I’ve covered the Vanguard International High Dividend Yield ETF (NASDAQ:VYMI), a diversified index ETF focusing on international stocks with above-average yields, several times in the past. Considering recent market movements, I thought to write a quick article on how VYMI’s performance and fundamentals have evolved these past few months.

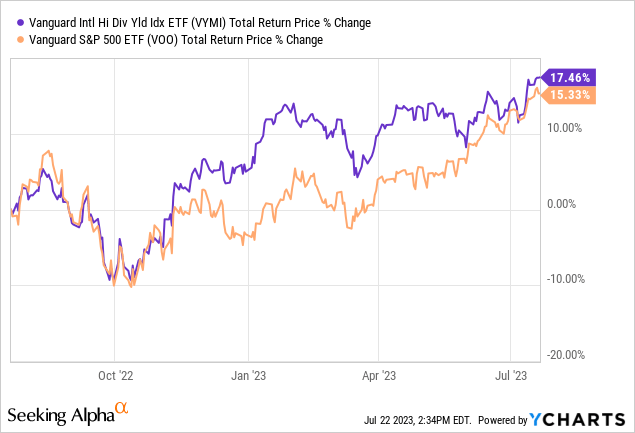

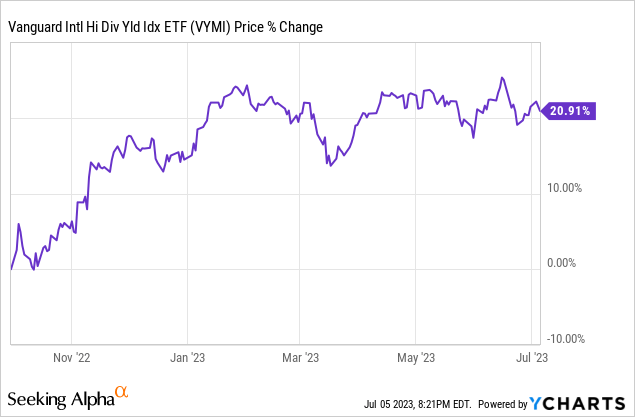

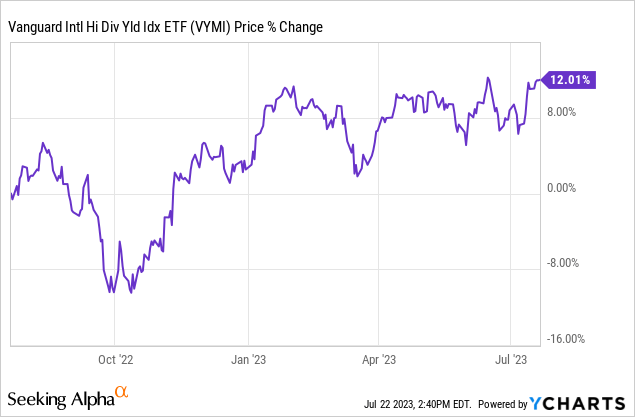

Dollar prices have declined since late 2022. This led to strong capital gains and some outperformance since then:

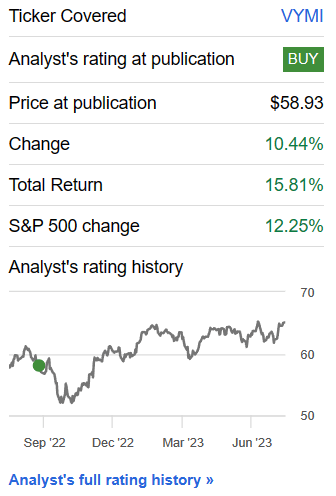

VYMI Previous Article

The dollar is looking reasonably priced right now, so I’m not expecting further gains from currency price movements.

VYMI’s valuation remains quite cheap, while U.S. equity valuations have risen. Wider valuation gaps mean strong capital gains are somewhat likelier moving forward.

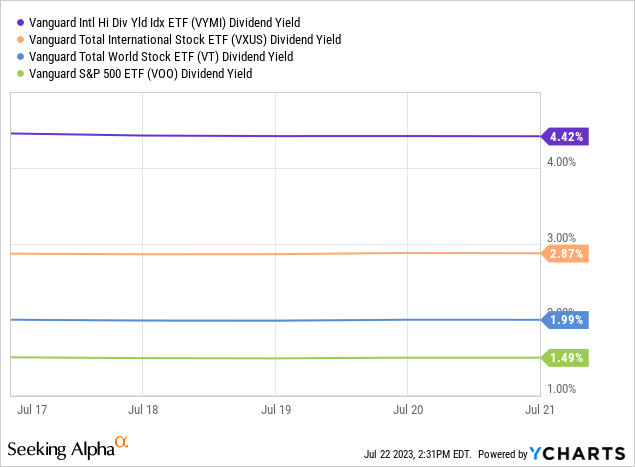

VYMI’s yield has decreased to 4.4%, due to a higher share price, and, in my opinion, due to ETF dividend volatility.

In my opinion, VYMI’s fundamentals have very slightly worsened these past few months. Nevertheless, the fund remains a strong investment opportunity, due to its cheap valuation and above-average 4.4% dividend yield.

VYMI – Quick Overview

A quick look at the fund before analyzing some recent developments.

VYMI is an index ETF, tracking the FTSE All-World ex US High Dividend Yield Index. Said index includes the top 50% highest-yielding international stocks, subject to a basic set of inclusion criteria. As the yield inclusion criteria is quite lax, the fund is quite broad, with investments in over 1,000 securities, from all relevant industries and international regions.

VYMI

VYMI

VYMI focuses on stocks with above-average yields, which results in an above-average 4.4% yield for its shareholders.

VYMI is a relatively cheap fund, as international stocks tend to trade with cheap valuations, as do stocks with high yields.

VYMI

VYMI’s valuation is more than 50% lower than that of the S&P 500.

VOO

VYMI’s investment thesis is simple: the fund’s dividends and cheap valuation could lead to strong, market-beating returns moving forward. Returns are somewhat dependent on investor sentiment improving, as valuation gaps will not narrow on their own. Sentiment seems adequate, with VYMI seeing strong returns since late 2022, with some volatility.

With the above in mind, let’s have a look at some of the fund’s recent developments.

VYMI – Recent Developments

Dollar Price Movements

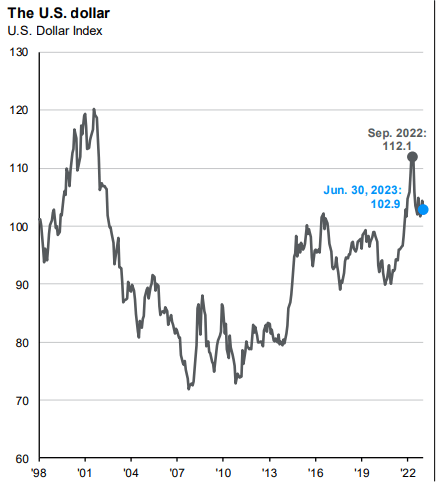

Dollar prices have declined almost 10% since September 2022:

JPMorgan Guide to the Markets

Two reasons for the above.

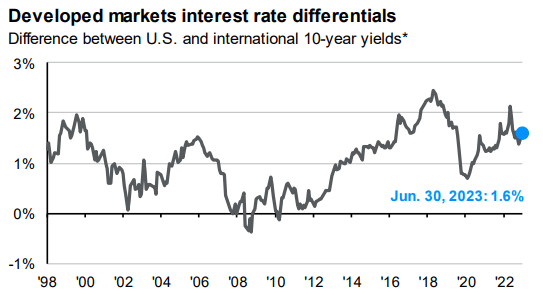

First, interest rate differentials between comparable U.S. and international securities declined. This was due to the Fed turning more dovish (less hawkish), and as markets have come to expect rate cuts in the coming months, and are pricing bonds accordingly. As interest rate differentials decline, so does the relative attractiveness of dollar-denominated securities, leading to lower demand for dollars, and hence lower dollar prices.

JPMorgan Guide to the Markets

Second, is due to prices simply normalizing: the dollar was unsustainably high in the past, prices have dropped to more reasonable, more sustainable levels since.

Lower dollar prices meant higher foreign currency prices, and higher values for most foreign currency investment assets. VYMI’s share price itself increased by over 20% peak to through, although that was with perfect timing.

Data by YCharts

Right now, dollar prices are around 2% higher than their historical averages, and around 5% – 10% higher than in the years prior from the pandemic. Under these conditions, further significant gains seem unlikely, although smaller, marginal gains remain possible. In my opinion at least.

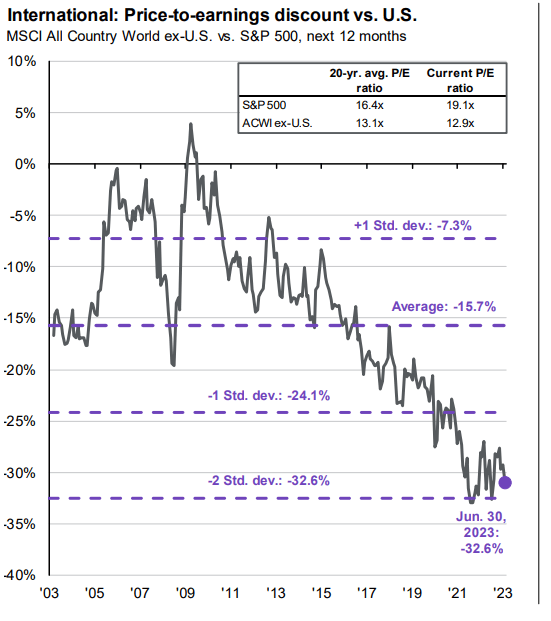

VYMI Valuation Analysis

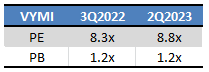

VYMI’s valuation has become a tad pricier these past few months:

Fund Filings – Chart by Author

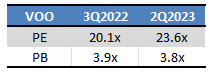

U.S. equities have become more expensive too, and by a wider margin. Data for the S&P 500:

Fund Filings – Chart by Author

Due to the above, valuation gaps between international and U.S. equities have widened these past few months. Bear in mind, there has been a lot of volatility, so this does vary month to month, and valuation gaps were wider several times in the recent past.

JPMorgan Guide to the Markets

VYMI’s cheap valuation could lead to strong capital gains and market-beating returns moving forward, contingent on valuations normalizing. Valuations could normalize due to improved investor sentiment, economic fundamentals, investor inflows, and a myriad other factors.

In my opinion, the valuation gap between international equities and U.S. equities is likelier than not to narrow moving forward, for several reasons. International equities have seen strong gains and some outperformance in the recent past. Economic fundamentals in Europe are improving. Fed has stopped hiking, for now at least, so the dollar could go (slightly) down. Investor sentiment is improving, at least for European equities. On a more negative note, these are not significant catalysts, and have led to barely any international equity outperformance in the past.

As a final point, a cheaper dollar decreases VYMI’s potential capital gains, while a comparatively cheaper valuations increases these. The net effect is about zero, considering both have similar magnitudes, of around 10%.

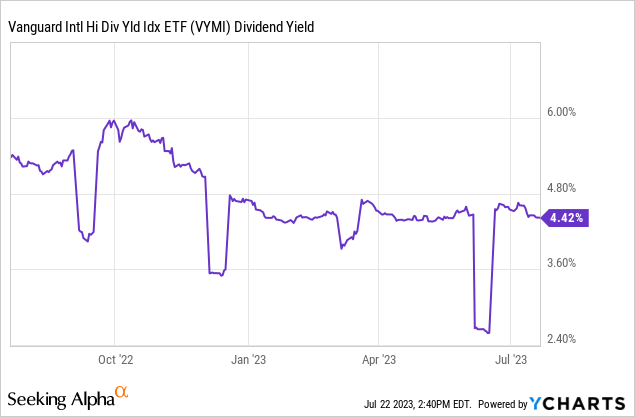

VYMI Dividend Analysis

VYMI’s dividend yield has steadily decreased from around 6.0% in September, to 4.4% as of today (ignore the gaps below, those are data collection / calculation issues):

VYMI’s lower dividend yield is mostly due to higher share prices / capital gains:

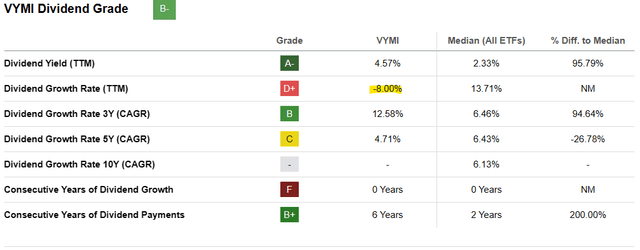

VYMI’s lower yield is also the result of lower dividends, with these decreasing by 8.0% these past twelve months:

Seeking Alpha

Importantly, I believe that the above was mostly due to normal ETF dividend volatility, and not due to a real, long-term decrease in the fund’s dividends or underlying generation of income. From what I’ve seen, growth looks weak now due to abnormally large dividend payments all the way back in 2021. Excluding these payments, and focusing on the dividends paid YTD, shows positive dividend growth of 4.9% for the fund. Dividend volatility impacts these figures too, however.

Seeking Alpha

As VYMI’s lower dividends are the result of normal dividend volatility, I don’t see them as negatives per se. The volatility itself is definitely a negative, although one that is common to most ETFs.

Conclusion

VYMI’s investment thesis rests on the fund’s above-average 4.4% dividend yield, and cheap valuation. Recent economic and market trends have impacted the fund’s fundamentals, but with limited impact on the fund’s investment thesis and prospective returns.

Read the full article here