With rising real estate costs, it seems impossible for a lot of people to get ahold of some real estate. With limited supply across the U.S, my prediction is that property prices remain elevated.

Thankfully, REITs are a viable option for a lot of folk and is one of my personal favorite ways to get the real estate exposure I would like. Let’s discuss a REIT that has upside potential, a steady dividend payment, and has a portfolio of diversified properties. I think that the retail space is still well and alive and Alpine Income Property Trust (NYSE:PINE) is a great candidate to get a slice of those profits while simultaneously giving you some real estate exposure.

PINE has a well covered dividend, a dividend growth rate over 37% since IPO, a variety of diversified tenants in their portfolio, and is currently undervalued.

Overview

Alpine Income Property Trust operates as a net lease real estate investment trust focusing on commercial properties that are leased to high quality companies and high credit-rated tenants.

A net lease is an agreement in which a lessee is responsible for paying some or all of the property taxes, insurance, upkeep, and maintenance expenses associated with the property. With PINE, this leaves a lot of liability and risk off of their end of the table which can enable more profitable margins.

PINE is externally managed by CTO Realty Growth (CTO) which happens to also be publicly traded. CTO’s credentials and management has a proven history.

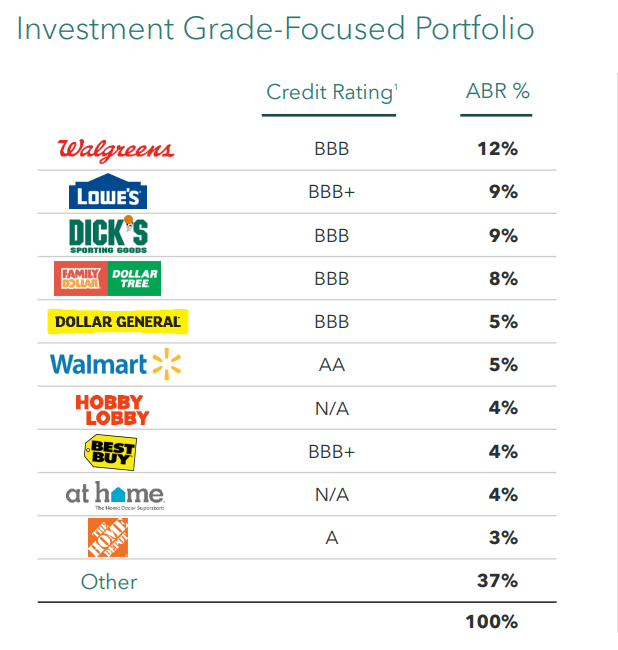

Quality Tenants

PINE’s portfolio consists of 143 properties across 34 states, and a current occupancy rate of 99.5%, according to the latest investor presentation. You probably recognize a lot of their tenants. Some of these highly popular brands consist of Walgreens (WBA), Lowe’s (LOW), Darden Restaurants (DRI) which consist of popular food chains such as Olive Garden and Red Lobster, Dollar, and Verizon (VZ) just to name a few. The lease maturities are well-staggered, with merely 1% of annual base rent expiring this year.

Alpine’s Investor Presentation

Direct competitors in the net lease space such as NNN or dividend community favorite, Realty Income (O),both have exposure to “investment grade” tenants at around 43% – 50% of their total portfolio. Whereas PINE has a total exposure of investment grade tenants of around 63%.

Alpine’s Investor Presentation

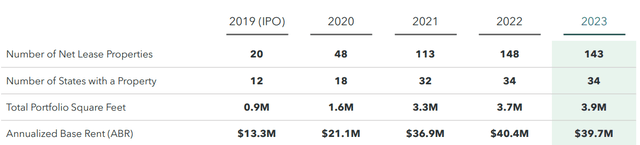

PINE has managed to 7x their number of net lease properties since IPO in 2019 as well as triple the annualized base rent. This is a testament to how well-managed PINE’s portfolio is and how the stock price doesn’t currently reflect the growth in portfolio size. Their tenants are cash flow positive and PINE is set to benefit from this from a sense of stability and increased profitability through rent increases.

Alpine’s Investor Presentation

Market Advantage

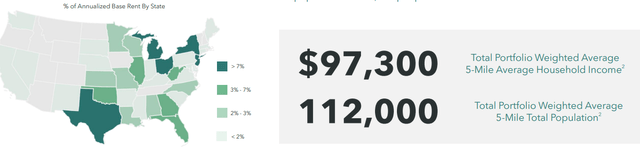

The geographic positioning of PINE’s portfolio is also a stat that I find pretty cool and reassuring; 47% of its annual base rent originates in areas that have a 5-mile radius average household income at $97,500. These are areas of the country that, according to the average, could be classified as high income earning. The average household income currently sits at approximately $88,000. PINE has strategically positioned a large portion of their tenant portfolio in parts of the country where households have a higher level of discretionary income which translates to higher consumer spending. Higher consumer spending means that in theory, PINE can comfortably increase profitability through raised rents.

Alpine’s Investor Presentation

Dividend Growth

PINE currently has a 7% yield and I strongly believe that we will see continuous increases to these payouts.

As stated in the latest earnings call:

For the second quarter of 2023, the company paid a cash dividend of $0.2750 per share, representing a 1.9% year-over-year increase over the company’s Q2 2022 cash dividend, and the current annualized yield of nearly 7%. – Matt Partridge

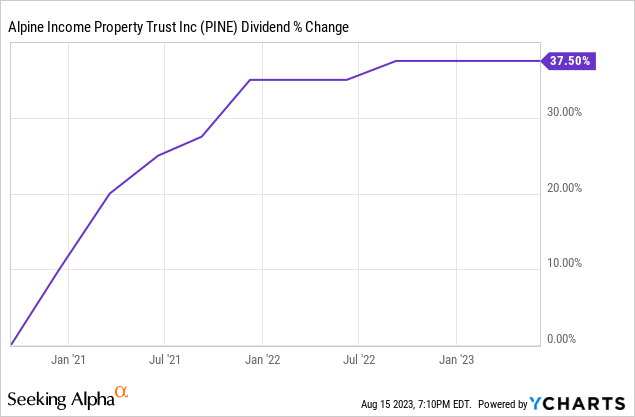

While a 1.9% raise may not be that impressive at first glance, let’s take a deeper look at their trailing history.

We can see that PINE has grown their dividend by 37.5% since the start of 2020. In my opinion, the dividend is strongly supported by a conservative payout ratio of 73% and a strong portfolio of quality, cash flow positive tenants.

The annualized per share cash dividend is $1.10 per share. At the current price of $16.90, this represents a more exact annualized yield of 6.5%.

Valuation

Alpine Income Property Trust has large potential upside that has not been captured by the price movement yet.

Alpine’s Investor Presentation

According to the latest guidance, PINE anticipates that AFFO will range between $1.52 and $1.55 per share, accompanied by net acquisitions totaling $100 – $125 million. This is increased from the prior outlook of $75M – $125M. The increased acquisitions should translate into increased profits which and I believe this a great opportunity for entry.

We can see that the revenue growth since IPO has been amazing, 285% growth since 2019. PINE’s revenue is on the smaller side at the moment but I strongly believe that this is a chance to get in early and ride the momentum upward.

PINE is currently undervalued in comparison to peers, trading at a price of $16.90 with a forward price-to-adjusted-funds from operations (P/AFFO) ratio of 11.4. This is below the sector median of 15 as well as below competitors like Realty Income. The starting yield of PINE also makes this more attractive to investors looking to maximize their cash flow.

Alpine’s Investor Presentation

We can see an average price target of $20.44 per share with a majority of buy ratings. While the price currently sits at $16.90, this represents a potential upside of 17%.

Alpine’s Investor Presentation

Decent upside potential alongside a great dividend growth rate, makes this an attractive entry point to add some solid real estate exposure to your portfolio. PINE’s total enterprise value is $124 per/sq ft compared to their competitor average of $268 per/sq ft. This gives investors the chance to enter below the estimated replacement cost.

Are There Risks?

Roughly 90% of the rent PINE collects is within the retail space. If you aren’t a big fan of the future of retail, then maybe this should be a pass for you. It’s quite understandable after all with the changing landscape of brick and mortar locations and the evolution of ecommerce.

My research shows that the retail sector is doing fine though. There are plenty of retail companies breaking record profits at the moment. According to research by the Wall Street Journal, retail sales have increased for four straight months.

Who knows though? The emergence of unfavorable conditions could significantly impede the market’s ability to command retail space rentals and could throw off PINE’s 99% occupancy rate. For now, I don’t believe this is probable, but I am still considering it as a possibility.

Conclusion

Amid soaring real estate costs, owning property seems unattainable due to limited supply. Property prices might remain elevated. REITs offer an accessible alternative. Alpine Income Property Trust stands out with potential, diversified holdings, and a steady dividend. Its strategic positioning and portfolio growth suggest an undervalued stock poised for profit and yield. Yet, PINE’s reliance on retail rental space bears watching, considering evolving retail dynamics.

Read the full article here