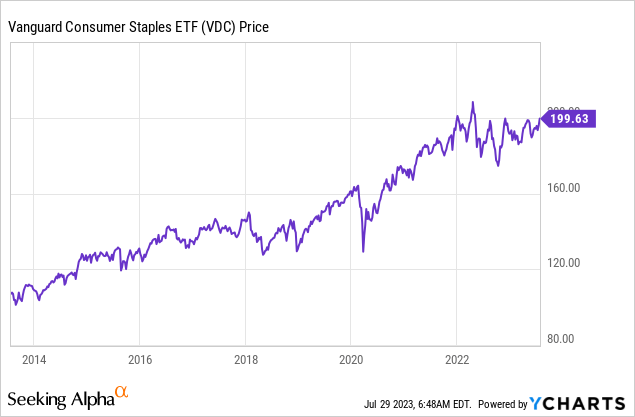

The Vanguard Consumer Staples Index Fund ETF Shares (NYSEARCA:VDC) is a relatively cost-efficient fund (a 0.10% expense fee) that has a strong long-term performance track-record (see chart below) and has a relatively defensively positioned portfolio in an arguably expensive market. That being the case, the VDC ETF is a perfect “SWAN” fund for Nervous Nellie’s that want to sleep well at night. The VDC ETF is overweight such consumer stalwarts as Procter & Gamble (PG), Coca-Cola (KO), Walmart (WMT), and Mondelez (MDLZ) – just to name a few. In my opinion, investors desiring to build a well-diversified portfolio should allocate some capital to the consumer staples sector in order to help buoy their portfolios during times of market stress and to earn a bit of income on the side (VDC currently yields 2.33%).

Investment Thesis

Consumer staples are considered to be a “defensive” sector that will generally hold up better than other sectors in times of market turbulence for a number of reasons. First, these companies typically make products that have resilient demand despite weak macro-economic conditions: shampoo, toothpaste, dish-washing & laundry detergent, paper towels, diapers, etc. Secondly, during inflationary times consumer staples companies can typically raise prices in order to pass-through increased costs directly to consumers.

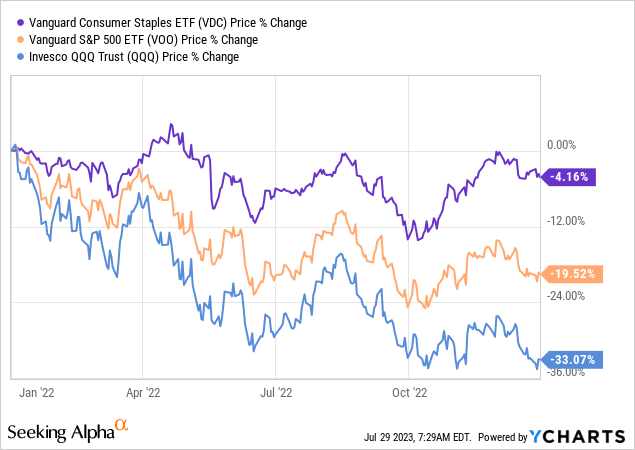

And this is exactly what we saw in the 2022 bear-market:

As can be seen in the graphic above, the Vanguard Consumer Staples ETF outperformed the Vanguard S&P 500 ETF (VOO) by 15%+ last year while trouncing the tech-heavy Invesco Nasdaq-100 Trust (QQQ) by almost 29%

That being the case, let’s take a closer look at the VDC ETF to see how it has positioned investors for success going forward.

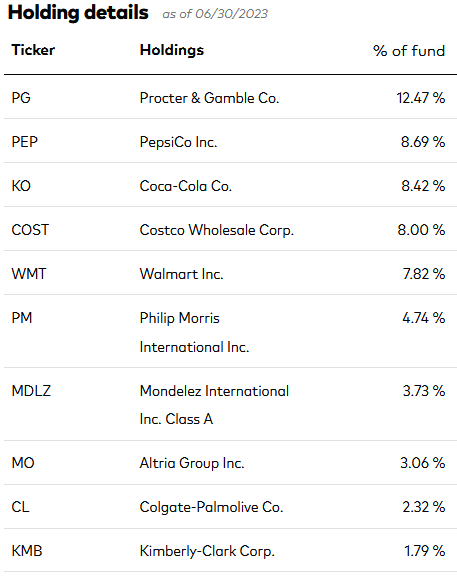

Top-10 Holdings

The top-10 holdings in the VDC ETF are shown below and were taken directly from the Vanguard VDC ETF webpage where investors can learn more detailed information about the fund:

Vanguard

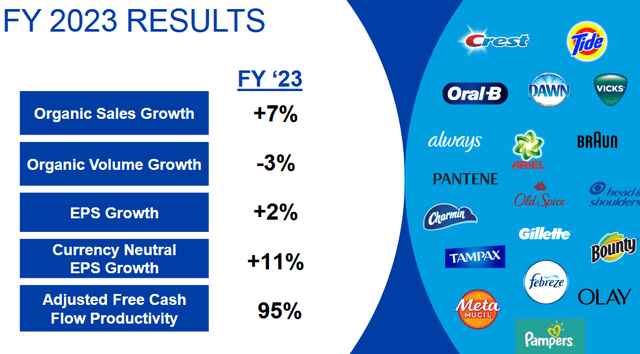

Procter & Gamble is the #1 holding in the VDC ETF with a 12.5% weight. P&G is a perfect example of a company that was able to increase pricing in order to protect margin during the recent surge in inflation. P&G announced Q4 FY23 earnings last week, and it was a strong report. Q3 non-GAAP EPS of $1.37 beat consensus estimates by $0.05, while revenue of $20.6 billion (+5.5% yoy) beat by $610 million. For the quarter, adjusted free-cash-flow was $4.6 billion and – as the slide from the Q4 presentation below shows – rounded out a relatively strong FY23 for P&G:

P&G

P&G returned over $16 billion to shareholders in FY2023: $9 billion in dividend payments and $7.4 billion of share repurchases. P&G is a dividend aristocrat – raising the dividend in April 2023 marked the 67th consecutive year that P&G has increased its dividend and the 133rd consecutive year that the company has paid a dividend since its incorporation in 1890.

Soft-drink and snack food companies PepsiCo (PEP) and Coca-Cola are the #2 and #3 holdings and, in aggregate, carry a 17.1% weight in the portfolio.

The #5 holding with a 7.8% weight is Walmart. WMT stock is up 23.2% over the past year and currently trades with a forward P/E=25.5x.

The #8 holding is the remnant of old tobacco giant Phillip Morris – Altria (MO) – with a 3.1% weight. Altria has been an under-performing stock over the past year (+3.4%), but currently yields 8.25%.

Consumer giants Colgate-Palmolive (CL) and Kimberly-Clark (KMB) round out the top-10 holdings with a combined weight of 4.1%. Colgate announced its Q2 earnings on Friday that beat on both the top- and bottom-lines. Revenue came in at $4.82 billion (+7.6% yoy) which beat consensus estimates by $120 million. Despite organic sales growth (5.4%) that came in ahead of expectations, and pricing +11% across the company, CL stock dropped 1.9% on the day, pushing its yield up to 2.5%.

Performance

As mentioned earlier, the VDC ETF has a relatively strong long-term performance track record, with a 10-year average annual return of 9.43% and a 9.62% average annual return since 2004:

Vanguard

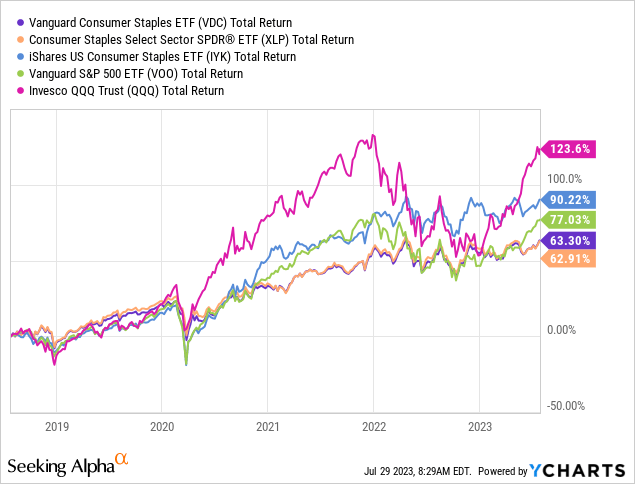

The graphic below compares the 5-year total returns of the VDC ETF as compared to some direct peers – the Consumer Staples Select Sector SPDR Fund ETF (XLP) and the iShares U.S. Consumer Staples ETF (IYK) – as well as the broad market averages as represented by the VOO and QQQ ETFs:

As can be seen in the graphic, not only was the iShares Consumer Staples ETF the best performing ETF in that sector, but it – somewhat surprisingly to me – even outperformed the S&P500 by ~13% over the past 5-years.

Risks

While the VDC portfolio holds relatively defensively stocks, they are still not immune to the macro global economy and could be negatively impacted by high inflation and rising interest rates. In addition, raising prices on brand name products could lead consumers to switch to cheaper off-brand offerings.

The top-10 holdings in the VDC ETF are relatively concentrated (~60% of the portfolio as compared to ~32% for the top-10 S&P500 ETFs). However, that’s really what investors should want because these top-10 companies are arguably the global leaders in the consumer staples sector.

The bigger long-term risks of holding the VDC ETF is under-performing the S&P500 – which has a 10-year average annual return that is roughly 340 basis points higher. Which is why I advise investors to make the S&P500 the cornerstone of their portfolios (as I do) with an allocation substantially higher than individual sector ETFs like VDC.

Summary & Conclusions

Based on its own merits and long-term performance track record, I rate the VDC ETF a BUY. However, I certainly need to acknowledge the outstanding performance of the iShares IYK ETF, which not only has outperformed its Consumer Staples peers over the past 5-years, but also beat the S&P500 over that time frame by a very impressive 13%.

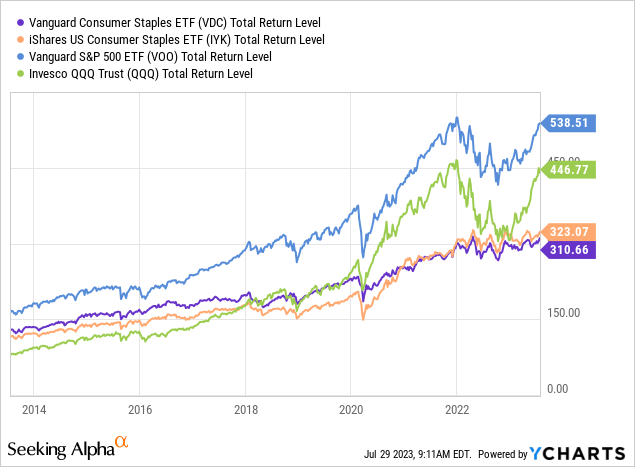

I’ll end with a 10-year total returns comparison of the VDC ETF versus IYK, VOO, and the triple Q’s. This chart proves why long-term oriented investors should allocate a significantly greater proportion of their portfolio to the broad market averages like the S&P500 and Nasdaq-100 as compared to the consumer staples sector.

Read the full article here