Investment Thesis

I argue that Roblox (NYSE:RBLX) is growing more stably than it may appear at first.

But I’m quick to note that the bull case is not without blemishes. Indeed, its underlying profitability leaves investors wanting more.

Nevertheless, I make the argument that if Roblox can convince investors that the business is still growing at 20% CAGR, investors will be keen to back this stock and this would see its multiple re-rating higher.

Here’s why I’m bullish on Roblox.

Why Roblox?

Roblox allows users to create their own games, virtual worlds, and experiences using its platform. Roblox provides a social platform where users can connect with friends and join communities. Its platform is free to play, allowing users to enjoy a lot of free content without any upfront cost.

The way that Roblox monetizes its platform is through in-app purchases. All that being said, there are a few considerations that are weighing on its stock, which we’ll turn our focus towards.

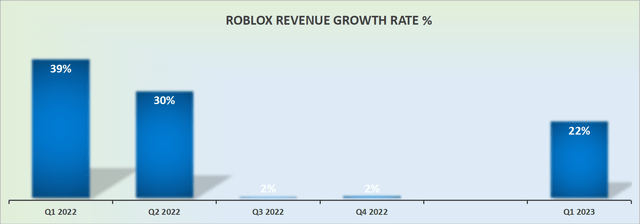

Revenue Growth Rates Are More Stable Than They Seem

RBLX revenue growth rates

Roblox is growing at around 20% CAGR. That’s clearly not a company that is in hyper-growth mode, but if Roblox can convince investors that it’s stably growing at 20%, this would positively entice investors to reconsider the stock.

Furthermore, bookings, which is a leading indicator of revenue growth rates, were up 23% y/y in Q1. This once again suggests that Roblox has what it takes to grow at 20% CAGR.

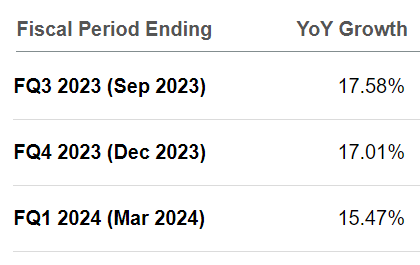

What’s more, if we make the assumption that Q2 2023 ends up growing against the same period a year ago by 20% CAGR, this would mean that H2 2023 would be up against much easier comparables and could with ease grow at close to 20% CAGR.

SA Premium

Now, this is where we get to the most critical and pressing question. Can we make the case that in 2024 Roblox is able to grow by 20% CAGR? I believe that even if it can’t grow by 20%, it will be extremely close to this figure. And why is that important?

The importance for investors is that, if a company is growing rapidly but is highly volatile, it will get a lower multiple than a company that can be “counted” on for slow and steady predictable growth.

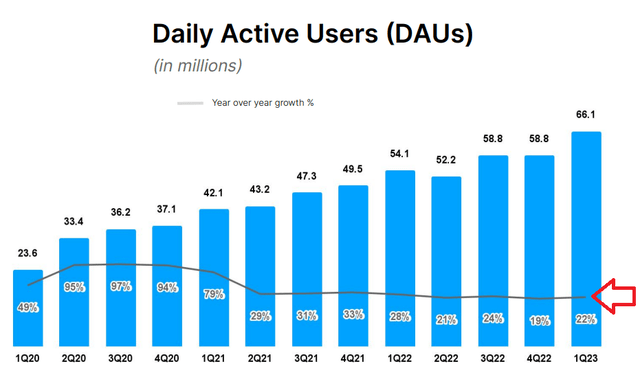

As evidence for my thesis, consider Roblox’s customer adoption curve.

RBLX Q1 2023

What you see above is that Roblox’s DAU figures appear to be growing in the range of +20% CAGR. If Roblox can continue to deliver approximately 20% DAU growth rates, this would be yet another supporting argument that in 2024 Roblox has the potential to grow its revenues at 20% CAGR.

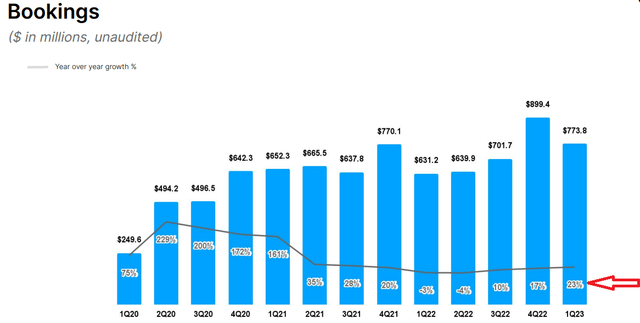

So, that’s where the heart of the bull/bear case lies. Can Roblox grow in the post-pandemic environment by 20% CAGR? Or to put it more concretely, can Roblox stabilize the y/y growth in bookings, see red arrow.

RBLX Q1 2023

If, when Roblox reports its Q2 2023 results in a few weeks’ time, bookings are once again up about 20% y/y, I believe that investors will be more than willing to give the stock the benefit of the doubt.

Next, let’s discuss Roblox’s profitability.

Free Cash Flow Leaves a Lot to be Desired

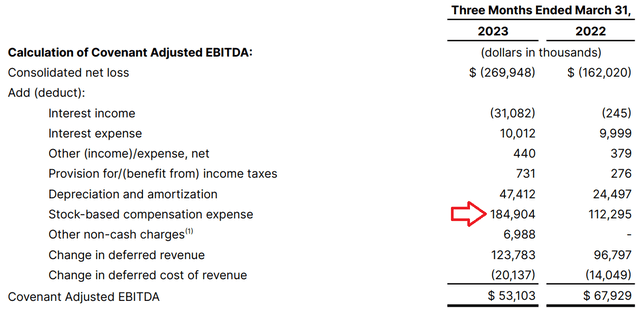

To be balanced, the one thing that weighs on the stock is that the vast majority of Roblox’s profitability is stock-based compensation.

RBLX Q1 2023

And to add to the insult, stock-based compensation was up 65% y/y, even as revenues were up in the mid-20s%. This implies that management is taking more in compensation than they are actually growing the business.

Or, to put it another way, approximately 28% of Roblox’s revenues is stock-based compensation. For a business that is growing in the around 20%, there appears to be something not quite right with this compensation structure.

I would counter this by noting that Roblox hasn’t seen its multiple expand this year. As we look across the board, countless stocks have seen their multiple expand since April, but Roblox hasn’t participated in this upside re-rating.

My point is that if Roblox can convincingly grow its revenues in Q2 2023 and show that bookings for Q3 also come in strong, I make the case that investors will be willing to give the stock the benefit of the doubt.

The only caveat here is if Roblox once again deems it necessary to gouge out from its revenues excessive stock-based compensation. And if that’s the case, I’ll promptly downwards revise my rating on this stock.

The Bottom Line

Roblox is not in hyper-growth mode.

Despite concerns about profitability, Roblox has the potential to grow at a 20% compound annual growth rate and attract investor support.

Recent bookings growth of 23% year-over-year in Q1 2023 indicates the company’s ability to sustain its 20% CAGR.

The critical question for investors is whether Roblox can maintain this growth rate in the post-pandemic environment.

If the upcoming Q2 2023 results show bookings around 20%, investors are likely to turn optimistic.

However, the company’s profitability is hindered by stock-based compensation, which represents a significant portion of its revenues.

Nonetheless, if Roblox can demonstrate strong revenue growth and avoid excessive stock-based compensation, investors may be inclined to reassess the stock positively.

Read the full article here