Investment Summary

Following a series of investment updates since my April publication on Avanos Medical, Inc. (NYSE:AVNS), there is still the potential to unlock further risk in my informed view.

As a reminder, the buy thesis on AVNS is predicated on the following factors:

- The company’s focus on a leaner cost structure, aiming for $55mm in savings by FY’25.

- Reduction in FY’23 sales well anticipated and now baked into equity value.

- Valuations supportive, with my numbers calling for a rating to 54x earnings (104% upside at the time of the April publication).

Here I’ll run through the additional critical facts for consideration in the investment debate, and what’s changed in my investment thesis. Chief among these are the changes to forecasts, obtained via the company’s “transformations” to be achieved this year. Net-net, I am reiterating AVNS as a buy, eyeing the same $40 price objective as in the previous analysis.

Figure 1.

Data: Updata

Critical Factors For Consideration

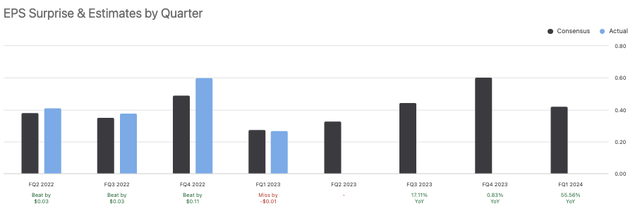

The major critical updates to AVNS’ outlook centre around its most recent numbers and capital management initiatives this YTD. Consensus now sees $0.61 in quarterly earnings by Q4 FY’24, with the ramp on this looking mighty attractive in my eyes [Figure 2].

Figure 2.

Data: Seeking Alpha

1. Divestitures, Investitures

First on the examination plate is AVNS’ sale of its struggling respiratory health business to Sunmed, a provider or anaesthesia and respiratory care services. There are benefits to the deal:

- The transaction will gross AVNS $110mm in an all-cash consideration.

- Perhaps more importantly, however, it frees up a heavy load of capital, and, removes a significant laggard from the company’s portfolio.

- The segment’s sales have struggled in the last few periods, the result of 1) such a high base through the Covid-19 period, and 2) diminishing demand for respiratory–related inventory.

- You’d be looking at Q4 this year for the transaction to settle.

On the acquisition front, the firm also revealed it will buy Diros Technology Inc. in an announcement from June. Diros is a renowned manufacturer of radiofrequency (“RF”), most commonly used in the management of chronic pain.

The Toronto-based Diros has a focal interest in developing radiofrequency ablation (“RFA”) technology. Notably, according to AVNS, there are more than 1mm RFA procedures performed globally, thus making it a potentially lucrative market for AVNS’ chronic pain business. For reference, the RFA procedure utilizes minimally invasive probes to deliver RF energy. It works by heating the nervous tissue near the probe’s tip, and deactivating the nerve’s transmission capability through the blockade of the neurochemistry associated with pain.The acquisition process is projected to conclude in Q3 this year– alas, H2 FY’23 will be a busy year for the company.

2. Financial Headwinds Now Well Accounted For

Investors dumped AVNS shares immediately following its Q1 numbers, wiping more than $5/share in equity value in the days afterwards. They were released in May.

It clipped $192mm in quarterly turnover, down ~300bps YoY. There are FX headwind is baked into this number, but we shouldn’t forget the respiratory business’ lagging effects— it was down another 600bps YoY to $32.4mm in sales.

Regarding the remainder of the top line, note the following:

- The pain portfolio was also down across the board, clipping $70.5mm in turnover, an average 10% decline. Surgical Pain, Game Ready, and the five-shot HA product lines were all down ~10% as well.

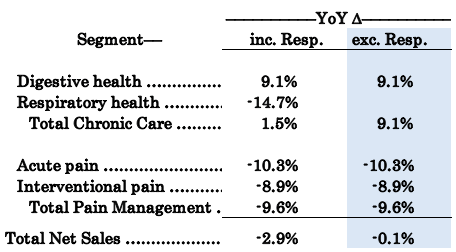

- In chronic care (where the respiratory segment is also found), the digestive health portfolio was a standout. AVNS clipped 36% growth to $88.8mm in the business, and was the best-performing segment in Q1. This is something to take close note of. For starters, the chronic care division won’t have any respiratory health sales as of FY’24. In that vein, it will just be the digestive health business— and this could be a major compounder moving forward, given this momentum.

- I ran a basic thought exercise to remove respiratory from the Q1 numbers in FY’22 and FY’23 [Figure 2]. Doing so, the YoY decline was just 10bps, versus the c.300bps reported. This serves as valuable information moving forward.

Figure 2.

Data: Author, AVNS 10-Q’s

Therefore, following the sharp selloff from Q1, I estimate the company’s adjusted outlook is now well priced in. Evidence for this is seen twofold, 1) in the bounce off the May lows, and 2) with the additional fundamental factors in AVNS investment arsenal.

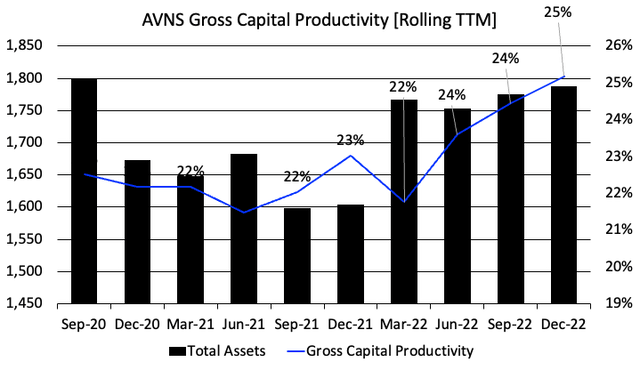

For example, even with the portfolio results of Q1, the company is ratcheting up gross capital productivity. Figure 3 illustrates this point well. You can see AVNS increased operating assets from the 2021–’23 period, most of which came from operating assets (versus cash and equivalents or working capital, for example). At the same time, the company has added another 300bps in gross return from these assets, now producing $0.25 for every $1 in operating assets.

This is pleasing to my investment cortex, and ties into the data shown in Figure 4. You’ll note three major themes here:

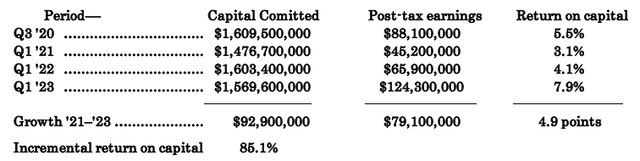

- Looking at Q1 FY’21—’23, AVNS committed an additional $92.9mm to operating capital, generating a further $79.1mm in post-tax earnings from this incremental investment [figures are rolling TTM]. Note, both the capital committed, and the after-tax income, have been adjusted for the firm’s R&D investment— I’ve capitalized it on the balance sheet, and added it back to operating income.

- This resulted in a return on incremental capital of 85.1%, tremendous profitability off the commitments made, and evidence the company’s strategy is building momentum. This adds a heavy bullish weight to the risk-reward symmetry.

- However, on a periodic basis, the returns on existing capital have lagged the hurdle rate (12% average market return in this instance), and thus, there’s been no economic earnings produced over the time frames shown. Without the economic profitability, this to me explains why AVNS has failed to catch a reasonable bid over the last 12–18 months.

Figure 3.

Data: Author, AVNS 10-Q’s

Figure 4.

Data: Author, AVNS 10-Q’s

The delta between incremental and historical returns are actually a bullish feature in the investment debate in my view. It is a demonstration that AVNS’ new capital placements are more profitable than old ones, aligning with the transformation strategy outlined. Further, we get paid for what happens in the future, not what’s already happened. So the increasing ROIC and positive incremental returns tell me AVNS has propensity to continue along this trajectory.

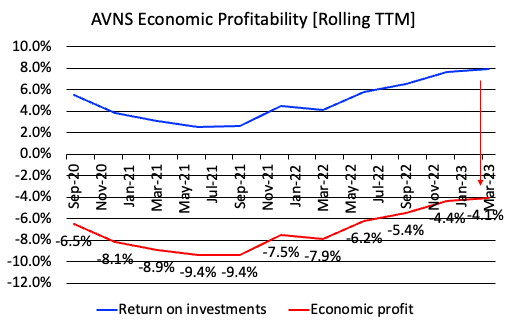

You can see the spread in AVNS’ returns on existing capital and the resulting economic losses in Figure 5. Put simply, a firm must meet or succeed the market’s return on capital (typically an average of ~10–12%, as mentioned) in order to add value for its shareholders.

Investors are looking for the most efficient and effective means to compound capital, and thus capital must be deemed valuable in a company’s hands —more valuable than what it could be in the average investors’ hands. You also need something to benchmark your company against. If you are to allocate even $1 against a firm’s market value, in the form of an equity investment, you’d be expecting the company to be investing at rates of return higher than the benchmarks in order to compound its intrinsic value over time. If the average investor can get an average 10–12% on their money by simply riding the benchmark, a return on invested capital of 13%+ is required from the company in order to add value from an intrinsic value perspective [note: for unprofitable companies in medtech, the stock returns are primarily event-driven, but even then, over time, returns on capital must be eventually produced for long-term equity gains].

Hence, economic losses, absence of major catalysts = no value add for shareholders. This is precisely why the company’s capital budgeting initiatives (including the cost savings, divestitures and investitures) are so important in the AVNS investment debate. AVNS absolutely needs to increase the profits produced on its existing capital in order to re-rate in the mid-term.

Figure 5.

Data: Author, AVNS 10-Q’s

Valuation

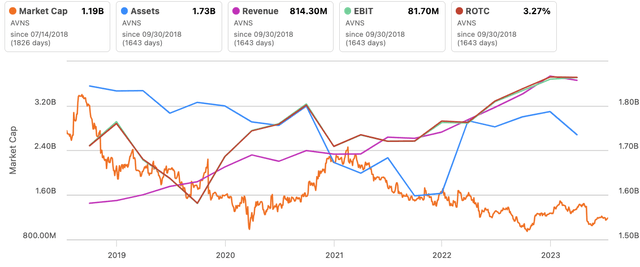

Investors are selling AVNS cheaply at 15x forward earnings and 0.92x book value, 23% and 58% discounts to the sector, respectively. Up until mid–FY’22, it appeared that investors were valuing AVNS primarily on asset factors, as seen below [blue line representing operating assets]. The recent divergence in market value to asset value is therefore an intriguing factor.

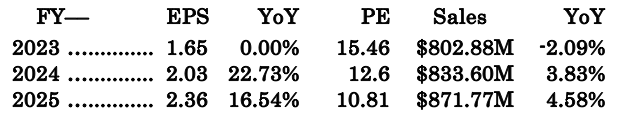

With recent gains in sales and operating income, I’ve revised my FY’23 an FY’24 forecasts higher [see: Appendix 1], and now call for $802.8mm and $833mm at the top line, respectively (from $787mm and $818mm, respectively). I’d be looking to earnings growth of 22.7% next year on these numbers, getting me to 12.6x forward P/E, thus quite the attractive multiple in my eyes.

With the cost savings in place [the company is set to realize $10mm this year] and factoring out the respiratory segment, I still get to ~$40 in equity value, in line with the previous analysis. Hence, I’m retaining this as the next price objective moving forward.

Figure 6.

Data: Author, AVNS 10-Q’s

In Short

AVNS is at a potential inflection point in its growth journey. Management have labelled FY’23 as a “transformational year” for the company, meaning it is leaning up, repurposing capital, and focusing on creating value for shareholders. You see early evidence on this in the recent divestitures and investitures discussed in this report, also in the operating statistics— with respiratory included and excluded.

Moving ahead, I’d be looking to AVNS clipping $802mm in sales this year, a higher number on its existing ROIC, and a price target of $40. To get there, consider that:

- Incremental ROIC is > than historical ROIC, indicating the profitability of the company’s new capital placements;

- The leaner cost structure, adding $10mm to FCF in FY’23 alone;

- No more respiratory segment from FY’24, with the sale to be completed in Q4 this year.

Net-net, I am reiterating AVNS as a buy on the culmination of factors dicussed here.

Data: Author

Appendix 1. AVNS consolidated revised forecasts [financials and multiples]

Read the full article here