Walt

Disney’s

films and theme parks have captured the hearts of millions, but its stock performance has been less than enchanting. Once a favorite of growth investors, shares have tumbled nearly 60% from their peak in 2021. With CEO Robert Iger ready to make some tough choices as he works to return the House of Mouse to its former glory, a path higher for the beaten-down shares is coming into view.

If this were a fairy tale, Disney (ticker: DIS) could be compared with the kingdom in Sleeping Beauty: dormant, overrun with vines, and waiting for a hero to restore it to life. Perhaps Florida Gov. Ron DeSantis, who has chosen to make an example of Disney for its opposition to a state law passed under his administration, would be cast as the wicked witch, and a recent box-office slump could be blamed on a nefarious spell that had fallen over the land.

But this is the real world, and in the real world, Disney has been plagued by its own missteps. It is spending big on streaming, where profits remain elusive, while cable revenue continues to deteriorate. Its recent films, like Elemental and Indiana Jones and the Dial of Destiny, fell short of the mark set by Barbie, Oppenheimer, and even The Super Mario Bros. Movie. To repair the damage, Iger, who had stepped down in 2020, returned as CEO, taking over from Robert Chapek.

Iger is no Prince Charming, but he has made clear that this is a whole new world for the media titan. With his contract extended for two years, until 2026, Iger has time to implement his vision for the company, one that centers on two pillars: streaming and theme parks. Everything else, including Disney’s cable channels, could be on the table for a possible sale. Disney is also taking steps to ensure that its earnings return to a more sustainable path. Costs have been cut, shows canceled, and a course forward—one that focuses on what Disney does well and profitably—charted. Even the dividend, paused in 2020, could return by the end of this year. With its shares appearing cheap relative to its earnings and the sum of its parts, now looks like the right time to bet on the magic returning—at least to Disney’s stock.

| Headquarters | Burbank, Calif. |

|---|---|

| Recent Price | $85.86 |

| 52-Wk Change | -14.0% |

| Market Value (bil) | $158.8 |

| 2024E Sales (bil) | $94.2 |

| 2024E Net Income (bil) | $8.3 |

| 2024E EPS | $5.02 |

| 2024E P/E | 17.1 |

| Dividend | None |

Note: Fiscal year ends in September. E=estimate.

Source: FactSet

“Rome wasn’t built in a day, and Disney’s problems won’t be solved in a year,” explains Wells Fargo analyst Steven Cahall. “Bigger picture is, Disney seems to be taking increasingly bold actions.”

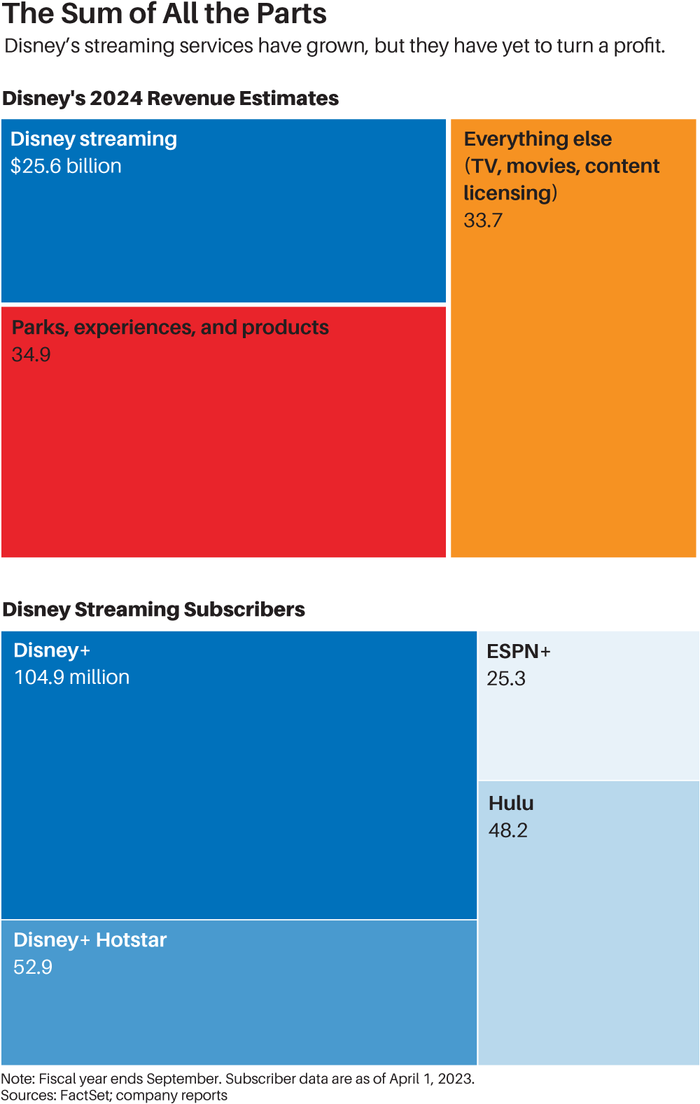

Not that it has much of a choice. For now, the brightest spot in Disney’s portfolio is its theme parks, cruises, and consumer products business. The division, which represented more than a third of revenue last fiscal year, at $28.7 billion, and two-thirds of operating profits, at $7.9 billion, has benefited from pent-up demand for travel and experiences by consumers in the U.S. and abroad, keeping attendance high and giving Disney pricing power at its attractions. Management says that per capita spending at Disney’s parks is more than 40% higher than in 2019, thanks to premium offerings like Genie+ and Lightning Lane. Recent reports suggesting a drop-off in waiting times don’t change that.

“The parks are a really powerful tollbooth on consumer discretionary spending,” says Wolfe Research analyst Peter Supino. “They attract consumers with higher purchasing power, whose spending tends to grow faster than nominal GDP. It’s a really nice structural position.”

The same can’t be said for Disney’s media business. Iger is faced with the thorny problem of balancing its growing, but expensive, streaming segment against its slowing cable business. Disney’s revenue from its linear networks, which include ABC, ESPN, Disney Channel, FX, and National Geographic, was down 4% in the past four reported quarters, to $27.4 billion, as advertising sales slumped and customers cut the cord. The past year’s operating income dropped 11%, to $7.3 billion. Simply put, linear TV is caught in a doom loop: Higher churn and fewer subscribers prompt price increases to make up for lost revenue, increasing the incentive to cancel. Disney declined to comment for this article.

Streaming has yet to take the baton. Disney’s direct-to-consumer segment lost $4.2 billion in the past four reported quarters on revenue of $20.8 billion, which was up 13%. But losses widened 77%, as content costs grew faster than subscription revenue. Disney’s fiscal third-quarter results, which correspond to the calendar second quarter, are due on Aug. 9.

Things should improve as Iger focuses on running the streaming business for profitability, not merely subscriber growth. The company expects to have between 135 million and 165 million Disney+ subscribers outside of India by the end of its fiscal 2024, or September of next year, up from 104.9 million at the beginning of April. (Disney+ Hotstar in India adds another 53 million subscribers, but at an average monthly revenue of only 59 cents, versus $6.47 for core Disney+.) Management expects the streaming segment to reach break-even by the end of that year, though Wall Street isn’t convinced—analysts expect a streaming loss of about $500 million in fiscal 2024.

Still, there’s no denying that Disney remains a must-have for children of all ages, with popular shows like The Mandalorian and movies like Frozen on repeat. Disney plans to raise prices for the advertising-free tier of Disney+, which costs $11 a month in the U.S., $3 more than the ad-supported version, and more hikes are in store abroad. It’s likely most subscribers will simply pay the higher bill.

“Pixar, Marvel, and Star Wars are taxes on parents,” says Christopher Rossbach, chief investment officer at J. Stern & Co. “You have no choice but to subscribe, and that gives Disney pricing power.”

Other big changes are coming that should help Disney meet its numbers. Disney has all but promised to purchase the one-third of Hulu, with its 48 million subscribers, that it doesn’t own from

Comcast

(CMCSA) by early next year, which could come with a price tag of nearly $10 billion. There are benefits of bringing ownership fully in house. Hulu features adult-oriented content that can appeal beyond the more family-friendly Disney+ franchises.

Disney said it plans to allow U.S. users to access Hulu via the Disney+ app if they subscribe to both services—encouraging bundling. And bundling is likely the way forward for Disney—a bundle of Disney+, Hulu, and ESPN+ has just 2% churn, according to MoffettNathanson, far lower than the services individually. The no-ads version of the bundle goes for $20 a month in the U.S.

“In short, one hard Disney bundle that includes content from Hulu, Disney+, and ESPN+ will deliver enough premium content to reduce churn, aggregate engagement, and generate substantial nonprogramming cost savings,” explains MoffettNathanson analyst Michael Nathanson.

In the meantime, the focus will be on controlling costs. Disney plans to decrease non-content-related expenses by $2.5 billion this year by reducing marketing spending, cutting some 7,000 jobs, and finding savings in technology, procurement, and other areas. The company will also reduce spending on content, which was on track to reach $30 billion in 2023, by $3 billion annually. It plans to start with the low-hanging fruit, namely sports rights and high-price shows that don’t drive enough subscribers to justify, such as the recent cancellation of series based on the Mighty Ducks and National Treasure franchises. Disney also walked away from a bidding war for Indian Premier League cricket streaming rights. “We’re getting much more surgical about what it is we make,” Iger said in May.

An unexpected contributor to cost-cutting may be the concurrent strikes by unions representing Hollywood actors and writers. They are pushing for a share of streaming revenue and protections against artificial-intelligence use of their work or likeness—demands that Iger called “not realistic” in an interview with CNBC on July 13. The immediate result is that content production has come to a standstill, though most viewers won’t be able to tell for a while. Long postproduction timelines mean that strikes won’t begin to affect scheduled streaming releases until the winter or early next year. Sports, game shows, and news broadcasts will go on as usual, and international productions can largely proceed uninterrupted.

Needham analyst Laura Martin doesn’t expect meaningful production work to resume before January, even if the strike is resolved before the holiday season. That means studios won’t spend much on new scripted content in the U.S. for the remainder of 2023. She estimates that could translate to an additional $3 billion to $5 billion in free cash flow for Disney, and savings should continue even after the strike ends, Martin argues.

“The primary impact of the writers and actors strike is it will structurally lower content costs at the streaming companies, which is what Wall Street has been demanding,” she says.

In the long term, Disney’s direct-to-consumer business should look more like

Netflix’s

(NFLX), which is about 50% larger in streaming today and boasts an operating profit margin of nearly 20%, compared with Disney’s negative 20% streaming operating margin. “It’s going to be a multiyear path [to Netflix-like margins], and investors are going to need to be patient,” says Jason Ware, chief investment officer at Albion Financial Group. “But the good news is we’re not talking about a long-duration equity that has no earnings, which was the Netflix story. Disney has established businesses with real profits and cash flows. It’s not a speculative company.”

In the shorter term, a slow but steady narrowing of streaming losses and cost cutting will help turn the tide for Disney’s bottom line. Analysts are expecting the company to return to year-over-year earnings-per-share growth in the fiscal fourth quarter, which ends in September, after four straight quarters of negative comparisons. Even the soon-to-be-reported quarter should see Disney notch a profit of $1.00 per share, down 8%—but better than a 14% year-over-year decline three months earlier—as it pushes toward a profit of $3.75 in fiscal 2023. The following year should be even better, with earnings hitting $5.04, up 34%.

Little of the possible good news appears to be reflected in Disney’s stock price. At $85.50, near levels first hit in 2014, shares are trading at 18 times 12-month forward earnings, well below their five-year average of 29 times and below the S&P 500’s 20 times. That’s a large discount to Netflix, which trades at 30.6 times, and only a slight premium to

Paramount Global

(PARA), at 15.6 times, despite better prospects.

Warner Bros. Discovery

(WBD) trades at 196 times. Even an increase to 22 times—three quarters the historical multiple—would put Disney stock at $105, up nearly 25%.

But the real opportunity is evident when looking at the sum of Disney’s parts. In the worst case, shares could be worth $76, using math from Atlantic Equities’ Hamilton Faber, who doesn’t expect streaming to break even until 2026 and applies a 1.5 times revenue multiple to that revenue. He values Disney’s remaining business at 12 times earnings.

That seems too pessimistic. The current price looks close to a floor, even when writing off the entire value of Disney’s linear networks.

Streaming leader Netflix’s enterprise value amounts to 6.2 times expected revenue over the coming year. Applying just half that multiple to Disney’s streaming business gives a value of $74 billion. The company’s theme parks and consumer products segment is probably worth $134 billion, after putting a modest 13.5 multiple on operating income of $9.9 billion.

Adding those together and subtracting Disney’s net debt and minority interests gets to an equity value of about $156 billion, or $86 per share. That’s Disney stock’s current price.

But that ascribes not a penny of value to the company’s linear networks, a shrinking business that will still comfortably earn between $6 billion and $7 billion over the next year. Putting a multiple of seven on that business would give it a market value of about $46 billion, lifting the stock price to $111.

Slightly more aggressive math points to even greater upside. Putting a multiple of 16 on Disney’s parks yields $158 billion, more than the entire market value of the company. That would take the stock to $124. The risk/reward favors buying here.

There’s another potential path for Disney that could deliver a payout for shareholders, while also solving the CEO succession question: Sell the farm and move on. Needham’s Martin thinks that

Apple

(AAPL) should buy Disney to propel its virtual- and augmented-reality ambitions. It would mean exclusively owned content for the Apple Vision Pro headset, and creative possibilities using AR at the theme parks. Apple doesn’t need to make money from content, she notes, instead using it as a lure to sell more high-margin hardware. Disney is already an initial content partner for the Vision Pro, with Iger making an appearance at the unveiling event in June.

“If you believe we’re moving into a world where goggles or headsets are the next computing platform, as Apple and

Meta Platforms

[META] do, then Disney becomes a very interesting target,” Martin says. Disney’s $210 billion enterprise value is 7% of Apple’s market capitalization, or two years of free cash flow. Apple didn’t respond to a request for comment.

Absent a sale, there’s a simple way for Disney to demonstrate to investors a return to financial stability—by reinstating the dividend. Former chief financial officer Christine McCarthy said earlier this year that the company plans to restart its payout by the end of 2023, though it would initially be smaller than what it was when put on hold in spring 2020, when it paid 88 cents a share semiannually. The company certainly has the money to do it, with free cash flow expected to hit $3.6 billion this fiscal year, on its way to $9 billion in fiscal 2025.

“Paying a dividend is important because it shows a focus on free cash flow,” MoffettNathanson’s Nathanson says. “Disney needs to get back to that $8 billion to $10 billion range in a few years’ time for the stock to be supported by cash flow.”

A dividend announcement could happen at an investor summit planned for September, an event that gives management a chance to get the narrative back on track and to potentially offer new targets for future streaming profit margins after reaching break-even. Disney will still need to achieve its goals—but putting them out will help Wall Street see the path to get there. In short, there’s a solid lineup of positive catalysts in the back half of 2023 that could help reignite interest in Disney’s beleaguered stock.

And who knows? Maybe it turns out to be a fairy tale with a happy ending after all.

Write to Nicholas Jasinski at [email protected]

Read the full article here