Recent events at Amyris (NASDAQ:AMRS) could be interpreted as the beginning of a turnaround, but for every positive there is a negative. The company finally appears to be serious about cutting costs, but there has been no news regarding asset sales. The PwC consulting engagement and the CEO’s exit may lead to the resolution of performance issues, but shareholders continue to be left in the dark. Amyris has a limited runway in which to sell off assets and reduce cash burn, but it is unknown how either of these initiatives are progressing. In this regard, no news is likely bad news.

CEO Resignation

Many investors are likely to view John Melo’s exit as an overwhelming positive, as he has often been held accountable for all of Amyris’ problems. Despite this, it should be kept in mind that Melo would not be leaving if things were going well. Amyris is Melo’s life’s work, and it is unlikely he voluntarily stepped away from the role, as he will now be cast as a failure even if the company succeeds going forward. Melo is also no longer on Amyris’ board, so this is more than just an issue of Amyris seeking a more suitable CEO.

Internally, the company has known it has had serious issues for the past six to nine months, and yet a reduction in force was only just announced and Melo “resigned” without a replacement CEO ready. Han Kieftenbeld may be adequate for the role, but it is hard to imagine he was anyone’s first choice. This begs the question of whether Melo and Amyris parted ways suddenly, or if Amyris has just not been able to find a suitable replacement CEO. Given Amyris’ current situation it also seems less than ideal that the CEO and CFO roles are not separated.

The other consideration is what Melo’s resignation means for the deals that should be nearing completion:

- Manufacturing JV

- Brand sales

- Strategic transactions

It seems unlikely that Amyris would fire its CEO if a large transaction was in the process of being negotiated.

Communication Issues

One of the most concerning aspects of Amyris’ recent problems has been the lack of communication with shareholders. Amyris is quick to highlight any perceived positive news, but is reticent to share negative news and generally gives no insight into problems. For example, Barra Bonita has been operational for around 12 months, and yet ingredient revenues remain low, and ingredient losses are still large. Despite this, there has been no real discussion regarding Barra Bonita beyond general statements about how it was lowering production costs.

The announcement of Melo’s exit and the headcount reduction indicate that the poor treatment of shareholders is likely to be ongoing. There was little detail regarding Melo’s exit or how the work with PwC is progressing. More importantly, there were no details about the layoffs. Amyris has a weak balance sheet and large losses, a situation that must be resolved in the near future. It is therefore important for shareholders to understand the size of the layoffs, where these layoffs are occurring, and how this will affect cash burn going forward.

Sinking Ship

In addition to Melo’s resignation, Amyris’ Chief Science Officer and Head of R&D, Sunil Chandran, also recently left the company. Chandran’s exit from Amyris is potentially the bigger news, and also has negative implications. Chandran had been with Amyris for many years and given the company’s pipeline of molecules and more speculative projects, like the production of antibodies using yeast, it is not clear why he would leave Amyris if he thought the company had a bright future. This could suggest that R&D spend is going to be massively curtailed and that as a result Chandran decided to pursue opportunities elsewhere.

PwC Engagement

On June 5 it was announced that Amyris’ Board of Directors had engaged the Business Recovery Services unit of PwC and established a Restructuring Committee to execute a transformation project. This program aims to deliver a 250 million USD annual reduction in costs, as well as improve the company’s capital structure and liquidity.

This type of consulting arrangement will likely be expensive, something that Amyris cannot currently afford. It is also quite damning that a third-party has been brought in to try and resolve issues that Amyris has been working on for the better part of 12 months.

There is also the possibility that PwC and the Restructuring Committee decided an immediate change in management was needed after discovering the extent of the company’s problems.

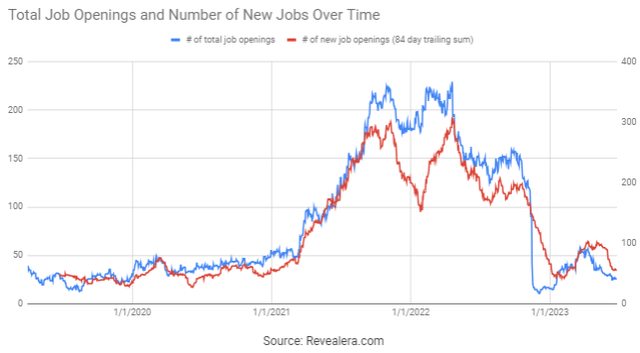

Layoffs

Amyris recently announced a global reduction in force as part of cost reduction initiatives, although there has been no indication of how large the layoffs are. Given the size of Amyris’ losses, the company needs to dramatically reduce its headcount. Some of this should come through brand sales, but large layoffs are needed if the company is serious about avoiding bankruptcy. The fact that details of the reduction in force were not communicated to shareholders is hardly comforting. There also doesn’t currently appear to be a hiring freeze in place, despite the company’s struggles.

Figure 1: Amyris Job Openings (source: Revealera.com)

Business Fundamentals

Amyris’ growth appeared to hit a wall towards the end of the fourth quarter of 2022, with the company facing liquidity issues after failing to close the strategic transaction with Givaudan in a timely fashion. Outside financing and the receipt of cash from Givaudan now appear to have enabled Amyris to continue expanding, albeit at a slower pace than in 2022.

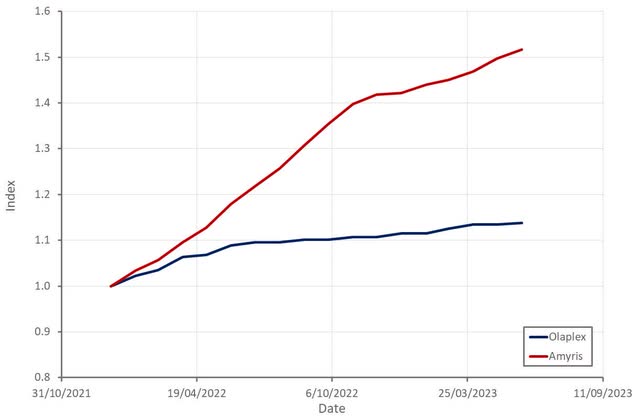

Figure 2: Brand Awareness Indices (source: Created by author)

At this point growth is something of a secondary concern though, as Amyris has done little to improve profitability. This is concerning as supply chain pressures have eased significantly and Amyris has been bringing production in house for the better part of 12 months.

Costs will likely continue to be an issue for Amyris in the second quarter due to a combination of:

- High feedstock costs

- Underutilization of facilities

- Overstaffing

- Inefficient operations

Feedstock costs are a particular concern as sugar prices were elevated in 2022 and spiked higher in March 2023. This appears to be correcting now, but assuming sugar prices are representative of sugarcane prices, ingredient margins will likely continue to be depressed.

While Amyris does not break out gross profit margins by segment, the fact that gross margins are still low after the consumer business has grown so much indicates that ingredients losses are large. The reason for this isn’t clear, particularly given that Barra Bonita should have helped to resolve this situation.

Precision fermentation at scale is obviously difficult, but it can be done. DSM has been operating Brotas for a number of years now, and the fact that it is still running presumably means that it is profitable. Despite having to utilize CMO’s, Evolva has better ingredient gross profit margins than Amyris. Most of Evolva’s production has been of Vanillin, and Evolva has been using the same CMO in Spain as Amyris.

Conclusion

Senior leadership turnover and engaging a consulting firm are not things that would be occurring if Amyris’ turnaround was progressing as expected. If anything, recent developments probably indicate that the company’s situation has continued to deteriorate.

While the financial situation is dire, Amyris has a number of valuable assets, which should mean that bankruptcy is not an immediate concern. For example, the sale of Biossance alone would likely be enough to resolve a lot of the company’s financial problems.

Amyris still has potential, but it is unclear whether the company can capture any of the value it has created, or if it will continue to bleed out while selling off assets on the cheap.

Read the full article here