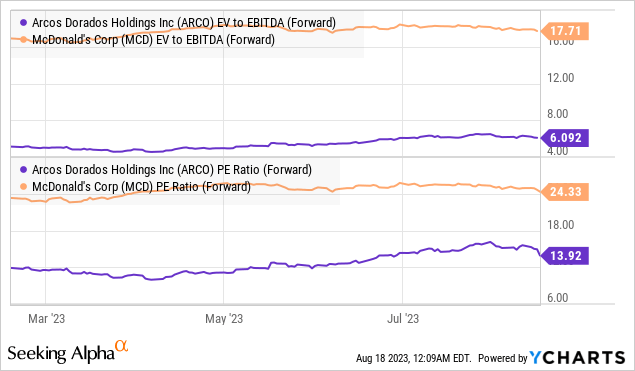

In terms of valuation, ARCO is trading at a forward EBITDA multiple of just 6x or 14x on its 2023 consensus EPS. Notably, both metrics are a deep discount relative to its brand partner McDonald’s Corp. While we agree that MCD as a global leader deserves a premium, we’d also say that ARCO’s strong outlook and long-term potential justifies a higher multiple, narrowing the valuation spread.

ARCO Stock Price Forecast

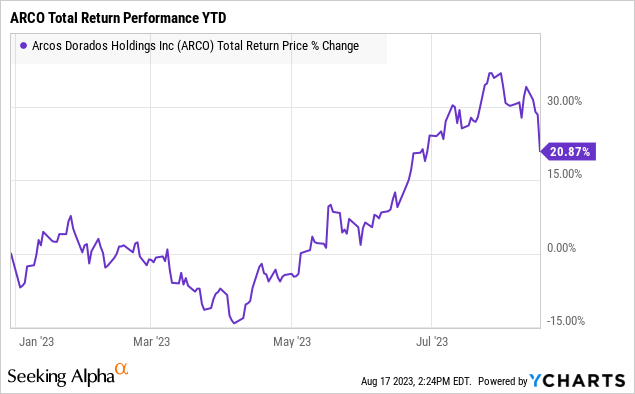

From the long-term stock price chart, it’s important to note that shares of Arco are trading around a price of $10.00 is near its highest level from the past decade. We can blame the wide swings of volatility on macro disruptions and FX headwinds, but there is also a thought that the outlook is stronger today than at any time in the past.

Seeking Alpha

Zooming into the chart, ARCO has been trending higher over the past year, outside of this latest correction off the earnings report which we could connect to a “sell the news” type of market reaction.

In recent weeks, the main market story has been renewed global growth concerns and a rebound in the US Dollar translating into some weakness in emerging markets and shares of ARCO, now down -13% from its recent high.

At the same time, we believe this current pullback could signal a new buying opportunity with shares offering good value in the area of technical support.

Seeking Alpha

Final Thoughts

There’s a lot to like about Arcos Dorados as a leader within the consumer discretionary sector of Latin America. We rate ARCO as a buy with a price target of $14.00 for the year ahead representing a 20x multiple on the current consensus 2023 EPS.

The way we see it playing out is that continued economic resiliency should be positive for the operating backdrop, opening the door for Arcos to outperform expectations. Declining cost pressures through easing inflation should help support margins and earnings through the end of the year as a catalyst for the stock.

In terms of risks, even as the McDonald’s brand maintains a “defensive” aspect to changing economic conditions, sharply weaker economic conditions would undermine the growth trajectory. Softer sales trends or disappointing margins in the next few quarters could lead to a deeper selloff in the stock.

Read the full article here