Following our recent financial analysis of Bridgestone Corporation (OTCPK:BRDCY, OTCPK:BRDCF) and Compagnie Générale des Établissements Michelin (OTCPK:MGDDF, OTCPK:MGDDY), today we are finalizing our tire update with Continental Aktiengesellschaft (OTCPK:CTTAF, OTCPK:CTTAY). As a reminder, the German player is not only active in tire manufacturing but also is one of the most relevant original equipment manufacturer (OEM) suppliers. Indeed, if we look at the recent Q1 update, the company’s tire revenue represents 35% of total top-line sales, while ContiTech and the automotive division account for 15% and 50% of the total turnover, respectively. In our last update (Q4 comment), we analyzed how 1) the dividend per share was further cut with a payment of only €1.5 per share, 2) we were expecting lower margins with still uncertainty on 2023 recovery (especially in the automotive segment), and 3) Conti was fairly priced in on a reverse Price Earning valuation. Our publication titled ‘Staying On The Cautious Side,’ with a prudent approach, proved right. Continental underperformed the S&P 500 return (including the dividend already paid in early May 2023) and declined by almost 8.5% at the stock price level.

Mare past analysis

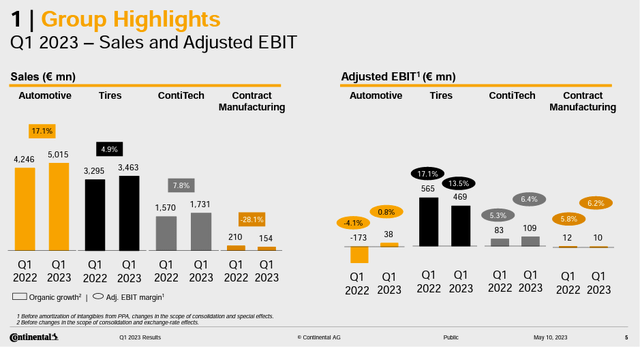

To sum up, the company delivered a beat compared to low Wall Street expectations. In detail, the top line reached €10.3 billion at the aggregate level, slightly above estimates at €10.2 billion. The company delivered an adj. operating profit margin of 5.6% at €578 million compared to estimates of €478 million.

Going to the detail, here below are our main highlights of the division with our Q2 forecast:

- Automotive: Revenue was supported by organic growth (17%) with small support from FX evolution (1%). We should say that the company strongly outperformed in the EU and China, lagging in North America. According to Continental, this performance was due to a few clients that pushed volumes out by a quarter and is forecasted to reverse. Here at the Lab, we prefer not to focus on a quarter but look at the output going forward. Key to emphasize is the lower margin compared to Q4, as inflation has hit. Here at the Lab, we forecast a gradual sequential margin improvement with higher earnings in the segment (€61 million with a 1.2% adj. margin), which is mainly derived from a better operating leverage in production; however, we are confident that the margin recovery will show the real story starting from Q3;

- Tires: Sales growth reached a plus 5% and was split by a minus 8.6% in volumes and a plus 13.5% from positive price/mix evolution (FX was minor). Looking at Michelin and Bridgestone, the company recorded higher volume losses and came below the competition. Here at the Lab, we believe the company is protecting its margin. Indeed, Bridgestone’s price/mix reached a plus 10% while Michelin’s a plus 12.3%. Still related to volumes, we see weakness in low-performing tires while the premium segment remains solid. Looking at the margin, the core operating profit stood at 13.5%, in line with expectations. There was also a positive one-off related to inventory gain, which accounted for a plus €50 million. In the tire division, dealer stock remains elevated, and we should not forget competition from Asian manufacturers. Our team does not expect the guidance to be changed in Q2, forecasting lower volumes with an FX headwind more than offset by price/mix evolution. In detail, our sales forecast reached €3.5 billion with a 13.1% in core operating profit margin;

- ContiTech: As already mentioned, ContiTech reported good numbers. Sales were up 10%, and adj. EBIT margin was at 6.3%, with an improvement on a quarterly basis and a positive price evolution. We expect a positive division in line with Q1 2023 with an FCF of around €50 million for Q2. ContiTech revenue is forecast at €1.7 billion with a margin of 6.5%.

Continental Q1 Financials in a Snap

Conclusion and Valuation

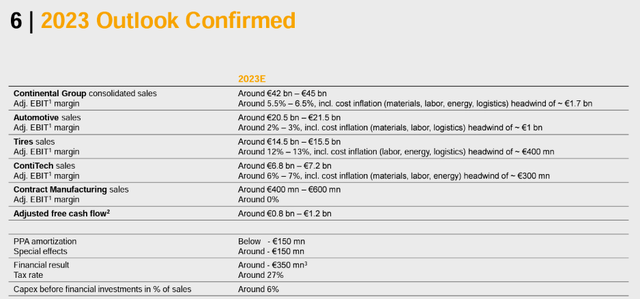

There was an outflow of minus €952 million on Continental’s free cash flow, mainly driven by higher working capital requirements. Aside from higher inventories that drag cash by almost €500 million, we believe the company agreed to pass-throughs additional costs with clients’ payment delay. The 2023 outlook was left unchanged, and we think that Continental will confirm the guidance with sales in the €42-45 billion range and adj. EBIT margin between 5.5% and 6.5% on the group level. Looking at the division, the outlook is for 2-3% in Automotive, 12-13% in Tires, and 6-7% in ContiTech. This already incorporates a cost inflation headwind of €1.7 billion (last time, we already estimated a higher cost of €1.5 billion) with a free cash flow between €800 and €1.2 billion.

2023 Conti outlook

Overall, we see this 2023 as very much similar to 2022, with an outlook that remains dependent on pass-throughs to automotive suppliers and a story of efficiency gains and volume recovery throughout the year. Conti’s Auto division reported a positive margin; however, it was down on a quarterly basis, while ContiTech and the tires segment reported good numbers, albeit arguably looked over by Wall Street. Here at the Lab, Q1 results do not change the overall negative narrative on the company. Conti needs to deliver a margin step up in the Auto segment. That said, we decided to remain on the sidelines. A comps valuation also supports this. As a reminder, Bridgestone and Michelin’s payout are towards 50%, with a dividend yield of 5% and 3.3% compared to Conti at 2.19%. Bridgestone and Michelin’s payout is well covered by cash flow yield at 9%, while Continental is still lagging. Michelin’s price-earnings is 8.97x is lower than Continental Aktiengesellschaft P/E, which is at 9.44x with an EV/EBITDA of 4.45x. Therefore, we favor Michelin and remain neutral on Continental with a target price of €66 per share ($7.2 in ADR), valuing the company with a P/E of 8.5x.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here