Crane ships and construction barges have joined the pleasure boats floating off the coast of vacation hot spots Montauk and Martha’s Vineyard this summer. The hard hats working on them aren’t there to catch some rays. They’re driving steel cylinders deep into the seabed to build America’s first large-scale offshore wind farms, a milestone decades in the making. Both projects are set to start sending electricity to the shore by the end of the year.

Public officials in New York and Massachusetts toasted the news last month when the first turbine foundations were installed. “The windmills that will power hundreds of thousands of homes are beginning to emerge from the water,” said Massachusetts House Speaker Ronald Mariano. Offshore wind is a crucial technology to decarbonize large coastal population centers, including cities like Boston and New York that probably wouldn’t be able to go green without it. So, its arrival is a major milestone in the nation’s energy transition.

But behind the scenes, the news about wind power is more sobering. Financially, the industry is teetering, with a parade of companies planning to renegotiate or pull out of contracts, jeopardizing plans for projects that were expected to provide electricity for millions of homes. Inflation is erasing profits, causing some of the largest energy firms in the world to back away. “Returns on offshore wind are becoming more and more challenged,”

Shell

CEO Wael Sawan told Barron’s last month, just days after a Shell joint venture said it would pull out of a power contract in Massachusetts. Shell won’t build renewable projects that can’t earn initial returns of 6% to 8%, he said.

At least eight multinational companies in three states have quietly started to back out of wind contracts, or ask to renegotiate deals in ways that will pass more costs to consumers. Beyond Shell (ticker: SHEL), they include

BP

(BP), Denmark’s

Orsted

(DNNGY), Norway’s

Equinor

(EQNR), Spain’s

Iberdrola

(IBDRY), Portugal’s

Energias de Portugal

(EDPFY), and France’s

Engie

(ENGIY) and state-owned Electricite de France. The projects those companies are building will collectively cost tens of billions of dollars to construct and connect to the grid. The cost problems they’re facing make offshore wind a dicey investment proposition today, with the potential for substantial write-downs ahead.

America’s pledge to decarbonize is at risk, too. President Joe Biden announced a goal in 2021 to have 30 gigawatts of offshore wind power installed by 2030, enough to power roughly 10 million homes, up from essentially zero today. “We’re going to make sure that the ocean is open for the clean energy of our future,” Biden said last year.

Credit Suisse analyst Mark Freshney says there’s little chance that the country will reach Biden’s goal.

“We won’t get there,” he says. “We might get to 15.”

The White House didn’t respond to a request for comment, but other Biden administration officials dispute Freshney’s prediction. “The Biden-Harris administration remains committed to pursuing a goal of 30 GW of offshore wind by 2030, and we remain on track to meet that goal,” wrote a spokeswoman for the Bureau of Ocean Energy Management, which handles offshore leases. Combining two projects that are now under way and 16 other plans that it’s currently considering, the BOEM says there are 27 gigawatts of offshore wind projects that are in the pipeline. Most are along the East Coast from Maine to Virginia, but the government has also leased parcels off California and is preparing lease offerings in the Gulf of Mexico.

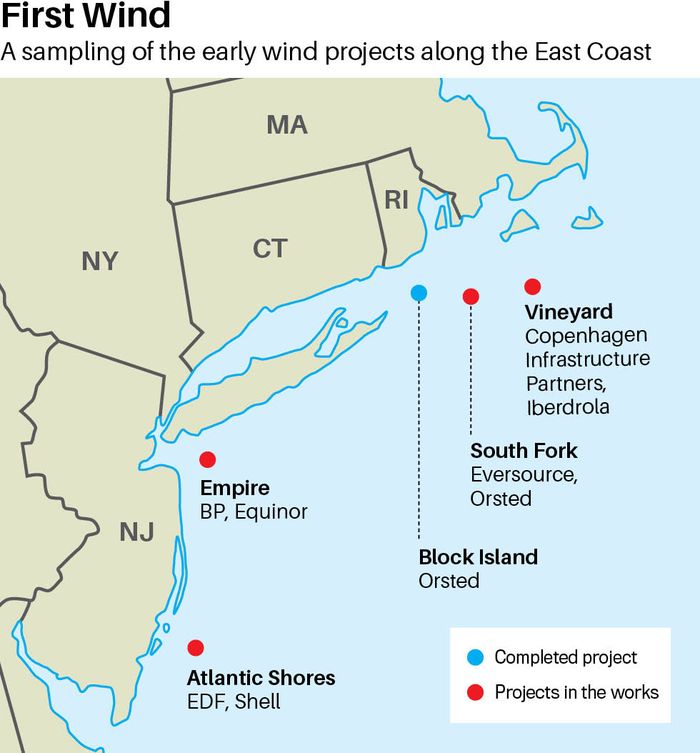

Offshore wind’s arrival in America has been a long time coming. Outside the U.S., 64 gigawatts of offshore wind had been installed as of the end of last year, a number expected to double by the end of 2025. While Europe started building farms in the 1990s, the U.S. has been much slower to adopt the technology, and some efforts have failed. A project off the coast of Cape Cod, Mass., announced in 2001, ended up snarled in litigation after local residents complained about the turbines spoiling their views. It died quietly in 2017. Today, there are only two operating offshore wind farms in the U.S.—one off Rhode Island and one off Virginia—generating a combined 42 megawatts, less than 0.1% of global offshore wind capacity.

The problems with launching offshore wind projects in the U.S. go beyond obstructed views. For years, the cost of installing the turbines was too high compared with the power that those turbines produced. Europeans have been less sensitive to higher prices because they already pay a premium for electricity compared with American consumers, who benefit from abundant coal and natural-gas reserves.

A decade ago, the U.S. government estimated the cost of electricity from a new offshore wind farm at more than $200 per megawatt-hour, twice as expensive as coal, and three times more than advanced natural-gas-fired plants. Since then, offshore wind costs have fallen dramatically—more than half, by most measures. The U.S. is also giving tax credits to qualifying projects that can be worth as much as $26 per megawatt-hour, bringing offshore wind costs to around $75—about $15 cheaper than a new coal plant.

One reason wind costs have declined is that turbines themselves are much larger and more efficient than they used to be. Turbines that companies were installing a decade ago were half as tall and about a quarter as powerful as today, says Christian Skakkebæk, senior partner at Copenhagen Infrastructure Partners, a renewable-energy fund manager that’s a half-owner of the Martha’s Vineyard project. That project’s turbines will rise 837 feet, almost three times as tall as the Statue of Liberty. And because the turbines will be 35 miles off the coast, they are barely visible from oceanfront property.

| Company / Ticker | Recent Price | YTD Change | Market Value (bil) | 2023E P/E | Offshore Wind Plans |

|---|---|---|---|---|---|

| BP / BP | $36.15 | 3.5% | $104.6 | 6.4 | CEO Bernard Looney called offshore wind “challenged.” Its New York project is looking to renegotiate electricity contracts. |

| Equinor / EQNR | 30.09 | -16.0 | 90.4 | 7.2 | Norway’s energy giant is partnering with BP in New York and planning to build floating wind platforms near California. |

| Iberdrola / IBDRY | 50.20 | 7.4 | 80.5 | 15.4 | The Spanish utility is behind the successful Vineyard Wind project and rockier Commonwealth Wind project in Massachusetts. |

| Orsted / DNNGY | 31.26 | 3.5 | 39.4 | 38.1 | Its global market share in offshore wind is 29%, but could slip as bigger energy companies plow money into the industry. |

| Shell / SHEL | 61.73 | 8.4 | 206.9 | 7.2 | The oil giant’s joint offshore wind venture in Massachusetts announced it doesn’t plan to proceed with its contracts. |

| TotalEnergies / TTE | 58.61 | -5.6 | 146.4 | 5.9 | A large ocean lease the French energy company signed last year near New York could make it a major offshore wind player. |

E=estimate

Sources: Bloomberg; Credit Suisse; company reports

Those towering turbines point to the industry’s potential. Offshore wind can solve problems that other forms of renewable energy can’t. Land-based wind power is cheaper than offshore and already accounts for 10% of U.S. electricity production, but it isn’t feasible in many areas. Developers need to negotiate with private landowners for space and often face opposition because of visual impacts. The turbines can’t be nearly as tall and powerful as the ones in the water. Wind gusts off the coast are also much steadier than they are onshore.

The East Coast is particularly appealing for offshore turbines. The water is shallow, and the ocean floor is sandy rather than rocky, allowing steel to be installed directly into the ground instead of having to rely on more-expensive floating platforms. The wind is consistently strong. “That combination of robust wind and shallow waters could make Massachusetts the Saudi Arabia of wind,” says Massachusetts State Rep. Jeff Roy, the chairman of the Joint Committee on Telecommunications, Utilities, and Energy.

Offshore wind isn’t going to be the main solution to decarbonizing the U.S. power grid, but it solves key problems that have kept high-population areas from going green, says Skakkebæk. New York, for instance, has said its electricity will be carbon-free by 2040. For now, natural-gas power plants account for nearly 60% of its generating capacity. The state is unlikely to reach its goal without offshore wind.

The new, more urgent age of American offshore wind started at the tail end of Barack Obama’s presidency, when the BOEM began leasing more large ocean-bed parcels for wind development. The agency has now approved leases on more than 2.7 million acres of ocean bottom, an area equivalent to a square more than 60 miles on each side.

It’s what happens after leases are signed that has stalled the process. The gap between when offshore wind developers secure rights and when the first steel enters the water can run many years. The Montauk project that just placed its first turbine won its lease in 2013, and has since been navigating various approval processes. To get a project off the ground, developers have to wait for states to hold bidding processes to supply power to regulated utilities. After that, the permitting process to lay cables and protect marine life can take years, not to mention the possibility of legal challenges. In that period, developers face considerable inflation risks.

Companies now caught in the inflation trap are almost all from the other side of the ocean. The projects being developed along the East Coast may have American-sounding names like Commonwealth Wind, but they’re backed almost entirely by European companies that pioneered the modern wind industry and have been working on it for decades. Outside of

General Electric

(GE), few large U.S. firms are involved. Denmark’s Orsted is the market leader, and its stock the purest play on wind development. Utilities from several European countries have also invested heavily through U.S. subsidiaries.

Companies such as BP, Shell, and Equinor, known for oil production, have lately turned to offshore wind to decarbonize their energy mix in the face of government and investor pressure. With high cash flows from fossil fuels in the past few years, those companies plowed large investments into offshore wind.

As competition rose, bids on acreage in one section of the ocean off New York skyrocketed last year. Several European companies, including joint ventures involving

TotalEnergies

(TTE) and Shell, paid more than $700 million each for sections of the ocean bottom. The parcels contained less acreage than farms other companies had leased for less than $10 million prior to the pandemic, according to Freshney, the Credit Suisse analyst. “The cost just went through the roof,” he says. “It was a bubble.”

Other costs soared, too, because of inflation pressures that have also hurt other industries. Steel is much pricier than it was prior to the pandemic, for instance. A consultant hired by the wind developer on Shell’s Massachusetts project estimated that costs have risen more than 20% since 2019, and rising interest rates have added more financial stress. “This is not an industry that is in a healthy and mature state,” the report said. Another problem: The supply chain to build wind turbines is nowhere near ready to handle the influx of projects. Installation capacity is at 20% of where it needs to be, according to a study by energy consultant Wood Mackenzie.

Now, states are trying to manage the fallout. Offshore wind projects backed by Shell, BP, Iberdrola, and several others have already said they need to renegotiate the contracts, with the implicit—and sometimes explicit—threat that they could pull out. The new terms will have to be more lucrative for project developers, with electricity prices probably linked to inflation.

Regulators now face a “huge problem from a ratepayer’s perspective,” said Ronald Gerwatowski, chairman of the Rhode Island Public Utilities Commission, at a recent hearing about offshore wind. Developers can essentially hold regulators hostage by threatening to walk away from already-permitted projects unless rates are hiked.

Already, some states have agreed to change policies in a way that could lead to more-expensive rates. In Maryland, a new law shifts some of the federal Inflation Reduction Act’s support from consumers to wind developers. Previously, Maryland law said 80% of the federal benefits had to go to the consumers.

New Jersey’s legislature also just passed a law that will redirect federal tax money to Orsted to complete an offshore project known as Ocean Winds 1 that will supply enough power for 500,000 homes. Those funds were previously expected to go to electricity consumers. Republicans opposed it, with state Sen. Edward Durr calling it a “huge handout at the expense of New Jersey utility customers,” one that could cost up to $1 billion. Orsted tells Barron’s that the bill denied each New Jersey ratepayer only about $2.40 per year, and won’t result in a real hike in electricity rates.

After New Jersey passed the bill, developers of another wind project in New Jersey—Atlantic Shores, backed by Shell and French utility EDF—said they needed similar support. “Tens of thousands of real, well-paid, and unionized jobs are at risk,” the developers said. “Hundreds of millions in infrastructure investments will be forgone without a path forward.” The governor’s office declined to comment about the request.

Orsted is also talking to New York officials about boosting payments to wind developers based on inflation rates. New York’s new contracts have mechanisms that allow for inflation adjustments, but the contracts that Orsted signed in the past don’t.

“We sign multidecade contracts to sell the power at an agreed price before the project is ever built,” says Orsted spokesman Ryan Ferguson. The per-megawatt value has to pencil out over a 25-year contract, but “they’re not doing so based on current development costs.”

New York officials say they are reviewing Orsted’s proposals for inflation adjustments. The state is already expecting wind power to be more expensive than other sources. “Electricity consumers across the state can expect to see slight increases in electricity bills to support offshore wind development once the projects enter commercial operation,” says a spokesman for the New York energy agency.

Equinor and BP also have two projects in the state, and have asked officials to reconsider the rates they originally signed on for. The companies “have seen the estimated costs of our projects rise sharply,” said Teddy Muhlfelder, an executive at Equinor Renewables Americas, in a statement. The companies remain “strongly committed” to the projects, and are looking for a way forward, he added. The state is reviewing the request.

By next year, Massachusetts residents will be receiving 800 megawatts worth of wind energy from the Martha’s Vineyard project, enough to power 400,000 homes or so. But developers of two other projects in the state that collectively were expected to add 2.4 gigawatts—three times as much as the Vineyard project—have attempted to pull out of their contracts. Commonwealth Wind, owned by a subsidiary of Iberdrola, just reached a deal with three utilities to terminate its contract and pay a $48 million fee. And developers of SouthCoast Wind, owned by Shell, EDP, and Engie, said last month that they’re planning to terminate their contract. In a statement, Rebecca Ullman, SouthCoast’s director of external affairs, said the company is still in discussions with utilities over the contracts and is “looking forward to future [offshore wind] procurements in New England.”

Massachusetts just released a new draft request for proposals that could push the whole process back considerably, and allows for more inflation-related adjustments. Roy, the state legislator, said in an interview that he now expects Massachusetts’ major wind projects to come into service in 2031 or 2032, instead of in the late 2020s, and be “more costly.”

State regulators and utilities have fought some proposals to pay wind developers more, but momentum is building for these contracts to be repriced or rebid. That gives the companies a better chance to make adequate returns—though Freshney anticipates asset impairments ahead as higher construction costs diminish their expected profits.

Some companies are eyeing novel strategies to make wind projects pay off. BP CEO Bernard Looney said in an interview with Barron’s earlier this year that BP plans to juice returns by integrating the power its wind turbines produce into other segments of its business—essentially upselling the electrons into its hydrogen and electric-vehicle-charging businesses. “We will have a 10 gigawatt demand for electrons in our own charging infrastructure,” he said. Shell’s Sawan has outlined a similar strategy.

But even with those potential projects, the public investment case for offshore wind now looks iffy. Orsted, the most direct way to bet on offshore wind, has already written down the value of one of its U.S. projects. The stock is up 25% from its October lows, but it’s too soon to signal an all-clear. The industry may be in the early stages of a bad-news cycle, with more impairments to come at various companies, Freshney says. Other issues loom, including protests about how the turbines impact whales.

Eventually, hundreds of turbines are likely to be humming up and down the coasts, and in the Gulf of Mexico, too. They will represent a step forward in the fight against climate change. Paying for them will be anything but a breeze.

Write to Avi Salzman at [email protected]

Read the full article here