This article was first released to Systematic Income subscribers and free trials on July 9.

Welcome to another installment of our Preferreds Market Weekly Review, where we discuss preferred stock and baby bond market activity from both the bottom-up, highlighting individual news and events, as well as top-down, providing an overview of the broader market. We also try to add some historical context as well as relevant themes that look to be driving markets or that investors ought to be mindful of. This update covers the period through the first week of July.

Be sure to check out our other weekly updates covering the business development company (“BDC”) as well as the closed-end fund (“CEF”) markets for perspectives across the broader income space.

Market Action

Preferreds were mostly down on the week as higher Treasury yields took their toll.

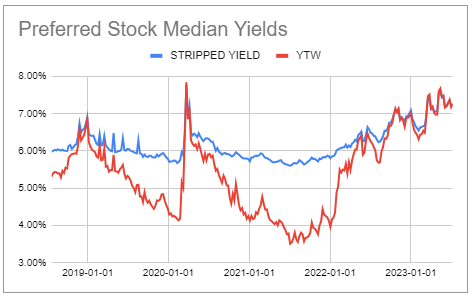

Preferreds yields remain north of 7% – a historically attractive level.

Systematic Income Preferreds Tool

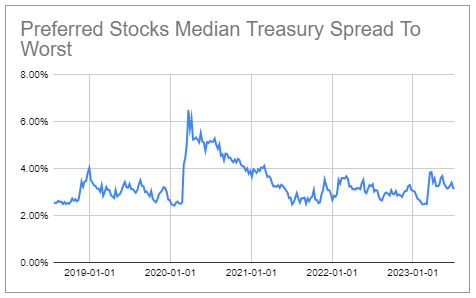

Credit spreads, however, have continued to compress as risk sentiment has improved. On this basis, preferreds look fairly-valued.

Systematic Income Preferreds Tool

Market Themes

On the service we try to cover the broader income space and gauge the risk/reward of various securities. This week a subscriber asked about the relative attractiveness of the mortgage REIT Annaly Series F (NLY.PF) and the CLO Debt ETF (JBBB) which we explore in this section.

On the face of it, JBBB has a higher portfolio yield of 10.6% (its distribution yield is lower) than the 10.2% yield-to-worst or YTW of NLY.PF however NLY.PF has idiosyncratic company risk, significant leverage, mortgage REIT risk and call risk. It seems obvious that JBBB is better on all fronts.

Let’s look at yield first. First, we shouldn’t really use stripped yield (i.e. YTW when the clean price is below $25) for floating-rate preferreds because it reflects lagged Libor from the previous quarterly dividend. Once we do this, the actual yield of the stock is closer to 10.6% not 10.2%. We call this the Float Yield metric in the Preferreds Tool and one we described in an earlier Weekly. Two, in terms of idiosyncratic risk, it’s true that NLY looks like a company whereas JBBB is a fund (technically, they are both registered investment companies but let’s ignore that for now). A company typically carries much more idiosyncratic risk than a fund. However, NLY is really a portfolio of securities rather than a typical company that has suppliers, inventory, factories etc. In this sense there is not much difference between it and JBBB except for what they hold.

NLY also is highly leveraged (as are all mortgage REITs) however it is leveraged on Agency MBS which have no credit risk and are highly liquid. JBBB is not explicitly leveraged however BBB tranches are implicitly leveraged as they are quite thin.

In terms of callability, NLY.PF is redeemable today however CLO debt tranches are also callable though JBBB investors won’t see those calls as JBBB will just reinvest the capital into other tranches. A good way to enhance call protection for NLY.PF holders is to partly hold or move to NLY.PI which has another year of call protection and a lower coupon than Series F.

Finally, a big advantage of NLY is that it’s a preferred so it always references a $25 liquidation preference i.e. there is no way for its “principal” to be eroded. JBBB “principal” however could be eroded through trading costs, management fees, defaults etc.

Overall, the point here isn’t that NLY.PF is better but that it has attractive and comparable qualities to funds and is a nice diversifier for corporate credit exposure.

Stance And Takeaways

Over the last couple of weeks we made several moves in our senior security allocation.

Specifically, we partly rotated from the SiriusPoint 8% Series B (SPNT.PB) to BDC Saratoga baby 2027 bond (SAY). SPNT.PB had a nice run and its yield moved below that of SAY. We view SAY as a higher-quality asset so it made sense to make the switch.

We also switched from mortgage REIT bond (AIC) to sister bond (AAIN) to pick up 0.65% of yield for about a year and a half longer maturity. Historically, AIC has tended to trade at a higher yield than AAIN but that has changed recently, perhaps tied to the upcoming EFC acquisition news.

Read the full article here