PacWest Bancorp (NASDAQ:PACW) finally reported much-awaited results for the second quarter after the market closed on Tuesday. Just before the market closed, speculation swirled on rumors that the regional bank was set to merge with regional banking rival Banc of California (BANC), causing shares to plunge by almost 30%. Rumors were later confirmed by both banks, and PacWest Bancorp’s share price fully recovered in the aftermarket. I recommended PacWest Bancorp as a speculative buy ahead of Q2 (due to expected deposit inflows), but given the merger announcement with Banc of California, I am downgrading my rating to hold!

PacWest Bancorp’s Q2’23 earnings report itself, however, was not nearly as bad as feared and the regional bank beat EPS consensus estimates and reported much smaller losses relative to the first quarter. The merger deal is likely a win-win situation for the bank and its shareholders.

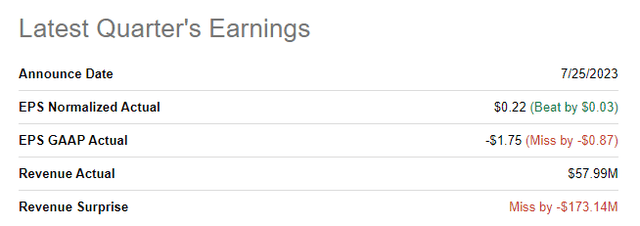

PacWest Bancorp beat EPS estimates

PacWest Bancorp reported revenues of $57.99M, missing revenue estimates. However, earnings were better than expected with the regional lender reporting $0.22 per share in adjusted earnings compared against a prediction of $0.19 per share.

Seeking Alpha

PacWest Bancorp’s Q2 earnings sheet was not bad, deposit base stabilizes

Expectations were not exactly high heading into earnings, and PacWest Bancorp reported overall good results.

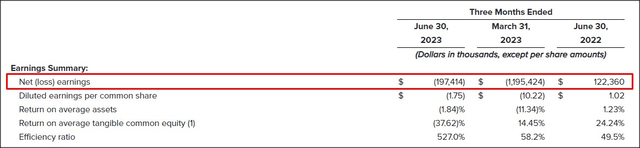

PacWest Bancorp generated a net loss of $197.4M in the second quarter, which was significantly below the Q1’23 loss of $1.2B. The regional bank made a loss and missed expectations largely because it sold a large block of loans, which occurred at a discount to face value, in order to provide relief to PacWest Bancorp at a time of heightened liquidity demands. The bank sold a $2.6B construction loan portfolio as well as a $2.1B Lender Finance portfolio in the second quarter in a bid to strengthen its balance sheet, raise cash and reduce lending risks.

PacWest Bancorp

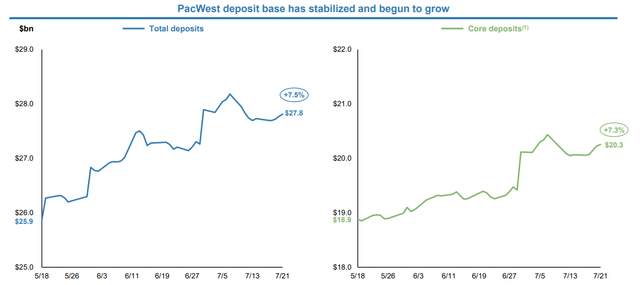

Deposit base is stabilizing as well

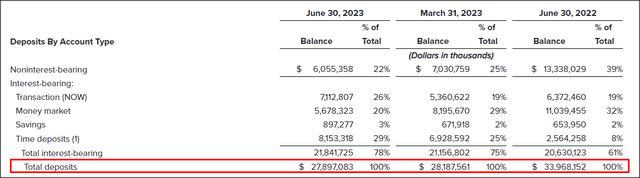

PacWest Bancorp had deposits of $27.9B in the first quarter compared to a deposit base of $28.2B in the second quarter, showing a decline of 1% quarter over quarter.

PacWest Bancorp

While the overall deposit trend was not bad, it was not as positive as I had hoped before the earnings release… which is when I recommended PACW as a speculative buy. Regional banks like Western Alliance Bancorporation (WAL), which was also extremely battered during Q1, saw strong deposit inflows to its franchise throughout Q2’23. Zions Bancorporation (ZION) more than fully restored its deposit base in the second quarter as well.

PacWest Bancorp

PacWest Bancorp’s merger with Banc of California

Shares of PacWest Bancorp dropped almost 30% yesterday at the end of the trading session on rumors that the regional lender could merge with Banc of California. PacWest Bancorp later confirmed those rumors, ironically causing a sharp upward bounce of the bank’s shares in the aftermarket.

The agreed-upon merger terms show that the transaction will be conducted in a 100% stock-for-stock transaction, and PacWest Bancorp shareholders will receive 0.6569 shares of Banc of California for each PacWest share they own. Shares of Banc of California currently trade at $16.21 (pre-market price), meaning the implied value of the merger for PacWest Bancorp’s shareholders, at this point in time, is approximately $10.65 per share, but this value will change, depending on the price of Banc of California’s shares at the time of the closing. The transaction is said to close in late 2023 or early 2024.

Shares of PacWest Bancorp soared 31% in the aftermarket yesterday, indicating that bank management negotiated a solid deal for shareholders, given the circumstances. Private equity firms Warburg Pincus and Centerbridge are set to invest a total of $400M (at a price of $12.30 per share) which calculates to a 20% investment in the merged regional bank: 16% for Warburg Pincus and 4% for Centerbridge. PacWest Bancorp’s shareholders are set to own 47% of the combined new regional lender while Banc of California investors will own 34% of the merged entity.

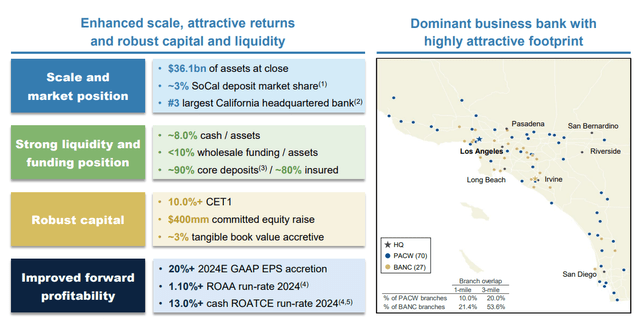

The combined bank will have $36.1B in assets and $30.5B in deposits, and the merger creates the third-largest bank in California. The transaction is expected, according to the merger presentation, to result in 20% EPS accretion in FY 2024 and approximately 3% tangible book value accretion.

PacWest Bancorp

My thoughts on the merger

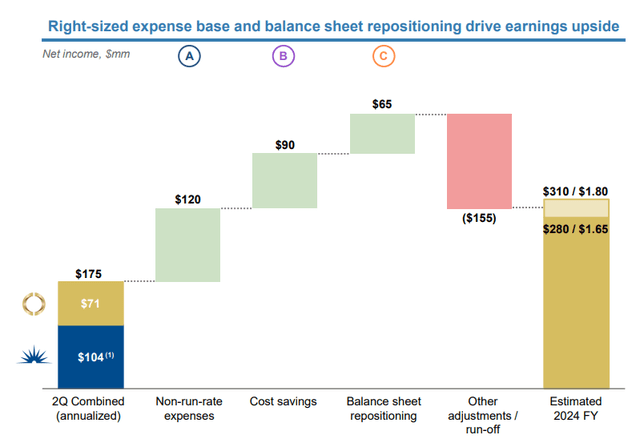

I believe the merger ultimately benefits shareholders of PacWest Bancorp because the bank’s share price has been weighed down by uncertainty and significant negative sentiment overhang after it lost a large chunk of its deposits in Q1. While the bank said that the acquisition will be accretive to tangible book value, PacWest and Banc of California also have an opportunity to optimize their cost structure and generate cost synergies for the benefit of shareholders. According to PacWest Bancorp, the merged company could have $130M in pre-tax cost savings and improve its net interest margin as well.

PacWest Bancorp

Risks with PacWest Bancorp

Due to the fixed exchange ratio and 100% all-stock nature of the deal, the final price PacWest shareholders receive will depend on the price of Banc of California’s shares. Until the transaction closes, I see PacWest Bancorp’s share price move in a price range of $8.50-10.60 (the price range results from the exchange ratio of 0.6569x applied to Banc of California’s pre-announcement share price of $13 and current pre-market price of $16.21).

Banc of California’s share price soared 11% on the merger announcement yesterday, and the higher the share price goes, the more value PacWest Bancorp shareholders will stand to receive as well. On the other hand, a decline in Banc of California’s share price implies a significantly lower deal value for PacWest Bancorp’s shareholders. Therefore, the biggest risk for PACW shareholders relates to the final deal value they will receive.

While the proposed merger has its benefits (and has a good chance, in my opinion, of getting shareholder approval given PACW’s depressed share price), I am downgrading my rating from buy to hold chiefly because PacWest Bancorp did not see it as material deposit inflows in the second quarter as I had hoped. My main reason to invest in PacWest Bancorp in the first place was to play a recovery in the deposit base which, given the merger announcement, is now no longer relevant.

Closing thoughts

PacWest Bancorp’s deposit situation was not as great as I thought it would be, but the regional bank overall submitted a very decent Q2 earnings sheet: the bank beat EPS estimates and reported a much narrower loss compared to Q1’23. The merger is a win-win situation for the bank and its shareholders, in my opinion, because it creates a larger regional bank and investors have had considerable concerns about PacWest Bancorp’s ability to survive. Given the circumstances, I believe it is overall a good outcome for PacWest Bancorp’s shareholders. Shares traded at about $10.50 before rumors about a merger spread yesterday, and I would expect the PacWest Bancorp share price to return to $10+ in the short term. Since the upside in PacWest Bancorp is now limited, given the deal terms, I am downgrading PACW to hold!

Read the full article here