Note:

I have covered Transocean Ltd. (NYSE:RIG) previously, so investors should view this as an update to my earlier articles on the company.

Last week, leading offshore driller Transocean Ltd. or “Transocean” reported an impressive contract win for the harsh-environment semi-submersible rig Transocean Equinox:

Transocean Ltd. (…) today announced a 16-well binding award for the Transocean Equinox in Australia for a consortium of four operators. The estimated 380-day campaign contributes approximately $184 million in backlog, excluding full compensation for mobilization and demobilization. The engagement also includes options that, if fully exercised, could keep the Transocean Equinox working in Australia into 2028.

This new award is expected to commence in the first quarter of 2025 in direct continuation of the rig’s previously announced five-well, 300-day commitment in Australia with a major operator, currently expected to start in the first quarter of 2024.

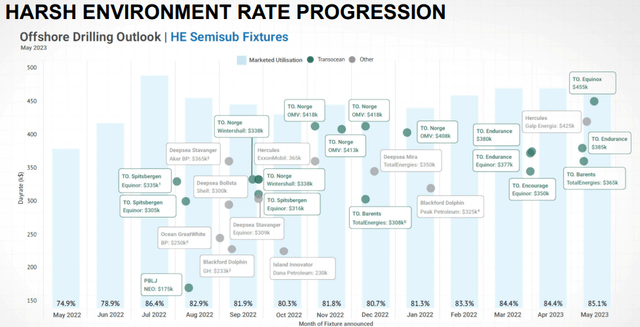

Including mobilization and demobilization fees, the estimated dayrate should be well above $500,000, a number not witnessed for almost a decade in the harsh environment of floater space:

Company Presentation

According to Esgian Rig Analytics (“Esgian”), the operator for the contract is understood to be well management company Zenith Energy, representing Beach Energy (OTCPK:BEPTF, OTCPK:BCHEY), Cooper Energy (OTCPK:COPJF), Woodside Energy Group (WDS, OTC:WOPEF), and ConocoPhillips (COP).

Remember, Transocean Equinox has been sitting idle since October 2022 after Equinor (EQNR) surprisingly terminated the rig’s long-term contract ahead of time.

While the rig is likely to remain warm-stacked for the remainder of the year, Transocean recently secured new work for the unit offshore Australia with the 300-day contract expected to commence in the first quarter of 2024.

Assuming the exercise of all options for the rig, Transocean Equinox won’t be available for new employment until 2028.

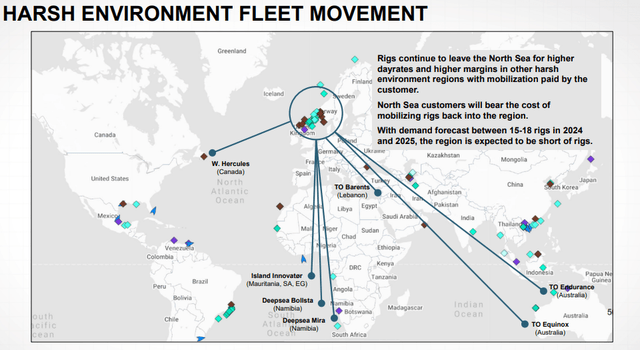

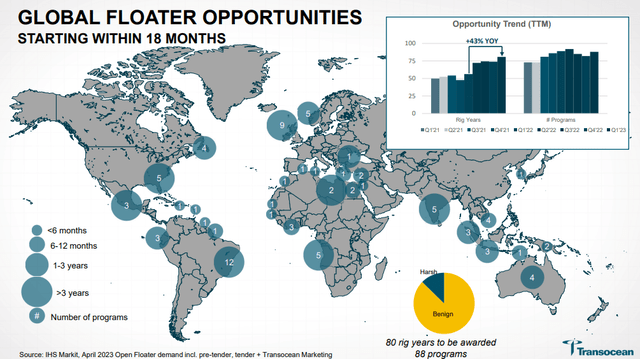

With sister rig Transocean Endurance and several other harsh environment floaters also scheduled to leave the currently weak North Sea markets, the region might very well end up being short of rigs once demand is returning:

Company Presentation

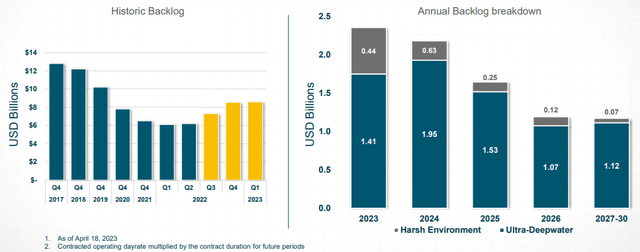

While the latest contract award is certainly great news, investors will likely have to prepare for a sequentially lower backlog number in Transocean’s next fleet status report later this month.

Company Presentation

In fact, the company has not disclosed a single drillship award in recent months which isn’t exactly comforting given the fact that the ultra-deepwater drillship Discoverer Inspiration has been sitting idle in the U.S. Gulf of Mexico for some time now.

In addition, ultra-deepwater drillship Deepwater Invictus is scheduled to roll off the contract later this month.

That said, even with drillship demand in the U.S. Gulf of Mexico apparently not as strong as previously anticipated, there are still opportunities in other regions, particularly Brazil and West Africa.

According to Esgian, Petrobras (PBR) has invited a number of rigs to move into phase two for the Buzios tender:

This follows the retendering of the opportunity in March to update the target start window and provide an extended mobilization period in order to accommodate newbuilds or reactivations. Petrobras is understood to have requested new pricing, with the new offers believed due by 14 July.

Moreover, Esgian indicates that Azule Energy is close to awarding a new drillship contract for work offshore Angola.

Assuming no further material contract awards until the release of Transocean’s next fleet status report, I would estimate aggregate gross backlog addition to be below $400 million.

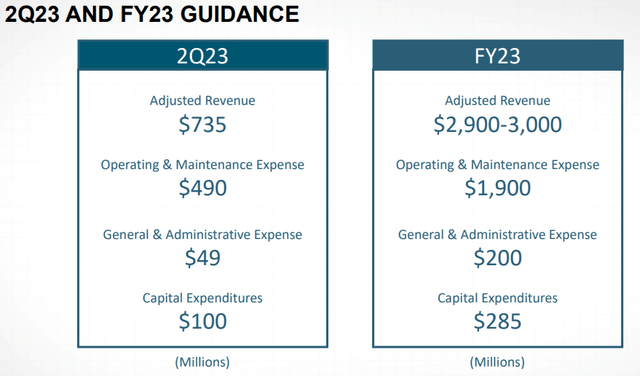

With projected Q2 contract drilling revenues of $735 million, I would expect the reported backlog to be down by up to 5% sequentially to between $8.2 billion and $8.3 billion.

Company Presentation

In addition, Transocean is unlikely to announce cold-stacked drillship reactivations in the company’s upcoming Q2 report which might be considered disappointing by some investors.

That said, overall market conditions remain strong, and I would be very surprised to see Deepwater Inspiration and Deepwater Invictus sitting idle for an extended period of time.

Company Presentation

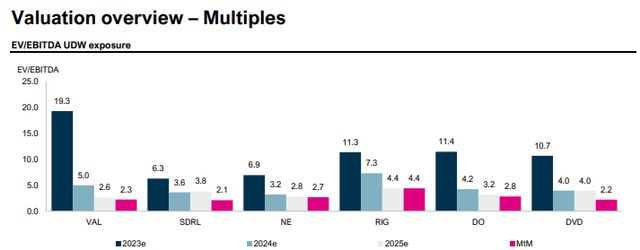

Valuation-wise, Transocean remains expensive relative to peers based on 2024 profitability expectations:

Pareto Securities

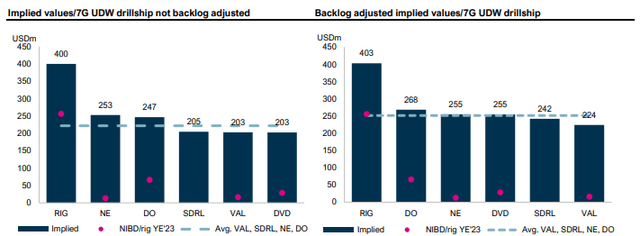

The same goes for implied 7th generation drillship values:

Pareto Securities

Given this issue, investors should also consider other U.S. exchange-listed competitors like Noble Corp. (NE), Valaris (VAL), Seadrill (SDRL), and Diamond Offshore (DO) as well as jack-up pure play Borr Drilling (BORR).

Bottom Line

Transocean reported an impressive contract win offshore Australia which might keep the harsh environment semi-submersible rig Transocean Equinox in the region well into 2028.

While the company has demonstrated substantial progress on the semi-submersible front in recent months, Transocean has not reported a single drillship award since the company’s last fleet status report in mid-April.

As a result, net backlog addition in the upcoming July fleet status report is likely to be negative.

Moreover, some investors might be disappointed by the ongoing lack of cold-stacked drillship reactivation announcements, but I wouldn’t be surprised to see an award offshore Brazil later this year for one of the cold-stacked 7th generation drillships inherited from Ocean Rig.

While shares remain expensive based on a number of key metrics when compared to U.S. exchange-listed competitors, I would use any major weakness to initiate or add to existing positions as the industry outlook remains strong.

Read the full article here