Introduction

Netlist, Inc. (OTCQB:NLST) is an OTC (over-the-counter) play that offers investors the opportunity to capitalize on the growing demand for hybrid memory solutions (put another way, solutions that effectively fuse DRAM’s finer access speeds with NAND flash’s higher densities and cheaper economics) by enterprise customers across various industries. Netlist’s range of high-performance modular memory subsystems is primarily tapped by OEMs from the server, HPC (high-performance computing), and communications industries.

If this story piques your interest, here are a few other pointers worth considering.

Key Business and Operating Considerations

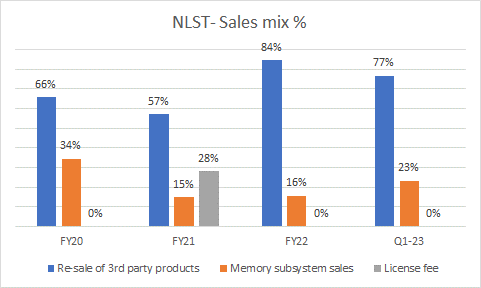

Even though NLST’s long-term ambition is to generate ample business through the sale of its modular memory subsystems, unfortunately, as things stand, that isn’t the major driver of topline growth. Rather, as highlighted in the image below, NLST’S sales narrative in recent periods has largely been driven by the re-sale of components to memory channel customers, which in turn are sourced from other vendors (these are opportunities that crop up on account of gaps in the distribution channels of component manufacturers), most notably SK hynix.

Company filings

The drawback of having such a large chunk of re-sales in your overall mix is that it typically restricts gross margin progression; NLST not only needs to account for the original cost of the components purchased but also add another markup for the cost of sales for these products.

What’s also challenging is that NLST doesn’t quite enjoy the luxury of clear order visibility. The company does not have any long-term agreements with its customers but rather receives purchase requests roughly 2 weeks before the preferred delivery date; these order requests are also susceptible to be capricious nature of its clients and can be rescheduled or canceled on short notice. Thus, NLST could come across various instances where it has sourced high-priced component inventory from SK hynix and the like but is unable to get rid of it at acceptable prices. This too will cause gross margin pressures.

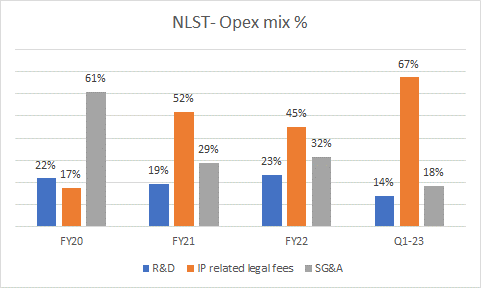

Then on the OPEX side, it’s worth considering that a few years back, funds were predominantly deployed in avenues such as R&D (Research & Development) and SG&A (Selling, General & Administrative) but lately the onus has shifted towards paying legal bills related to IP (Intellectual Property) disputes. In Q1, these legal costs accounted for over two-thirds of the total OPEX base, and NLST management has confirmed that it is likely to stay at these elevated levels all through FY23.

Company filings

Dig deeper into the triggers of these legal costs and you’ll then understand why so many investors gravitate to NLST.

Besides the re-sale of component products and the sale of modular systems, NLST can also license its portfolio of IP and procure fees for this. Not always, but these agreements typically come about after a legal battle with other bigger tech entities who are believed to have infringed on NLST’s patents. We saw this happen with SY Hynix a few years back, and more recently efforts will be made to reach out to Samsung Electronics and explore a potential licensing deal.

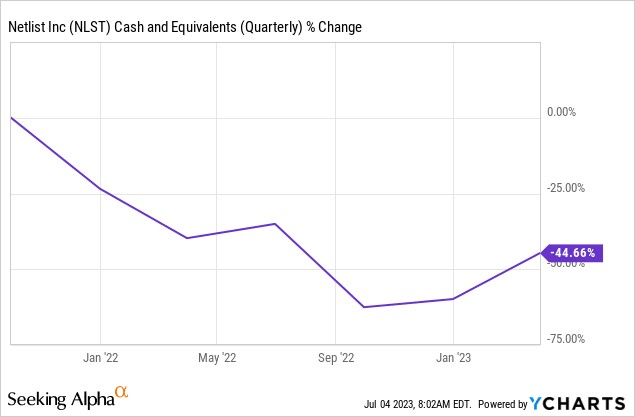

Crucially the quantum of funds that NLST usually wins during these legal tussles can often prove to be quite monumental (for instance, back in April, NLST won over $300m in damages in a patent infringement case with Samsung Electronics at the Eastern District of Texas), and can help prop up the financial position of the business. The $300m works out to roughly 10x, NLST’s current cash on books, something which had come off a long way (down by -45% from the $64m levels seen in Q3-21).

YCharts

It looks like the IP infringement sub-plot of NLST has legs, as the company is currently in the midst of a battle with not just Samsung, but even the likes of Micron, and more crucially Google. Of course there’s no guarantee that NLST wins all these cases but management sounded increasingly confident about their position on the earnings call back in April.

Closing Thoughts: Stock-Related Considerations

This is something that perhaps should’ve been mentioned at the start of this article, but nonetheless, it’s better late than never. We don’t believe the NLST stock is meant for the faint-hearted or those with a conservative risk appetite.

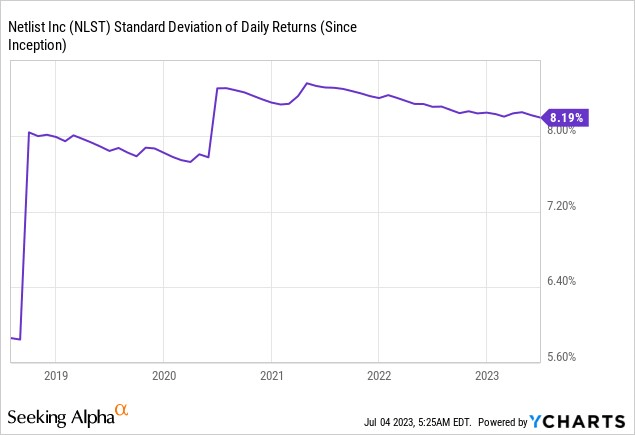

To get a sense of this facet, do consider the heightened level of gyrations associated with the daily movements of the stock. YCharts data shows that over the last few years, investors have had to consistently deal with standard deviations of over 8% on a daily basis. This elevated and relentless bout of instability every other day, can be very damaging for someone seeking to build a position in the stock.

YCharts

Then, if we shift our focus to NLST’s daily price movements, it’s fair to say that things are currently not in the best shape. From the first week of December last year, until April 2023, the stock had been trending up in the shape of an ascending broadening wedge pattern.

Investing

However, since then, we’ve seen a series of lower lows and lower-highs reiterating the presence of bearish momentum in the stock. In mid-June, we saw a breakdown below the lower boundary of the wedge, and more recently we’ve also seen a break below the psychologically crucial 100DMA for the first time since early Feb.

All in all, until we see a flattening out of the price action or the abatement of the ongoing downtrend (an end to the sequence of lower lows and lower-highs), we don’t believe it would be wise to kickstart a long position.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read the full article here