There are three metrics to look for when assessing the investment pitch of a business development company; dividend growth, net asset value, and operating momentum. The last metric is measured by growth after adjustment for non-accruals and leverage risk. Farmington, Connecticut-based Horizon Technology Finance (NASDAQ:HRZN) is a BDC focused on the venture lending market with most of its portfolio companies categorizable under life sciences, technology, sustainability, and healthcare information & services. These are broadly privately held and development-stage upstarts backed by venture capital firms. This ticker is essentially a venture lending platform with Horizon most recently underwriting a $30 million venture loan facility for SafelyYou, a San Francisco startup founded in 2015 and focused on providing fall detection and prevention technology for dementia care. It also includes the vertical farming company AeroFarms.

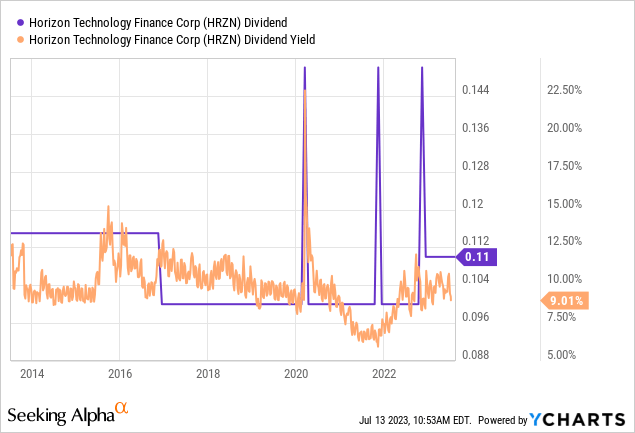

The BDC last declared a monthly cash dividend of $0.11 per share, in line with its prior payout and for a 10.2% forward dividend yield. I’m bullish on BDCs from what’s now set to be one of the most favorable environments to generate excess net investment income as a Fed funds rate hiked ten times to its highest level since 2008 at 5% to 5.25% looks set to be overlayed with a still strong economy. Upcoming post-Silicon Valley Bank collapse banking regulations could also push some demand towards BDC lending platforms with BDC venture loan peer Trinity Capital (TRIN) already flagging an uptick in deal flow. This is not unprecedented with the post-2008 financial crisis regulation birthing over a dozen neobanks.

Net Asset Value Expands As Total Investment Income Surges

Bears would of course highlight that whilst Horizon’s monthly dividend payouts are welcome, the BDC dividend growth history has been poor with the payout trendline being stagnant over the last decade and only briefly interrupted by the occasional annual special. The BDC brought in a total investment income of $28 million for its fiscal 2023 first quarter. This was up a huge 97% from $14.2 million in the year-ago comp. Horizon’s debt portfolio had a yield of 16.3% for the quarter on the back of a floating interest rate structure that heavily capitalized on the marked rise in the Fed funds rate. This was also flagged by management as being one of the highest portfolio yields in the industry. Critically, 96% of the outstanding principal on Horizon’s debt investments bore interest at floating rates as of the end of the first quarter.

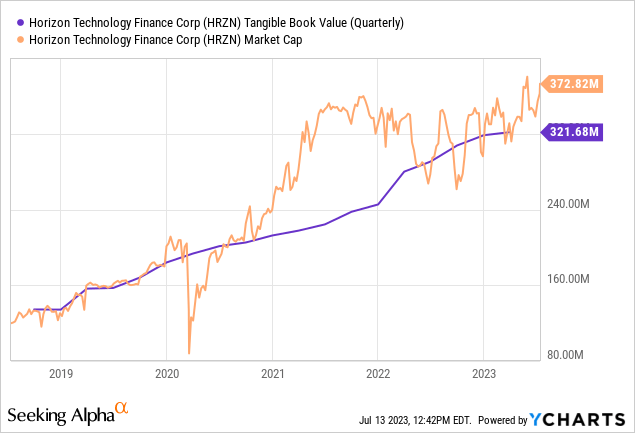

The BDC’s total investment portfolio also stood at $715.3 million which drove a net asset value of $321.7 million, around $11.34 per share. This was up sequentially from $318.4 million in the fourth quarter and $280 million in the year-ago comp. However, it did dip by $0.13 sequentially with the weighted average number of shares outstanding growing to 28,227,100 from 21,904,160 in the year-ago period. The BDC is currently swapping hands at a 14% premium to NAV per share which has meant opportunistic stock offerings to raise capital. Horizon most recently sold 3,250,000 shares for $40.63 million in gross proceeds that will be used to repay outstanding debt under its revolving credit facility with KeyBank. As a general rule, stock sales above NAV should be accretive to earnings.

Lending Momentum Set To Continue As Dividend Fully Covered

Net investment income of $13 million, around $0.46 per share, was a material increase from $5.7 million and $0.26 per share in the year-ago comp. This meant the 3-month aggregate of the monthly payouts was 139% covered by NII per share. This drove a spillover income of $0.81 per share which stands to surpass $1 per share before the end of fiscal 2023 on the back of continued lending momentum and a Fed funds rate that could be hiked by another two 25 basis points through to the end of 2023. Headline CPI fell to 3% for June, its lowest level in over two years, but the markets are still pricing in a 92.4% chance of the Fed hiking rates at its upcoming July 26th FOMC meeting.

The BDC is set to ride this elevated interest rate environment with expectations that a possible FOMC interest rate cut will only be considered towards the end of the first half of 2024. Horizon funded eight loans totaling $40.2 million as of the end of the first quarter and also held cash of $43.5 million and a credit facility capacity of $133.3 million. The BDC has moved to expand its credit facility by $50 million and recently updated the market that it has originated 12% more new loans on a sequential basis for its soon-to-be-announced second quarter. However, I’d flag that AeroFarms which the BDC has two term loans with a combined $7.2 million fair value as of the end of the first quarter filed for Chapter 11 in June. Critically, whilst the current environment is positive for NII, it rapidly ramped up the stress facing companies, and Horizon could see an uptick in loans on non-accrual status. The ticker is still a cautious buy here.

Read the full article here