Dear readers/followers,

You may recall some previous coverage of a Belgian company (currently the only Belgian company I own), with the name of Etablissementen Franz Colruyt (OTCPK:CUYTF). My last article on the company was back in 2022. Back when I wrote about the company, I called it “one of the most undervalued grocers in all of Europe”. And while we have seen some recovery for the company, we haven’t seen much. My position is up through a combination of both FX and appreciation.

There are many things to like about Colruyt. The company has a distinct home market advantage, similar to Axfood (OTCPK:AXFOY), a company I recently provided an update on. My watchlist position is still what I have – I did not add more unfortunately, but I may do so on a forward basis.

Let’s look at why I like this company and what it may offer you as an investment.

Colruyt – Plenty to like about European Groceries

Colruyt is the best sort of company – it’s a grocer, which is stable. It’s also family-owned, so there’s plenty of motivation behind it. Its main interest is the management of the Colruyt supermarket retail chains, and the corresponding subsidiaries, including stores like OKay, Bio-Planet, DATS 24, Dreamland, Dreambaby, and others.

These are not establishments that I personally frequent or even have been to. My analysis of the company is primarily based on numbers and trends. However, it has plenty going for it, including a century of tradition in the sector. What’s more, compared to Axfood, it even has a bigger market share, coming to over 30% of the Belgian grocery market.

Colruyt has a not dissimilar appeal from Axfood and similar companies more found in the “budget” segment of things. It competes with more publicly-listed grocers, including Ahold Delhaize (OTCQX:ADRNY), a company that I invest more money into – at least at this time. Its sales argument is pricing, in some cases guaranteeing the lowest regional prices.

This has been more difficult in this inflationary environment and with the margin pressures that are far more prevalent now than historically. Colruyt can be called a “discounter”, and the current environment calls for it, at times, to either sacrifice its margins or raise its prices, with either of these choices bringing quite significant issues in the longer term.

Unlike Axfood, which I reviewed not too long ago, Colruyt has significantly lower margins. Axfood has a 4.5% operating margin. Colruyt is at 2.6%. Axfood is at over 3% net – Colruyt is almost below 2%. This both highlights the advantages we see in Axfood, and also shows us the reason, or at least part of it, as to why Colruyt is currently so undervalued (though not at anything close to trough levels, which was earlier this year).

81.2% of the company’s sales are retail, with around 10% wholesale and the rest in other activities. As with most of these companies, we’re looking at a very high COGS of over 72%, as well as OpEx of almost 24%. This doesn’t leave much for operating or net income – but this is typical for grocers.

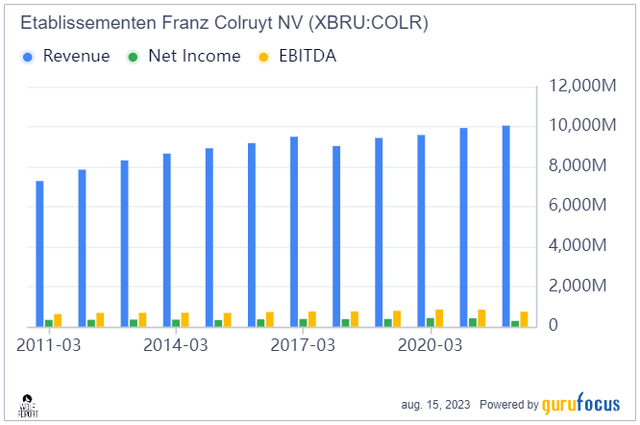

The company’s appeal most definitely lies in its stability and overall fundamental appeal. Things like this revenue trend.

Colruyt Revenue/net (GuruFocus)

As of the 1Q23 period, the company operated 744 of its own stores, 576 affiliate stores, and 321 pick-up points. However, the quarterly results haven’t changed any of the company’s challenges being faced. With the macro-economic challenges, the company expects a further decline in gross margins as Colruyt due to its status as a discounter is not to the same degree as others passing along costs to consumers.

The company’s own wording is a “remarkable net increase in operating expense” due to an increase in energy pricing, logistics, and employee benefit expenses due to automatic wage indexation, which is systemic in the home country of Belgium.

At the same time, the company is maintaining market share, and it’s continuing to invest under the stance that the challenges currently faced are of a temporary nature. There is an overall increase in net financial debt, around 1.1x net debt/leverage. This would be good leverage if it was inclusive of leases according to IFRS 16, but it’s the ex-number. As a comparison, Axfood managed ex-lease leverage of 0.3x – which puts the company’s leverage as elevated for what it is.

Colruyt has some negatives that are specific to its operating area in Belgium. Belgium is one of the only nations in all of Europe where an automatic wage indexation is applied. But it also has positive, such as the overall food inflation being lower than CPI – at least until early 2023.

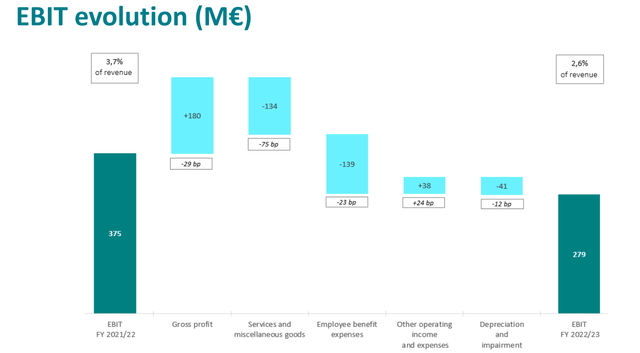

An EBIT bridge for the 2022/2023 period shines some light on the challenges faced by the company.

Colruyt IR

The company is seeing fundamental gross margin declines. Even including petrol sales, GM is decreasing by around 0.3%, which in the context of size is more than a rounding error. Excluding petrol, it’s down 0.4%. The company’s sales point of having the lowest regional prices is one of the more difficult parts of the company’s current P&L evolution.

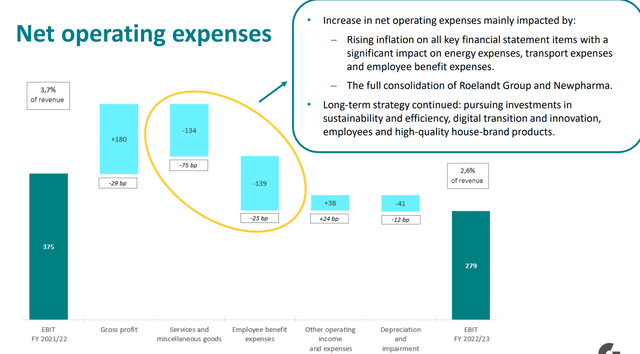

This picture of NOE gives us some image of where and how this is going.

Colruyt IR

At the same, high-level trends and consumer feedback remains positive here. The company’s results increased by almost 7%, and Colruyt added 5 new stores to its lowest-price chains, with a net add across the chain for CRU, Bioplanet, and Okay as well. Revenue growth was even better in its French segment, where results on the top line were up double digits. The company also continues to invest in French retail, opening new stores, renewing existing and doubling logistical capacity on a forward basis.

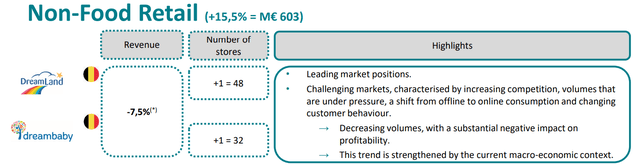

Also, let’s not forget that the company actually owns a fair bit of non-food retail. However, the numbers out of these aren’t at all as impressive as out of the food segment.

Colruyt IR

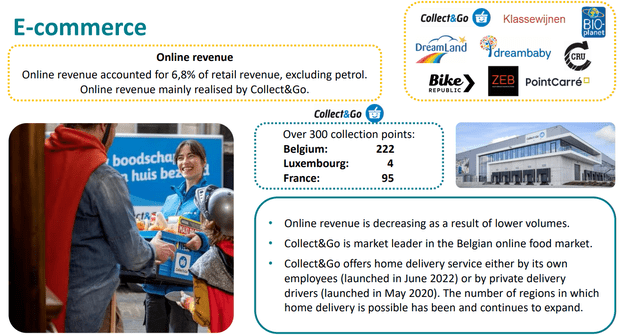

At least not for what you see above. The Bike Republic, the company’s fashion store, and other clubs/activities are up significantly – though from relatively low levels, where single or low number additions of stores still make double-digit revenue impacts. The positive here is that the company’s segments are profitable at an EBITDA level, and there are obvious synergies with its e-commerce drop points and strategies.

Colruyt IR

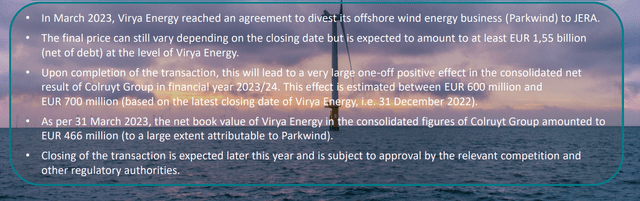

My perhaps biggest gripe with Colruyt is actually the high level. It’s my view that to make up for the margin dropoffs the company is expanding to atypical areas for its ambitions. This includes what you see above (bikes), but also something like the recent Viraya energy stake. The company has a near-60% stake in this company and is active in the development, financing, construction, operation, and maintenance of renewable energy sources, with a particular focus on offshore and onshore wind energy.

The company’s ambition also includes further investing in onshore wind energy, as well as tech such as solar and hydrogen. I’m not too thrilled in companies that start spreading operations across many, many areas. It leads to under-specialization, which in my experience not leads to actual outperformance and better income (as the company no doubt hopes), but instead a whole slew of “average” companies with only very limited upside.

Still, there’s some news here, with a sale of a wind energy business that will have a positive effect on the company.

Colruyt IR

Meanwhile, expectations are for high continued CapEx due to continued modernization, and ongoing expansion into non-food sectors – which I don’t necessarily view as a net positive for the company. That’s why, despite the valuation where this company is significantly undervalued, my PT is well below what others covering the company see here.

Let’s look at the high level and look at what we have going for us.

Valuation for Colruyt Group – There’s an upside, but it’s too small

There’s no doubt in my mind that Colruyt recently traded at a significant discount to any sort of fair value. As I mentioned in the previous segment, there were clear reasons for this. The company is looking down the barrel of significant margin challenges while also trying to grow non-food retail – not a segment I’m particularly interested in on a general level.

However, over 80% of the company is still food retail, and 10% is wholesale. So from that perspective, the company still fulfills my demand for a food investment.

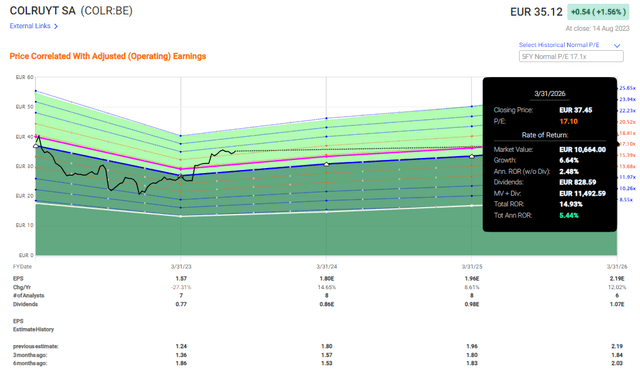

Colruyt trades on the native Belgian symbol of COLR, which is also my recommendation that you invest prior to the ADR, given liquidity. The company, despite what I said in terms of challenges, trades at a normalized P/E of around 21x. This is normalized. Less than half a year ago it was at around 11x P/E. So we’ve seen a significant improvement in a short time because the company was judging by every metric, far too cheap.

Colruyt these days trades at a normalized P/E premium of about 17-18x, which is below the typical EU average, with Axfood trading closer to 23x. The company also has a meager yield – only 1.6% at today’s valuation, and little chance for that growing massively as I see it.

The company has decent reversal forecasts. The fiscal 2024E is expected to bring about a reversal of about 15% EPS growth, but this was from a 27% decline in the 2023 fiscal. Beyond that, it’s about 7-9% growth rate on average.

Because much of the reversal has already taken place, the upside is limited, as I see it – but it’s there. In fact, due to the low yield, if we use 17x P/E as a forecast average, the company doesn’t even manage 6% annualized due to the valuation reversal we’re seeing here.

Colruyt Upside (F.A.S.T. Graphs)

Colruyt actually has a lot of things in common with Carrefour (OTCPK:CRRFY) (OTCPK:CRERF), a French Hypermarket stock I’ve owned and made a profit on. The company is a superb buy at a discount. The reversal potential is nothing short of massive, as we’ve seen here, close to doubling in share price.

Beyond that though, there are reasons for being careful when investing in this company – because the downside or average potential for this company is not as good as you think. If you invested any time after 2005, your returns here would be below 5%.

Other analysts agree with my assessment of the company. Colruyt is estimated to be worth between €20-€40/share with an average of €29/share by 10 analysts from S&P Global, only one of which has the company at a “BUY” recommendation at this time.

I add my voice to this chorus and give the company a PT of €30/share. This is my thesis for Colruyt.

Thesis

- The company does come with an ADR, but I don’t view the ADR as all that great. It isn’t liquid, it’s a 0.25X ADR, and I would say that in every way, the native ticker is far more appealing.

- Otherwise, Colruyt is a great grocer – as a grocer – but the main issues to the company are competition and resulting market share erosion and other operations – but in my view, the company can handle these margin issues with relative ease. It’s the company’s new investments that have me pause a bit and give the company a lower valuation target.

- What you’re investing in is one of the most profitable retailers on the entire European continent, with a good yield, and at a superb valuation with what I view as a massive upside.

- I view the company as a “hold” – and I would discount it based on its expansion plans, coming to a PT of €30/share.

Remember, I’m all about:

1. Buying undervalued – even if that undervaluation is slight, and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

2. If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

3. If the company doesn’t go into overvaluation, but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

4. I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside based on earnings growth or multiple expansion/reversion.

The company is no longer undervalued, and I would consider it to be a “hold” at this particular time.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here