Last week, shares of zinc-based energy storage solutions provider Eos Energy Enterprises, Inc. or “Eos Energy” (NASDAQ:EOSE, EOSEW) got hit by a report from shortseller outfit Iceberg Research questioning the validity of the company’s stated $535.1 million backlog:

Iceberg Research

After selling off by up to 65% on massive volume shortly after the report was published, shares recovered over the course of Thursday’s session and finished the day with a much more moderate 24% loss.

Shares dropped another 15% on Friday after Eos Energy reported weak preliminary Q2 results and issued a lukewarm rebuttal of Iceberg Research’s key allegations:

(…) The report also referred to legal proceedings involving multiple Bridgelink legal entities. The Company believes that its customer, Bridgelink Commodities, LLC, is a separate legal entity which is not implicated in the legal matters highlighted in today’s statements. This customer, representing 45% of the Company’s backlog, reconfirmed today that it continues to build pipeline and is actively seeking financing for energy storage projects covered by Eos’s multi-year Master Supply Agreement. (…)

Adding insult to injury, the company warned of approval for a much-touted Department of Energy (“DoE”) Title XVII loan guarantee potentially taking longer than expected “due to changes from the recent Interim Final Rule announced in May“.

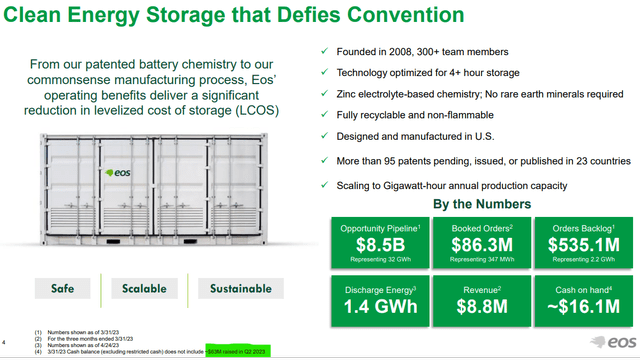

But that’s not all. Eos Energy only booked a paltry $0.6 million in new orders for the entire quarter (following $86.3 million in Q1) and cash and cash equivalents at the end of Q2 were just $23.2 million despite at least $63 million in capital having been raised during the quarter according to the company’s June presentation:

Company Presentation

Consequently, Q2 cash usage calculates to at least $56 million, an almost 70% sequential increase.

At the current pace of cash burn, Eos Energy will have to raise additional capital next month to avoid running out of funds.

At least, the company’s manufacturing transition to its new Z3 battery product appears to remain on track for now:

The Eos Z3 transition is fully underway, and the first semi-automated battery manufacturing line is installed and ready to start commercial production. Eos Z3 batteries utilize the same chemistry, which has over 3 million cycles, that incorporates a new mechanical design aimed at improving performance, lowering cost and increasing manufacturability. The Company expects to deliver its first customer orders from this line in the third quarter. Eos’s progression to the Z3 battery incorporates valuable lessons learned from the past 15 years into a new system design which the Company expects to result in efficiencies as it develops its new state-of-the-art manufacturing line

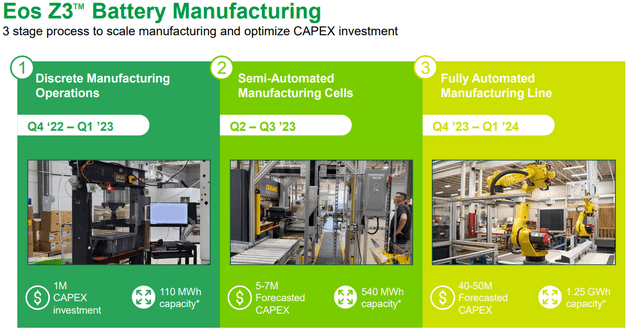

Please note that semi-automated production won’t be sufficient for Eos Energy to achieve positive gross margins, thus the company’s plan to move to fully-automated manufacturing by Q4:

Company Presentation

Unfortunately, up to $50 million in capital expenditures will be required for the final step to fully-automated battery production. Even when assuming some of the recently raised funds having been utilized for ordering long lead time automation equipment, Eos Energy will likely have to raise additional funds to complete the line.

While many investors are still hoping for the company to secure a massive DoE loan guarantee in the very near future, management has been much more cautious regarding the potential amount on the most recent conference call:

We feel positive about where we’re at. Unfortunately, the size of the organization we’re dealing with this process is taking longer than we would like. The overall size of the loan hasn’t changed from what we’ve said previously to 50 plus. And we’re optimistic that we’ll have something to announce in the near future.

Even when assuming the DoE dismisses Iceberg Research’s allegations and provide a generous $100 million loan guarantee, these funds would only be sufficient to cover a maximum of three-quarters of cash burn.

In sum, there appear to be considerable uncertainties with regard to Eos Energy’s order backlog and ability to satisfy its near-term funding requirements.

That said, at least Eos Energy’s CEO appears to have some confidence as he used the sell-off to acquire 31,199 shares in the open market at an average price of $2.23.

But given the underwhelming size, this insider purchase might predominantly serve the purpose of putting a temporary floor under the stock price as Eos Energy will likely have to raise additional capital very soon.

Bottom Line

Following a lukewarm response to new shortseller allegations, weak preliminary Q2 results, and a potential delay to the eagerly-awaited Department of Energy loan guarantee, Eos Energy Enterprises’ common shares ended the week on a poor note.

Based on the calculated Q2 burn rate and the company’s remaining cash balance at quarter-end, the company will likely have to raise additional capital as soon as next month.

Given the very high likelihood of sizeable, near-term dilution, investors should avoid the shares for the time being.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here