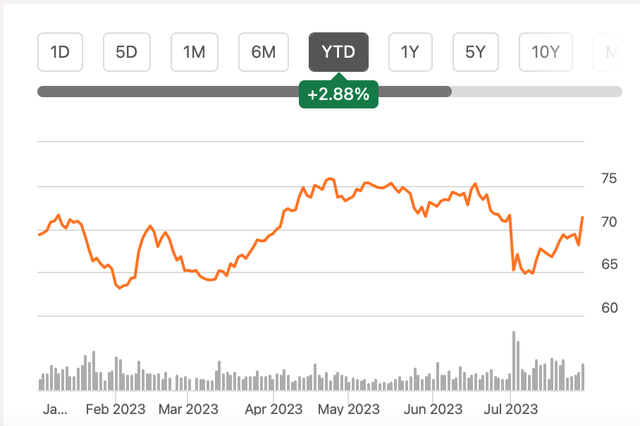

Since the last time I covered the pharmaceuticals giant AstraZeneca (NASDAQ:AZN) (OTCPK:AZNCF) in May this year, its share price is almost back to where it was when I wrote.

Even at the time, there seemed little short-term upside to the stock. In fact, it fell by almost 10% in the interim (see chart below), but after the release of its second quarter (Q2 2023) figures yesterday, it rose by almost 5%. Clearly, investors are happy with the results. Here I look at them in some detail to see why and draw insights into what could be next for the stock.

Price Chart (Source: Seeking Alpha)

Robust results

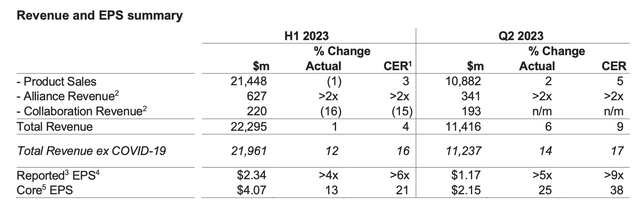

There’s nothing not to like in AstraZeneca’s results. Even if headline revenue figures show small growth (see table below) for the first half (H1 2023), that’s because of the softening in its COVID-19 sales. Revenues ex-COVID-19 medicines have grown by a healthy 12% year-on-year (YoY) at actual exchange rates [AER] and by 16% at constant exchange rates [CER].

Source: AstraZeneca

A massive 41% decline in cost of sales during this time has resulted in an increase in gross profit margin to 82% in H1 2023 from an already high 69.9% in H1 2022, continuing the trend from Q1 2023. This cascades down through to the rest of its profits as well, resulting in an over 4x at AER increase in reported earnings per share [EPS]. Significantly, Core EPS saw double-digit growth of 21% at CER, with an acceleration in Q2 2023. This is a significant improvement from the much smaller 6% growth in core EPS in Q1, 2023.

Oncology leads growth, approvals across markets

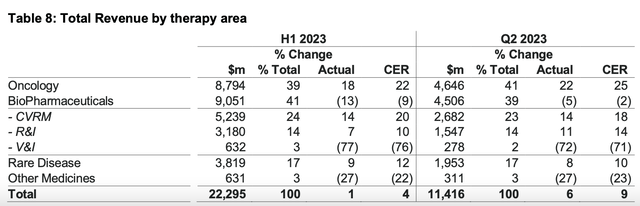

Underpinning the strong performance were double-digit growth rates in segments like oncology and rare diseases (see table below). The company’s blockbuster small lung cancer treatment Tagrisso, which alone accounts for 13% of the company’s H1 2023 revenues, showed double-digit growth.

Revenues across Segments (Source: AstraZeneca)

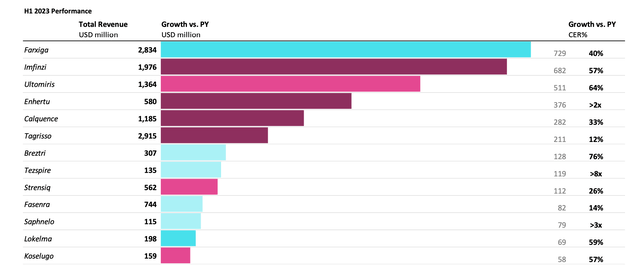

Diabetes medication Farxiga, the next biggest revenue contributor with an almost 13% share, showed even stronger growth of 39% at CER. But the highlight growth among big revenue generators came from the immunotherapy drug Imfinzi, which jumped by 57% at CER. (See chart below for further details).

Source: AstraZeneca

Significantly, Lynparza, the ovarian and prostate cancer treatment received advanced regulatory approvals in the US, which is its biggest market with a share of over 42% in revenue. The treatment is already a 6% contributor to the company’s revenues.

Further, the rare disease medication Ultomiris, which also accounts for 6% of the revenues and already showed 64% CER growth in H1 2023, has received EU approval for use in certain nerve diseases. China, too, has approved its treatments for a range of disorders.

Acquisition from Pfizer

It also bears pointing out that along with the results released yesterday, AstraZeneca also revealed that through Alexion, the rare diseases specialist it acquired in 2021, it has now purchased Pfizer’s (PFE) rare diseases gene therapy portfolio.

The USD 1 billion deal, which is expected to close in Q3 2023, follows Pfizer’s pullback from early-stage rare disease R&D. It now adds to AstraZeneca’s promising existing portfolio of rare diseases, which added over USD 7 billion or 16% of the total revenues in 2022.

Guidance indicates slowing down in H2 2023

Coming to the company’s outlook, positive as the latest numbers are, the guidance in CER terms reflects some cooling off in growth in H2 2023. Ex-COVID-19 revenue is expected to rise by “a low double-digit percentage”, compared to the 16% rise seen so far. However, it doesn’t sound material enough softening to be any cause for alarm.

However, it does expect Core EPS growth to slow down significantly to a “high single-digit to low double-digit percentage” from the 21% rise seen so far. Besides the effect of some come-off in revenue growth, a possible increase in the Core tax rate, expected to range between 18-22%, from 18% in the first half.

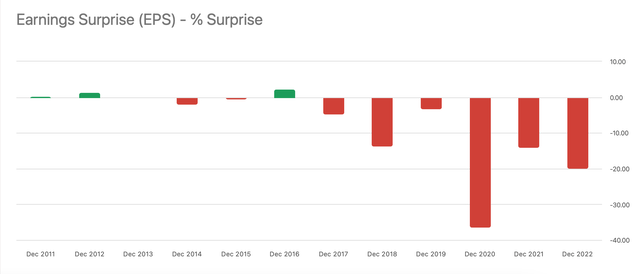

Analysts’ estimates are also in line with AstraZeneca’s guidance, with an expectation on average of a 9.6% EPS increase. It’s worth noting, though, that financially healthy as the company is, for nine of the past 10 years, its earnings have surprised on the downside (see chart below). Also, expectations of EPS growth have reduced from the 11% they were at the last I checked.

Source: Seeking Alpha

Market valuations and dividends

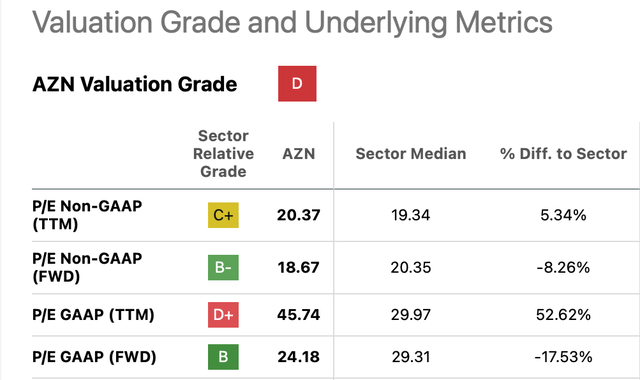

The current estimates give a forward non-GAAP price-to-earnings (P/E) ratio of 18.7x, which is slightly lower than the 20.3x for the Health Care sector and AZN’s own five-year average ratio of 19.5x. This difference isn’t big enough to justify a significant price rise, though. This is further reinforced by the fact that it has a tendency to underperform compared to analysts’ projections. Further, its trailing twelve months [TTM] non-GAAP P/E is also slightly elevated (see table below).

Source: Seeking Alpha

However, its market multiples look much better when we get into the next couple of years too, which is something to consider for medium-term investors. For 2025, analysts’ estimates show a forward P/E of 14.2x, which is quite a bit below its average. This indicates a 37% upside to the stock by late 2025 or early 2026.

For long-term investors, though, I’d like to point out its dividends. AstraZeneca’s TTM dividend yield isn’t terribly high at 2.1%. Its forward yield does get better at 2.9% however. And both TTM and forward yields are higher than 1.4% and 1.5% respectively, for the sector.

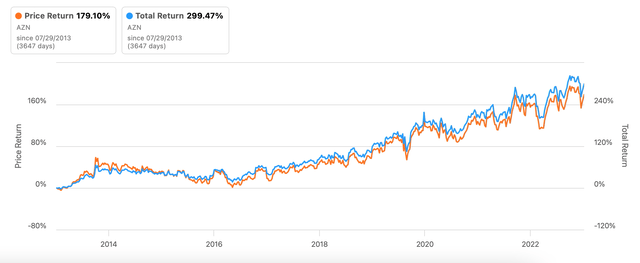

The real juice, however, is in how much dividends add up to returns over time. In the last ten years, just AZN’s price returns have been a solid 179%. But add dividends to the mix, and the total returns increase to almost 300%. In other words, the humble yield hides significant returns on its own over the long term.

Source: Seeking Alpha

What next?

So from a long-term perspective, AstraZeneca remains as good a buy right now as it ever was, especially for investors looking for a passive income. Its latest results continue to reflect its strong sales and good earnings growth. The company also continues to gain approvals for treatments across markets. And if it’s able to make the acquisition of Pfizer’s rare diseases gene therapy portfolio work as well as the Alexion acquisition, its numbers can continue to benefit.

However, for investors looking more for price gains right now, I think there could be better opportunities to buy the stock over the rest of the year as it’s fairly valued right now. Essentially, the story continues from the last time I wrote about it.

With the short-term and long-term pulling in opposite directions, let’s consider the medium-term, too. The arguments for its long-term hold here too, and the forward multiples look much better. With both the medium and long-term stories intact, I’m retaining a Buy on AstraZeneca.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here