PIMCO Global StocksPLUS and Income Fund (NYSE:PGP) is a closed ended fund managed jointly by PIMCO and Allianz Global Investors. The fund’s goal is to generate a dividend yield around 8-10% for income seeking investors. Founded in 2005, the fund invests into stocks, corporate bonds, preferred shares and futures contracts to generate income.

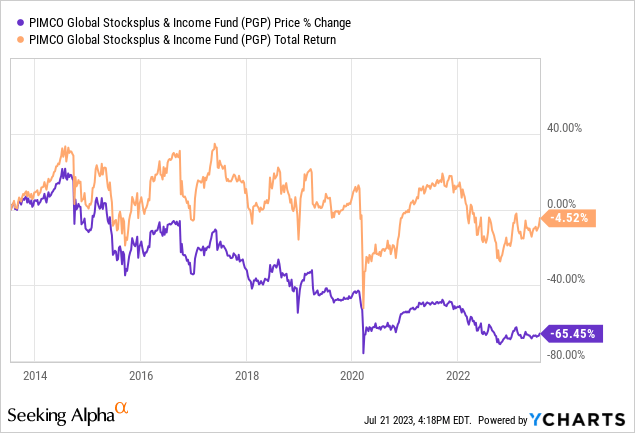

Unfortunately, the fund’s long term performance leaves a lot to be desired. In the last decade, the fund’s share price is down -65% and its total return is down -4.52% including reinvestment of dividends. There were periods in the past where the fund enjoyed positive returns, but those periods were either brief or did not result in strong gains (around 3-4% annually compounded). When it comes to high yielding funds, you want that fund’s annual total returns to be at least half of its yield. For example, if a fund yields 12%, its annual total compounded returns should be at least 6% but ideally closer to 12% if it were to be worth investing in.

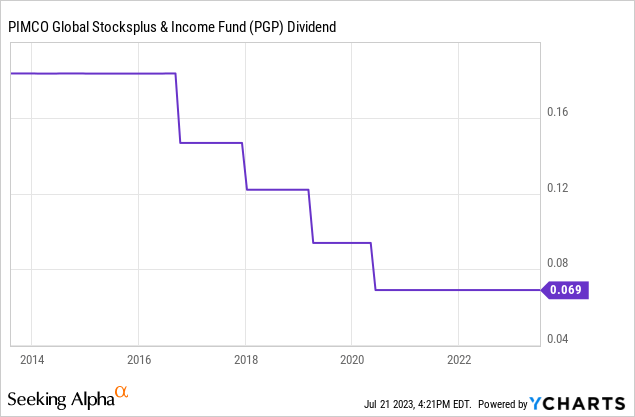

This could be forgiven if the fund posted dividend growth or at least stable dividends, but this fund has a history of cutting dividends every few years. A decade ago it was paying close to 20 cents per share (on monthly basis) which was cut to 15 cents in 2017, 12 cents in 2018, 10 cents in 2020 and 7 cents in 2021. If you bought the stock for its 10% yield a decade ago and held until now, your current yield to your original cost would be only 3.75%. Add inflation to the mix, and your real yield against your original cost would drop to below 2%. So much for buying this fund for high income.

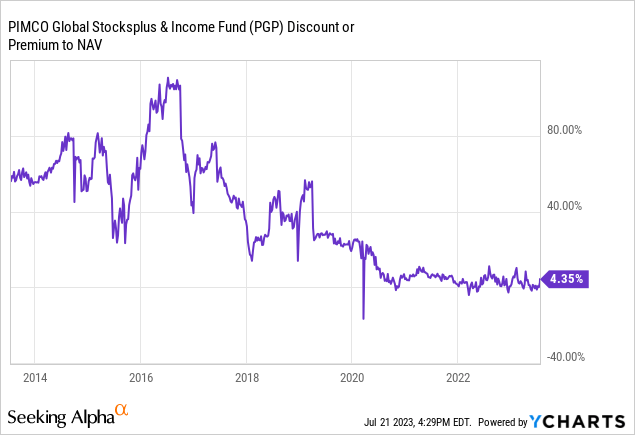

Then why did the fund perform so badly over the years? One reason is its valuation. This fund used to trade at a pretty sizeable premium against its NAV not long ago. In the last decade, PGP’s NAV premium ranged from 0% to north of 90% (with the exception of a very brief period in 2020 when it traded at a discount against its NAV, but this only lasted a couple of weeks). If you buy a fund that trades at a 50% premium against its NAV and the premium suddenly drops to 10%, your portfolio will lose a significant amount of value even if the NAV stayed flat. If a fund goes from 20% premium to 0% premium, that’s a 20% drop in share price. Interestingly enough, the fund is still trading at a premium of 4.35% despite its bad performance history.

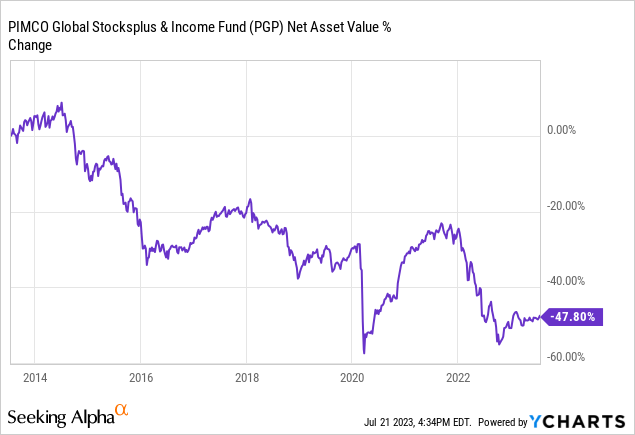

But this is not the whole story either. Even if we completely ignore the large premium against the fund’s NAV, we are still seeing a NAV decline of -47% over the last decade. Some of this is expected since dividend payments get deducted from NAV, but this drop is still very steep and indicating that something is simply not working with the fund, and we can’t say that the share price drop we’ve seen in the last decade mostly came from declining NAV premium.

Another possible reason for the fund’s underperformance is leverage. Currently, the fund has a leverage ratio of 23% which may not sound like much but keep in mind that this came after an entire year of deleveraging. PIMCO has been reducing leverage in many of its funds since last year.

PGP’s leverage ratio (Pimco)

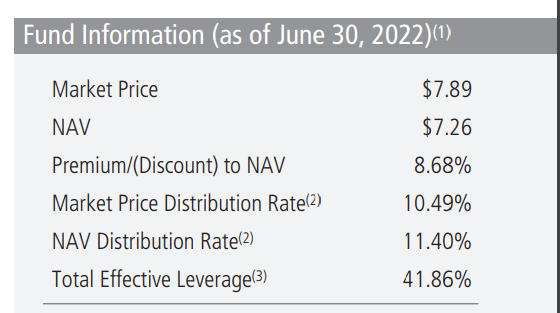

Below you’ll see that the fund had a leverage ratio of 42% as of June of last year, which is more than twice the current leverage ratio of 23%. Also notice that the fund had a NAV premium of 8.68% at the time.

PGP characteristics in June 2022 (Pimco)

Historically, this fund ran at a leverage ratio around 50%, and I could see them returning to that rate once the bear market in bonds (which has been going on since late 2021) comes to an end.

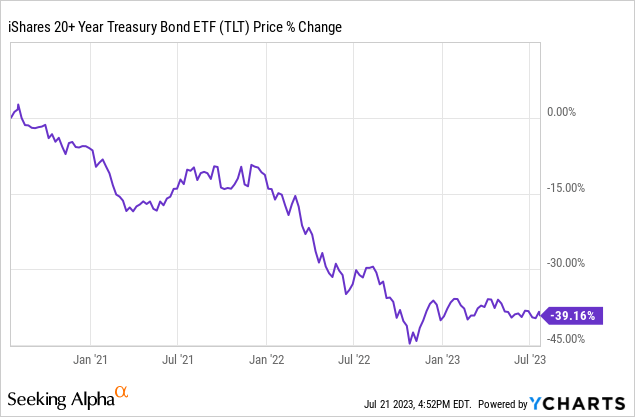

The fund invests in a lot of high risk assets such as mortgage backed securities, corporate bonds with junk rating, emerging market debt and other instruments. These instruments are risky enough as it is, and they become even riskier when you are highly leveraged. Sometimes people say that government backed mortgage backed securities are risk-free because the government promises to pay them back if the debtor fails to make payments, but this doesn’t mean that those assets can’t fall in value. If a MBS asset falls 50% in value and a fund is 50% leveraged in them, they could lose up to 75% of their portfolio value. Even government’s own bonds which are considered risk-free fall in value from time to time.

Since late 2020, long term government bonds lost about -40% of their value even though they are considered “risk-free” because the US government has never missed a coupon payment, but this doesn’t mean investors haven’t lose a lot of money in them. If investors were sufficiently leveraged in these bonds, they could even get completely wiped out even though they invested in “risk-free” bonds. This is also one of the reasons why several regional banks were in deep trouble earlier this year. There is no investment that’s completely risk-free, but even if there was, risk-free doesn’t mean an asset can’t drop in value.

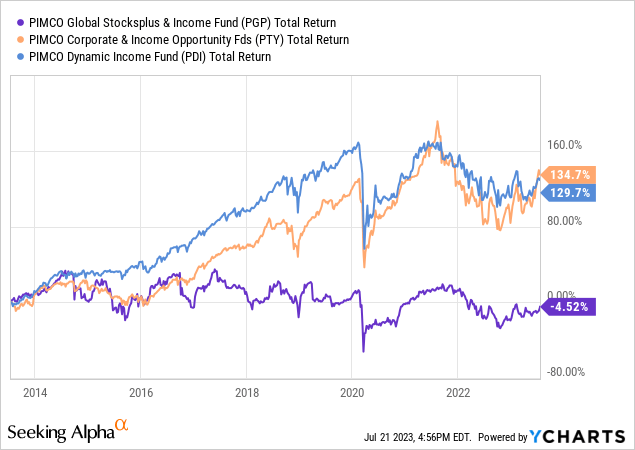

Don’t get me wrong, I am not saying all PIMCO funds are bad. In fact, PIMCO has a lot of good quality funds. Two such funds are PTY (PTY) and (PDI) both of which resulted in strong performance in the last decade, with PTY being up 134% and PDI being up 130%. Both funds have high yields in double digits and both seem to be working fine. If you must invest in a PIMCO fund, why not one of those instead of PGP?

In conclusion, I don’t think PGP is the best fund out there. You can easily find better alternatives even within other PIMCO offerings. There is no reason to tie your money in an asset that loses so much value during a period where virtually all assets gained value.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Read the full article here