In a market where the majority of trading volume is driven by ETFs, the way in which a company is labeled can drastically affect its market price. Those which get labeled favorably trade at a premium to fair value and those which are labeled as an out of favor category are sold to oblivion. There exists a significant opportunity in taking the other end of this trade. We can buy those which have been dashed against the rocks by a cursed label and sell those which have become overvalued due to a simple categorization as something the ETFs and other automated trading picks up.

This article will show active traders can fight back and take advantage of the algos.

Allow me to demonstrate the extreme variance in trading multiples among companies with similar properties simply because the companies have been labeled differently. Specifically, I want to point out mispricing in the following categories:

- The diversified exclusion

- Out of favor labels

- In-favor labels

- Miscategorized companies trading like the bucket they are placed in rather than their actual property type

The diversified exclusion

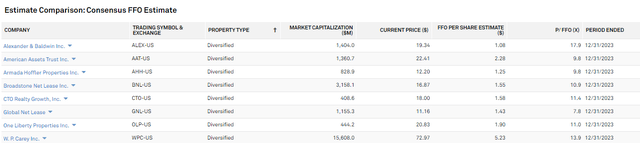

REITs that have been categorized as “diversified” are among the most fertile ground for value investing. While the REIT index has a roughly 16X multiple, the diversified REITs trade closer to 11X.

S&P Global Market Intelligence

Many of these companies are high quality with strong growth. So why do they trade so cheaply?

Well, ETFs and other pooled investment vehicles are often thematic in nature. They use a theme to attract investors and raise capital. The latest theme is of course AI, but prior to that there were hundreds of other themes. In the real estate world, the themes investors have been most excited about are industrial, multifamily and at times data centers.

So various CEFs, ETFs and other vehicles will specifically target REITs fitting the hot categories.

Diversified REITs, by their nature do not get targeted because they don’t naturally fit into any specific theme. This has resulted in them being passed over by most passive investment which unfortunately is a majority of investment trading volume. As a result, these diversified REITs trade at substantially lower multiples than the pure-play REITs which get scooped up by the passive investors.

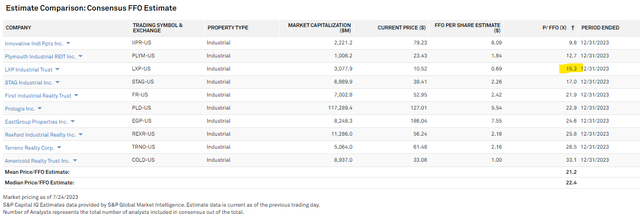

A clear example of this is LXP Industrial Trust (LXP) which used to be a diversified REIT with roughly 60% office and maybe 30% industrial and 10% miscellaneous (golf courses and other oddball investments). About 5 or so years ago LXP started to swiftly sell off its office assets and buy industrial and rebranded itself as an industrial REIT. As soon as that label took hold, its multiple shot up.

It used to trade below 10x and now trades at 15.3X.

S&P Global Market Intelligence

Simply being labeled industrial was enough to buy it inclusion in the thematic investment vehicles. It doesn’t matter to the themes that LXP still has 20 office buildings with over 2.3 million square feet (as of 1Q23). It is the industrial label that garners their attention.

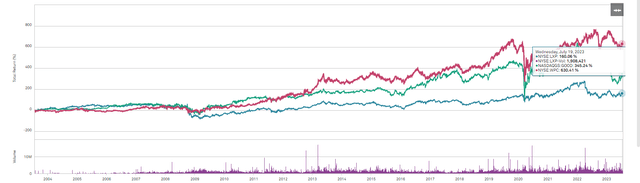

Compare LXP to diversified REIT peers W. P. Carey (WPC) and Gladstone Commercial (GOOD). Much like LXP these are diversified REITs that are mostly industrial.

However, since WPC and GOOD are still labeled as diversified they are not picked up by the thematic based investment vehicles. As a result, they trade at 13.9X and 9.8X FFO, respectively. Noteworthy here is that these are both much better companies than LXP.

Here is the 20 year track record.

S&P Global Market Intelligence

- WPC returned 630%

- GOOD returned 345%

- LXP returned 160%

And that is with LXP’s multiple shooting up after it became a “pure-play” industrial REIT. On a multiple expansion neutral basis, the outperformance of WPC and GOOD was even greater.

This is merely one example, but this pattern of trading is ubiquitous.

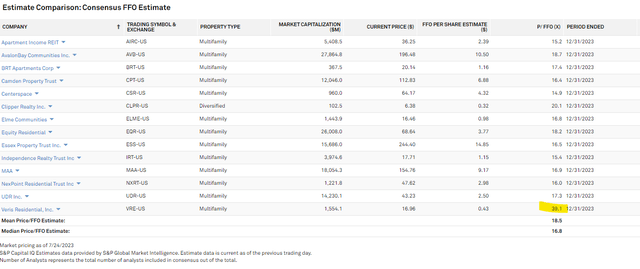

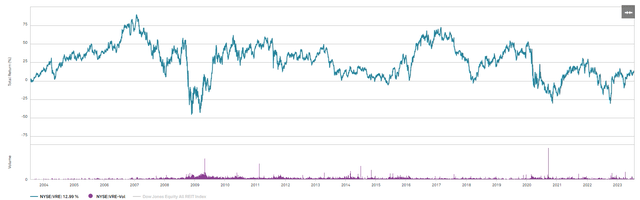

Veris Residential (VRE) used to be a diversified REIT but as soon as it got the pure-play multifamily label its multiple shot up and now sits at 39X.

S&P Global Market Intelligence

Much like LXP, its long term returns are terrible with a 20 year return of just 13%.

S&P Global Market Intelligence

When a REIT tries to jump ship and move into the hot sector the result is almost always a huge loss of FFO/share. Thematic investing is functionally the same thing in that it routinely chases the hot sectors AFTER they become hot.

So, how can one take advantage of the thematic and algorithmic trading? Buy the high quality, cheap companies that are being left out of consideration due to something as silly as a label.

Not all labels are created equal

While having a pure-play label puts a company up for consideration of the ETFs and passive themes, it is only of benefit if the label is one of the desired labels.

Just as investors tend to buy entire groups of stocks, they also sell entire groups of stocks.

A good label will get a company a few extra turns higher multiple while a bad label can cause a stock to trade at a bottom of the barrel multiple.

Here are the in-favor labels:

- Multifamily

- Industrial

- Self-storage

- Data-center

Then there are the labels that are more neutral

- Retail

- Healthcare

- Timber

- Land

- Specialty

Finally, the labels which cause investors to run for the hills with the slightest hint

To a large extent the ranking order is fundamentally justified.

An industrial REIT should trade at a substantially higher multiple than an office REIT. The differences in property quality among the property types are very real.

The mispricing happens when the market looks at how a company is labeled rather than what its properties actually are. Here is a clearcut example.

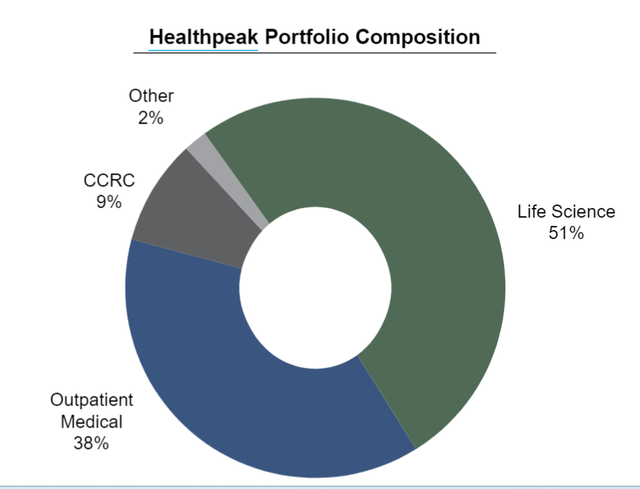

Healthpeak (PEAK) is about 50% research labs, 40% outpatient and 10% CCRC. It is labeled as a healthcare REIT – a neutral label.

PEAK

The outpatient facilities are an okay property type, but it tends to just be a stable source of income with somewhat low growth.

It is the life science that is the pride and joy of Healthpeak.

Listen to any Healthpeak conference call and it will be abundantly clear that research labs are by far their preferred property type. It is the source of their growth and the property type emphasized in every presentation.

It should be. Demand for lab space is high and growing

PEAK’s FFO multiple is 12.5X which looks about right to me. In general life science should trade around 16X while their other medical properties should be closer to 12X. A straight composite multiple would be slightly above PEAK’s 12.5X, but they are having some churn issues at the moment so I think trading at the lower end of the range makes sense.

Getting back to the theme of the article which is mispricing based on labels, compare PEAK to ARE.

Alexandria (ARE) is nearly 100% research labs making it a pure-play of PEAK’s best properties. However, ARE is labeled as an office REIT which knocks its multiple all the way down to 13X.

Not only is ARE entirely in the growth asset class, but they have the most premium assets of the group with a concentration of fully kitted properties in research hubs like Cambridge.

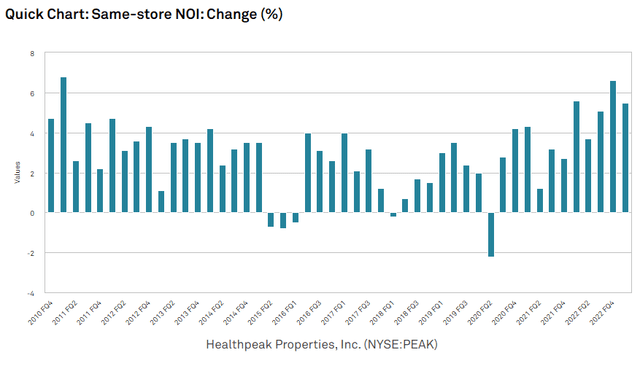

PEAK has had okay growth with a couple negative quarters but usually in the 2% to 4% range.

S&P Global Market Intelligence

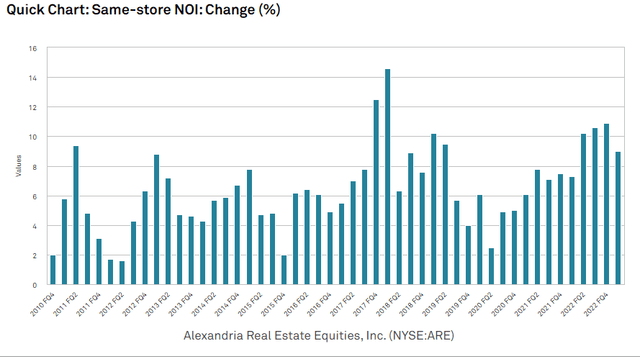

In contrast, ARE averages closer to 6% growth with no negative quarters and the most recent periods accelerating to around 8% organic growth.

S&P Global Market Intelligence

Given the differences in property quality and organic growth rates, I don’t think these companies should be trading at the same multiple.

It is just another example of how the combination of labels and thematic investing (in this case fear of office) can cause rampant mispricing.

As much as I am troubled by the paucity of active investors in the market, the increased passive share has now become the main source of opportunity. Watch for the mistakes caused by misguided themes and capture the mispriced shares.

Read the full article here