All figures are in $CAD unless otherwise noted

All financial data comes from Capital IQ unless otherwise noted

Price Target: $8.25

Investment Thesis

Driven by a fear of a dividend cut, a highly leveraged balance sheet, and an FFO payout ratio greater than 100% Northwest Healthcare (TSX:NWH.UN:CA) has seen its share price decrease by approximately 40% over the past year. The depression of share price has been warranted, but I believe that Northwest has entered an oversold territory. Investors who have a long-term investment horizon, stomach the risks of higher debt, interest rates, and a potential dividend cut are poised to benefit from Northwest’s sound real estate portfolio.

Introduction

Northwest is one of the largest healthcare REITs in the world. Operating out of Canada with 231 properties around the world, Northwest operates in 3 distinct regions as seen below:

- The Americas (Canada, USA, Brazil)

- 90 Properties & AUM of $2.8 billion

- 93% Occupancy & 9.3 WALE

- 6.2% Weighted Average Implied Cap Rate

- Europe (Germany, Netherlands, United Kingdom)

- 69 Properties & AUM of $2.1 billion

- 97% Occupancy & 15.2 WALE

- 5.4% Weighted Average Implied Cap Rate

- Asia-Pacific (Australia, New Zealand)

- 74 Properties & AUM of $5.6 billion

- 99% Occupancy & 16.1 WALE

- 5% Weighted Average Implied Cap Rate

Their asset classes can be broken into 3 defined groups. The first asset class is Hospitals and Healthcare Facilities (61%), followed by Medical Office Buildings (37%), and Life Sciences, Research, and Education (2%).

As at June 30, 2023, Northwest has a portfolio occupancy of 96%, a weighted average lease expiry of 13.5 years, and contracts secured by government-like entities. They also have a significant relationship with a privately owned real estate operating company called Northwest Value Partners. NWVP owns approximately 8.3% of the REIT and their operations consist of real estate ownership and management.

Asset Selloffs

Management is aware of the weakness in their share price and the factors driving the decrease. Northwest has a $340 million non-core asset sale program going on which I view as favorable for the company.

In an effort to reduce their debt, they entered into an agreement with an institutional investor to sell 14 UK hospitals for approximately $276 million. Two other non-core asset sales combined with the UK portfolio sale would have generated approximately $300 million. Proceeds were intended to be used to repay debt with an average interest rate of 8.2% and would have resulted in leverage decreasing from 57.6% to 53.1%. 2 weeks after the announcement, the institutional investor backed out of the deal leaving Northwest in the same predicament as before.

Given that the REIT operates a portfolio of high occupancy properties, they aren’t in a rush to fire sale their properties. I view this as positive even with the current share price issues. As higher interest rates have driven up cap rates, the current investment market for these properties isn’t commanding the price or interest that would compel Northwest to sell these properties. The debt issues while evident, should not be addressed through a fire sale because these properties are still high-value income generating properties.

Management has also addressed rising interest rates by focusing its efforts on reducing the weighted average interest rate and the proportion of debt that is at fixed rates. 66% of their mortgages and loan payables are now at a weighted average fixed interest rate of 3.38% compared to 65% at 4.18% in the first quarter of 2023.

Subsequent events after Q2 2023 include:

- Sale of approximately $54.8 million of its investment in unlisted securities from an Australian fund.

- Refinanced $70 million of variable debt at 6.35% set to mature in September 2023, down to 5.95%, and extended the term by 4 years.

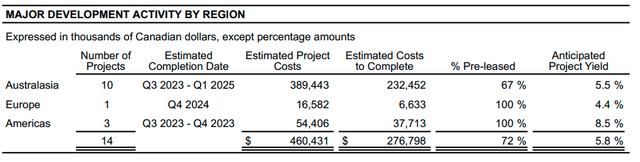

Development Activity

Northwest has 14 major developments with expected completions ranging from Q3 2023 to Q1 2025. The expected project yield for these developments is 5.8% and 72% of the developments are already pre-leased.

Major Development Projects (NWH Q2 2023 MD&A)

Financial Statement Analysis & Dividend Safety

For the first half of 2023, revenues increased by $45 million driven by acquisitions completed in the prior period and rent increases from inflation-indexed properties. Property operating costs increased by $17.5 million driven by the same factors as the increases in revenue.

Losses in their equity-accounted investments ballooned to $21.9 million mainly due to valuation changes for the properties. I view these as temporary headwinds as the equity-accounted investments are still generating NOI and the decreases in fair value are driven by an increase in interest rates.

The mortgage and loan interest rate expense increased by ~$51 million over the first 6 months of 2023 compared to 2022 as a result of rising interest rates. This is the biggest headwind for Northwest Healthcare as the interest expense nearly doubled in the first half of the year. I believe that with the pending asset sales and management awareness of higher leverage, there will be a significant reduction in acquisition and development going forward. During that time, I believe they will focus on managing and paying down high-interest debt.

One key catalyst for Northwest is that they have inflation-indexed rent in place for 82.5% of their properties. Same property NOI has increased by 4.4% in the first half of 2023 and 5.1% in Q2 of 2023. This mechanism effectively shields Northwest and ensures NOI growth. Most REITs don’t have the same safety in growth as Northwest for this reason. The portfolio occupancy also supports this as the demand for healthcare doesn’t face the same market-driving factors as retail, industrial, or office properties.

FFO (AFFO per unit in brackets) has decreased to $0.29 ($0.30) per share in the first 6 months of 2023 down from $0.40 ($0.40) in the same period of 2022. The REIT has declared $0.40 in dividends making their current 2023 AFFO payout ratio 138%. Management targets an 80-95% AFFO payout ratio and therefore, the current dividend is well above their target.

While a dividend cut seems somewhat likely, I believe that the increased AFFO payout ratio is temporary. If management can sell off assets at a reasonable price, it will give them liquidity and the ability to pay down debt. A reduction in debt leading to a lower interest expense would significantly enhance Northwest’s ability to pay its dividend on a consistent basis. Even with a dividend cut, the current dividend yield is at 11.11% which if cut in half would be ~5%. That yield is very competitive and it would provide Northwest more flexibility on their growth initiatives.

I believe the current debt-to-gross book value of 50.8% while high is not a major cause for concern. The rate has increased every quarter since Q4 2021. If interest rates have peaked, or are close to peaking, I would expect this rate to fall. Positively, The current weighted average interest rate of 4.88% decreased compared to the first quarter at 5.15% showing Northwest may be set up for a huge rebound if this trend continues. Northwest carries a 1.92x adjusted EBITDA interest coverage which is much lower than last year however, it’s still within a reasonable range.

Trading Multiples

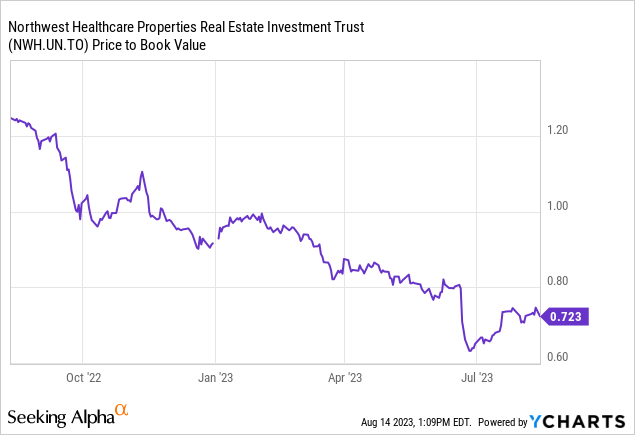

One key valuation multiple used to value REITs is the P/B multiple. Northwest is now trading at a P/B of 0.72x which is very low for a healthcare REIT. In 2022, the average P/B was 1.16x.

If Northwest is able to successfully reduce their leverage and/or interest rates begin to fall, I would expect the P/B to return to their 2022 levels. If priced at a 1.1x P/B, Northwest would be valued at $13.81 (98% upside) based on their current NAV per unit.

For an investor who can stick out the short-term volatility and potential dividend cut, I believe they will be compensated in the long run as Northwest’s operations are secured by credit-worthy tenants, long-term contracts, and a strong management team.

Conclusion

Northwest faces challenges in the near term however I believe these challenges have been overstated by investors. The predictable nature of healthcare, inflation-indexed leases, and the potential decrease in interest rates make Northwest an excellent investor looking to capitalize on the beat up Canadian real estate market. If you can stomach the risks of a dividend cut, I believe that Northwest will figure out the short-term issues and revert back to driving growth within its portfolio.

Disclaimer

This article should not be considered investment advice. Investors and potential investors should consult a professional and/or do their own due diligence before placing trades.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here