I have tracked Partners Value Investments (TSXV:PVF.UN:CA) (OTC:PVVLF) for the last 2 years and kept a reasonably detailed model. PVF is a very obscure company sitting atop Brookfield Corporation and Brookfield Asset Management. The purpose of the vehicle is to provide control over the corporate structure to senior Brookfield partners.

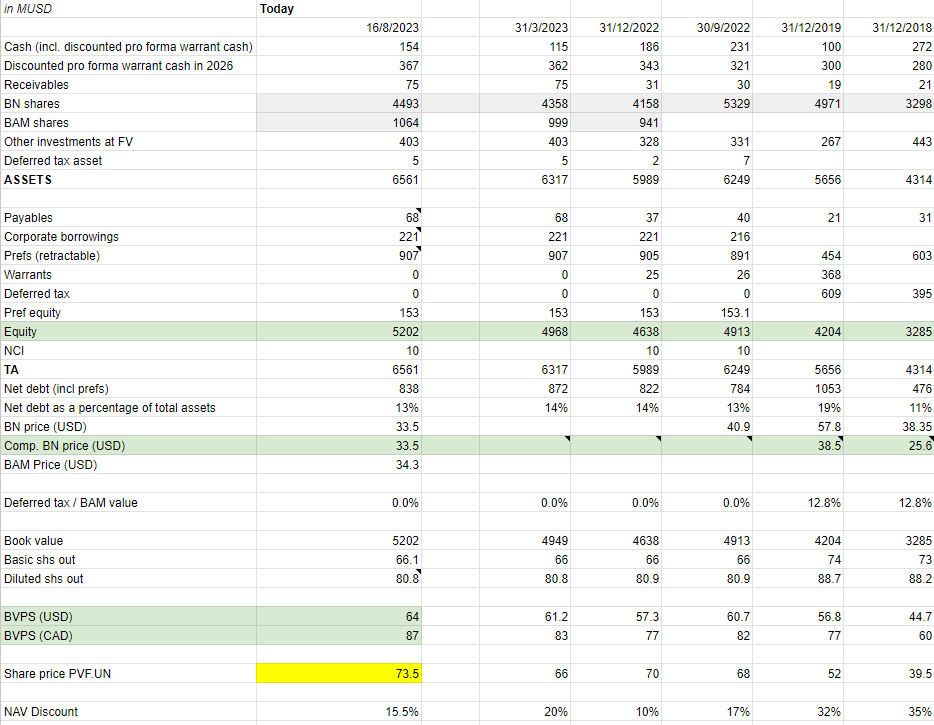

The following SOTP table is based on quarterly filings of PVF.

Author’s calculations based on Partners Value Investments public filings

We can see that most (in fact around 70%) of the values lies in ownership of Brookfield Corporation (BN), followed by Brookfield Asset Management (BAM) shares as a result of the 2022 Q4 spin-off.

Note that my “today” column updates the share prices of BN and BAM to today as opposed to Q1 quarter end in the next column.

Remark as well that the “discount pro forma warrant cash” table item is not something PVF reports on its balance sheet. This item is based on my understanding of cash injection from the deep in the money warrants that will expire in 2026. As the share dilution will be almost certain and there is no PVF dividend in the interim, I discount the cash back at 6% discount rate to reflect time value of money.

Today the NAV discount sits at 15.5%. This sounds low, before you consider the fact that

-

PVF’s main holding is BN, itself 50% undervalued as documented in my Seeking Alpha article on BN

-

PVF has been buying back around 10% of shares in substantial issuer bids (SIBs) in each of the last two years. PVF did this by issuing new preferred equity. Together with the very small normal course issuer bid (due to severely limited liquidity), I estimate the annual per share accretion to be around 1.5% right now

Regarding the latest substantial issuer bid in autumn 2022, Brookfield issued new preferred equity. I believe there are two reasons for this

-

Brookfield’s senior leadership believes in the underlying holdings and wants to remain slightly leveraged to it (see table). Net debt has ran in the mid-teens of total assets, and total assets are compounding

-

There might be tax deferral advantages to shareholders tendering for preferred equity as opposed to cash: indeed, the SIB and NCIB were done at very similar price levels, yet with widely different volume outcomes (SIB reached 10% of shares outstanding tendered, while NCIB is unsuccessful at very similar price levels)

Obviously this strategy of issuing new preferred is accretive win-win for everyone, including remaining shareholders.

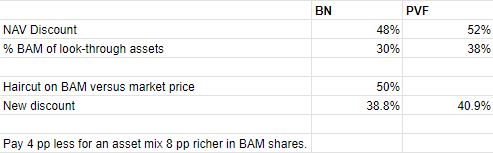

BN versus PVF: How to think about the relative valuation and exposures

As I wrote a long BN write-up article on Seeking Alpha as well, I think about the opportunity cost of owning BN versus PVF. According to my article, BN is currently undervalued by 48%, while 40% of that NAV comes from owning BAM as full market price.

In contrast, when you buy PVF (and taking into account said numbers), you buy at a look-through NAV discount of 52%. Here’s the numbers (and please refer to my BN article for a detailed breakdown).

Author’s calculations based on company documents

Note that PVF’s balance sheet cash and investments net almost exactly the liabilities today, so this gross value pillar was disregarded.

We find that buying PVF gets us 4 percentage points higher discount, but at the ‘cost’ of owning 8 percentage points more BAM at (arguably full priced) market price. Because it is a bit difficult to conceptualise what this means if you are sceptical about paying up full price for BAM, I made the following simulation.

Author’s calculations based on company documents

Even if you are only willing to pay half market price for BAM, PVF underlying’s NAV discount would still be 2 percentage points greater. In fact I simulated that you need to believe BAM is worth less than 20% of its market price for you to believe BN has a bigger NAV discount than PVF.

Another way to look at this is by valuing BAM at full market price and looking at the BN asset heavy stub. If we do this, we find that a higher percentage, i.e. 78%, of PVF’s share price is covered by underlying BAM shares, and the stub is valued at 80% discount (just like the stub discount at BN).

But what about liquidity you say? I would counter that the argument of >1% ongoing accretion from the PVF buyback offsets the low liquidity disadvantage for me personally as a long-term holder.

Senior management is recycling capital from BAM into BN

Interestingly, in its Q1 filing, PVF has reported ownership of 134 million shares of BN and 30 million shares of BAM. This is not the original spin-off ratio of 4-to-1 shares, and PVF previously reported a balance of 132 million BN shares.

We concluded that senior management has decided to sell around 2.5 million BAM shares (9% of the original allocation) and used this cash to buy more BN during Q1. Management seems to agree with my Brookfield Corporation (BN) article elsewhere on Seeking Alpha that BN is relatively undervalued compared to BAM.

Summary

I believe there will always be a 15% discount for PVF compared to its underlying assets. However, management is acting on this by having done substantial issuer bids in 2022 and 2021. If this continues, this buyback policy creates a value accretion per share on top of BN’s and BAM’s return of 15% times 10% or 1.5% p.a.

PVF also has a policy of remaining slightly levered (in the low teens compared to assets) to the success of Brookfield, by using hybrid instruments such as various preferred equity types.

On top of this, PVF pays no dividends itself, and reinvests all dividends received from BN and BAM. This allows some tax efficiency for some foreign investors taxed on distributions.

In summary, PVF is a way for very long-term oriented investors to be slightly levered to Brookfield Corporation and Brookfield Asset Management, and should compound slightly quicker thanks to buyback accretion.

Risks

On top of the risks outlined by Brookfield Corporation and Brookfield Asset Management (high leverage in the subsidiaries, principal agent problem with private equity management, political backlash), PVF additional risks make it only suitable for diligent and very long term oriented investors. The following are the most relevant additional risks.

Extreme illiquidity: sometimes no trades in a day

Publicly traded partnership tax risks: for example, the SEC requires a 10% sales tax on US publicly traded LP’s since 2023. For now, PVF has always issued qualified notices to avoid foreigners from getting taxed 10% at sale, but there can be no absolute assurance this will continue.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here