As I write this bit of research while sipping on a cold soda by a warm beach in Nicaragua, I am reminded that not all income is generated in developed countries. Although Nicaragua does not have a strong economy there are other developing countries in Latin America that do have emerging markets that offer strong investment opportunities for savvy investors.

Nicaragua resort – author photo

For example, according to a recent study by Deloitte, Colombia, Ecuador, Brazil, Mexico, Peru, and most recently, Argentina all offer incentives for “digital nomads” to work in their countries, enhancing the local economies in a post-Covid world where tourism is still suffering from the impacts of lockdowns.

The migration office in Argentina estimates that a digital nomad spends US$3,000 per month—twice as much as the average tourist.

In addition, those Latam countries have an opportunity to provide exports to replace Russian exports that are constrained by sanctions due to the invasion of Ukraine, with Argentinian gas being one example. Global lithium production is another resource that offers economic advancement opportunities for Latin American countries such as Chile, the world’s 2nd largest producer of Lithium.

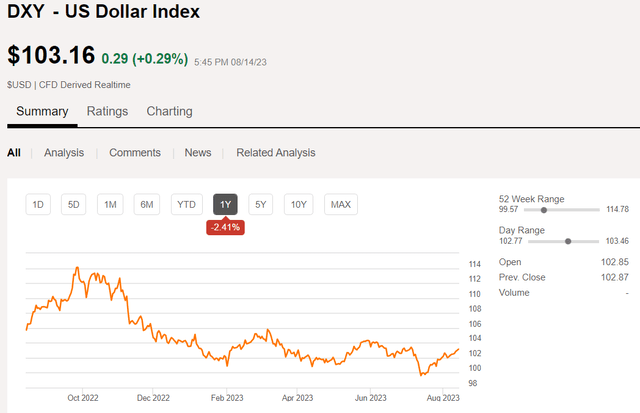

Emerging market economies around the globe offer opportunities for local currencies to perform well against a weakening US dollar. The USD has been showing signs of weakening since October 2022 as illustrated in this chart of DXY – the US Dollar Index.

Seeking Alpha

One fund that I have written about previously that offers investors a steady, high-yield income from investing in emerging market fixed income opportunities is Virtus Stone Harbor Emerging Markets Total Income Fund (NYSE:EDI). For income investors interested in holding a diversified source of income generation that is not dependent on a strong USD, I recommend considering EDI.

Back in February of this year, I rated EDI a Buy due to the positive outlook for EM debt in 2023. I stated at the time that I was cautiously optimistic about the long-term income generation potential for a high yield distribution that appeared to be well covered at the time, and which has continued to pay out a steady monthly distribution of $0.07 per month for more than two years now.

Seeking Alpha

At the current share price of $5.63 as of August 14, 2023, that distribution amounts to about a 15% annual yield paid monthly. The current NAV of the fund is estimated at $5.08 as of 8/11/23 so the current share price represents a premium of about 12%, which is a bit on the high side based on recent history, so I adjust my rating to a Hold at the current price.

Furthermore, since I last wrote about EDI back in February the fund managers proposed a merger with the sibling fund, Virtus Stone Harbor Emerging Markets Income Fund (EDF), which was approved and was initially expected to be completed by August 4. However, that merger has been temporarily delayed due to regulatory approval issues, so the two funds remain separately managed.

The fund also announced that its proposed reorganization with and into Virtus Stone Harbor Emerging Markets Income Fund (NYSE: EDF), which was scheduled to occur on or about August 4, 2023 subject to certain closing conditions, will be delayed pending regulatory approval related to the transfer or sale of certain foreign assets. An update on the timing of the reorganization will be provided at a later date.

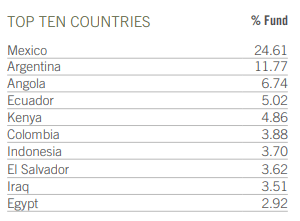

EDI Fund Facts

According to the EDI Fund fact sheet, about 50% of the fund holdings are based in Latin America, with about 28% in Africa, 9% in Asia, and the remainder in the Middle East and Europe. Top 10 countries represented are shown as of 6/30/23.

EDI fact sheet

Approximately 60% of fund assets are in Sovereign Hard Currency, 29% in Corporate Hard Currency, and 10% in Sovereign Local Currency. The ratings distribution includes about a quarter in investment grade fixed income with the remainder in junk-rated or unrated. The fund holds total net assets of $52 million as of 7/31/23 with leverage in the form of reverse repurchase agreements of 17.5%.

Conclusion

While EDI now trades at a premium of about 12% and yields 15%, the sibling fund EDF, which is expected to be the remaining fund post-merger whenever it gets completed also yields about 15% and trades at about a 12% premium. The most recent distribution from EDI indicated that 100% was ROC while EDF included mostly Income and only a small percentage of ROC in its latest distribution. My recommendation at this time would be to swap out of EDI and into EDF if you are inclined to hold long-term. There is no way to know at this point how long it will take for the merger to be completed but the writing is on the wall that EDI will be going away and EDF will remain.

The USD is gaining strength in recent weeks against foreign currencies but the longer term trend is for a weakening dollar as emerging markets gain momentum. In my opinion, it is probably wise to hold some percentage of an income portfolio in EM fixed income whether that is 5% or 10% of the total. In my case, I hold a position of less than 5% in EDI and I will most likely swap it for EDF in the next day or two based on my research for this article. Prior to this week I had expected the merger to close and believed that my EDI shares would just become EDF shares but it looks like that will not happen now unless I make it happen.

I still like EM debt as an asset class, and I still believe that EDI/EDF is a good way to hold that asset class in my income portfolio. I am unclear about the impact of regulatory hurdles preventing the completion of the merger, but I do not want to wait around for my EDI shares to lose value in the event that something derails the merger from happening. If any readers have additional information to share, please add your comments below.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here