Investment Thesis

Block (NYSE:SQ) has faced downward pressure on its stock price since early FY2022, primarily due to a significant deceleration in top-line growth resulting from many factors, such as pull-forward demand, a decline in B2B spending, and increased competition. Despite delivering decent 1Q FY2023 results, the stock’s performance was muted, with only a 2% rally in the aftermarket. SQ’s lackluster YTD return (recently exhibited some upside momentum due to the decline in CPI data) clearly indicates that it missed out on the hype surrounding the recent AI thematic rally. This mediocre performance was below both the S&P500 and Nasdaq, as the company failed to impress investors with its long-term AI roadmap.

I admit that SQ’s fundamentals, particularly its bottom-line, have significantly deteriorated over the past year. However, the company is now focusing on improving margins and driving earnings growth in FY2023. Although the valuation is still not at a bargain, even after a 72% pullback from its pandemic peak, I believe that investors will appreciate the company’s efforts to prioritize profitability and FCF profile. Additionally, we have seen a strong recovery in cryptocurrencies in recent months, which could boost its Bitcoin Gross Profit line. Therefore, I remain optimistic about the stock, as the worst may be behind us.

Look Through Near-Term Headwinds

The company model

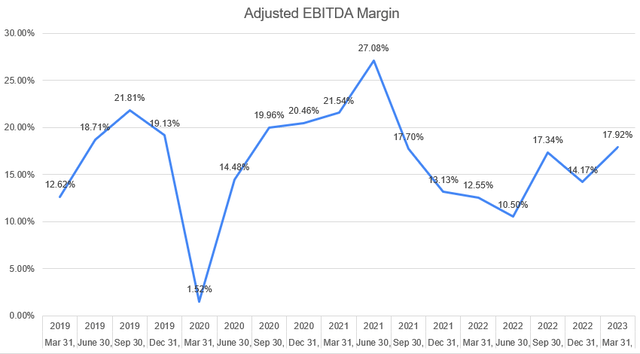

Investors may be curious about the reasons behind SQ’s sharp 75% drop in early FY2022 and why its upward momentum has been limited since then. Some may argue that considering the company’s FY2023 adjusted EBITDA outlook, SQ has maintained an impressive 34.4% CAGR in adjusted EBITDA from FY2019 to FY2023E.

The company model

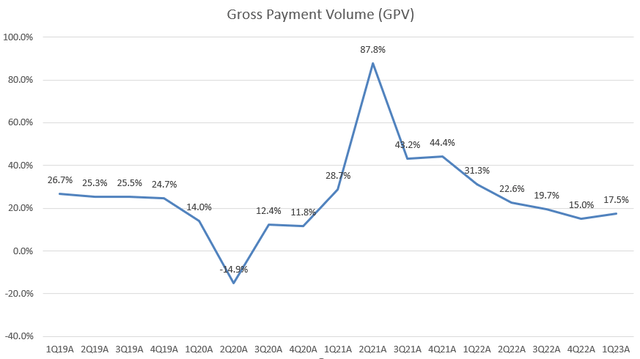

In reality, there were both macro and micro challenges in FY2022. Firstly, SQ’s fundamentals saw a significant decline. The company experienced a sharp decrease in transaction-based revenue due to sluggish growth in GPV. The point-of-sale (POS) industry has become increasingly competitive, with some major players expanding their market shares such as Apple Pay. As a result, SQ’s adjusted EBITDA growth declined by -2.2% YoY in FY2022, leading to a -41.5% YoY growth in adjusted EPS. This indicated that the stock price could easily drop 41.5% without impacting its valuation.

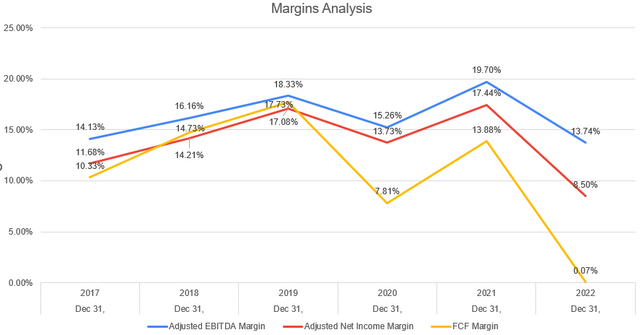

Additionally, when examining the chart, we can see that three key margins (adjusted EBITDA margin, adjusted net income margin, and FCF margin), which most investors focus on, were at their lowest levels since FY2017.

From the Macro perspective, the federal fund rate has sharply increased in FY2022 as the fed became hawkish to combat 40-year high inflation. Under this backdrop, high growth stocks with deteriorating fundamentals like SQ were particularly vulnerable. Therefore, I wouldn’t be surprised to see the stock experienced a significant selloff.

Nevertheless, as a long-term investor, we should look through the company’s near-term headwinds and focused on its secular growth catalysts. For example, the pandemic has undoubtedly accelerated the digital transformation, with more merchants and customers relying on fintech transaction products and services.

Connecting Square Ecosystem and Cash App

2022 Investor Day

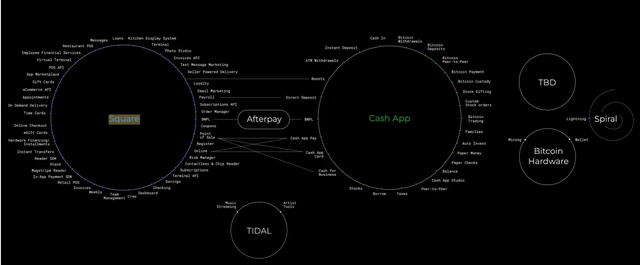

During the Investor Day in 2022, it was highlighted that Square’s business model has undergone significant changes over the past few years. In 2015, a majority of their gross profit was derived from merchants using Square for Payments. However, by 2021, the largest revenue stream has shifted to software and integrated payments, which, along with banking and international operations, have been growing at a faster pace than payments revenue. As the screenshot indicated, the company is currently focused on integrating Afterpay into its ecosystem, aiming to establish a connection between Square and Cash App. This integration is expected to be beneficial in terms of customer acquisition and increasing the lifetime value to customer acquisition cost (LTV/CAC) ratio over the long term.

Nevertheless, the management has cautioned that the integration of Afterpay may temporarily impact margins. However, they remain optimistic about the future synergies and potential benefits associated with the deal.

We can observe in Historical Financial Information that Cash App’s margins are currently lower than those of Square due to higher variable expenses such as P2P processing, risk loss, and card issuance costs.

Cash App Margin Remains Robust

Investor Relations – Historical Financial Information

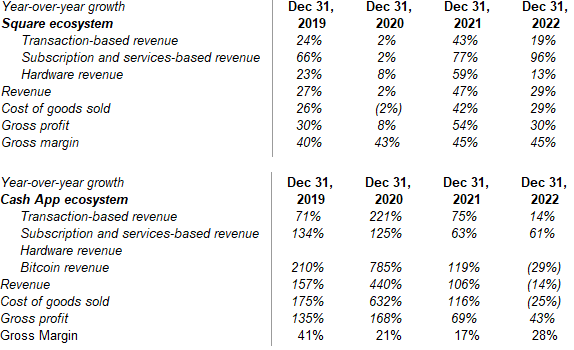

Based on the screenshot from the company’s Excel model, we saw that the growth of subscription and services-based revenue remains strong in both Square and Cash App ecosystem. The Cash App growth history has been remarkable, with a 61% YoY growth in FY2022. The gross profit of Cash App has been largely contributed by Instant Deposit and Cash App Card, which achieved an impressive 43% YoY growth in the last fiscal year. Moreover, the introduction of savings accounts and the Cash App Card has also played an important role in expanding monetization over the long term.

As mentioned earlier, the Cash App ecosystem currently maintains a lower margin of 28% compared to the Square ecosystem’s margin of 45%. However, there has been a notable improvement in margins, with a strong expansion from 17% in FY2021.

In addition, we should keep in mind that the gross profit from the Cash App ecosystem was affected by a significant slowdown in Bitcoin transactions during FY2022. However, considering the recent strong recovery in cryptocurrencies, this could potentially generate positive sentiment among investors.

Margin Improvement in FY2023

The company model

Indeed, FY2022 was a challenging year for SQ. However, there are many positive signs to consider. The adjusted EBITDA margin has rebounded from its recent low, indicating a positive trend. Additionally, in 1Q FY2023, the company not only exceeded expectations in terms of revenue and adjusted EPS but also raised its FY2023 outlook for adjusted EBITDA. During the earnings call, the management is expected to see an expansion in Cash App margin, which would contribute to overall margin expansion for the company. This suggests that investors can anticipate a recovery in profitability in the current fiscal year. If SQ can sustain consistent earnings growth and continue expanding its margins, it should boost more confidence in investors, even in the face of a slowdown in overall top-line and GMV growth.

Valuation

1Q23 Shareholder Letter

When considering SQ’s adjusted EBITDA outlook for FY2023, the stock is currently trading at a higher multiple compared to PayPal (NASDAQ:PYPL). SQ’s EV/adjusted EBITDA FY2023E stands at 32.7x, while PYPL is at 10.5x. Similarly, SQ’s P/E Fwd of 42x is higher than PYPL’s 14.3x, despite SQ’s strong rebound in adjusted EPS. Therefore, I don’t consider SQ as a value stock right now. However, I believe that SQ can demand a higher multiple due to its greater growth potential and strong outlook for margin expansion compared to peers.

Furthermore, the June CPI report indicates a significant decrease in inflation, with YoY inflation standing at 3% and core CPI dropping to 4.8%. This reduction in inflation could serve as a positive catalyst for high valuation growth stocks like SQ. If the US economy achieves a soft-landing scenario, SQ’s valuation could be supported by lower inflation expectations and a favorable outlook on long-term interest rates.

Conclusion

In conclusion, despite a 72% drop in stock price from the pandemic high, SQ shows many positive signs with an anticipated rebound in margin and profitability in FY2023. Moreover, Cash App’s growth remains strong, driven by Instant Deposit and Cash App Card. While SQ’s valuation may not currently be considered a bargain, as the fintech market leader, its potential for top-line growth and margin improvement following a cyclical downturn justifies a higher multiple compared to its peers. Most importantly, lower inflation expectations indicated by the June CPI report could benefit high valuation growth stocks like SQ. Therefore, considering the recent muted price action, I maintain a positive on the stock and view this as a potential buying opportunity for long-term investors.

Read the full article here