The following analysis and commentary is from the most recent Short Seller’s Journal. In the context of the stock market going “full idiot” right now, Wayfair’s (NYSE:W) share price has levitated to an absurd valuation.

Wayfair (W – $76.88) – W reported its Q2 number on August 3rd before the open. Of course, it reported a “beat.” The stock shot up from the previous day’s close of $72.89 to as high as $90 before closing at $84.67.

It’s a reflection of the degree of insanity that has engulfed the stock market. Despite the “beat,” revenues declined 3.4% YoY from Q2 2022. Revenues have declined for nine consecutive quarters.

The company did manage to cut costs out of its operations. As such, the operating loss declined to $142 million from $377 million. Nevertheless, a $142 million operating loss is not immaterial.

Embedded in the cost of sales and operating expenses is $167 million in equity-based compensation, which is non-cash. Although I think a short squeeze is the primary driver behind the spike up in the stock price, the company likes to look at the “as adjusted” operating income, which adds back the cost of stock compensation.

With W, this results in an operating income of $25 million. But the cost of stock compensation shows up in the form of stock dilution, which spreads the net income over millions of more shares.

The net loss for the quarter was $46 million vs. a loss of $378 million a year ago. However, included in the net income is a $100 million non-cash gain from the extinguishment of debt.

The company issued $678 million in 3.5% coupon convertible bonds and used part of the proceeds ($514mm) to buy back some of its 2024 and 2025 convertible bonds outstanding at a discount to carrying value, which gets booked as non-cash income. The remaining proceeds will be used for working capital and general corporate purposes.

But here’s the catch: W issued a greater amount of cash pay converts at 3.5% and used the money to retire a lesser amount of 1.125% and 0.625% converts, thereby increasing its cash interest expense and increasing the amount of debt outstanding.

I would suggest that part of the motivation/benefit of this transaction, aside from moving $514 million in debt maturities from 2024 and 2025 out to 2028, was GAAP earnings management because the transaction enabled the company to add $100 million to its net income before taxes, albeit non-cash. Net-net, the transaction weakened the balance sheet and it hurts shareholders.

The company attributes the decline in cost of goods sold – which is where W managed to reduce the operating loss YoY – to “operational cost savings initiatives.”

In poring over the breakdown in costs in the footnotes, it looks like most of the savings was carved out of SG&A. Furthermore, a portion of the improvement in gross margin is attributable to sales mix but also lower sales volume.

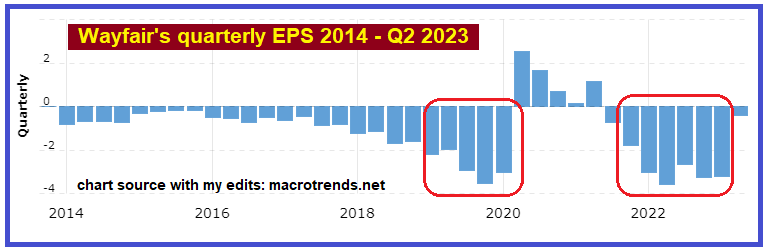

With nine straight quarters of declining revenue, Wayfair’s business is shrinking. And this is before price inflation is removed from the revenues.

In its entire nine-year history as a public company, W has had just five quarters of positive GAAP earnings. This is entirely attributable to the huge jump in revenues during the pandemic period:

W’s net income quickly plunged into big losses once the benefit from the pandemic faded. I think Q2 2023 is an anomaly because Q2 tends to be a seasonally strong quarter for the company.

The business is contracting. I suspect management cut as many costs out of the operations as possible. Unless revenues surge like they did in 2020, I believe W’s losses will revert back to the negativity experienced in 2019 and in the 5 quarters previous to Q2 2023.

The stock price is down 11.4% since the closing price the day it reported Q2. I’ve been riding puts since the day W reported. I am currently sitting on August 25th $74 puts. However, three months ago, the stock was trading at $30. I’m considering putting on a position in the November $55 puts.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Read the full article here